Asset Allocation Bi-Weekly – Small Caps and the Hope for a Soft Landing (June 24, 2024)

by the Asset Allocation Committee | PDF

They don’t call him Maestro for nothing. In the mid-1990s, Federal Reserve Chair Alan Greenspan achieved what was once thought of as impossible: an economic soft landing. As the US labor market showed signs of tightening, he raised interest rates from 3% to 6% in 1994 to preemptively combat inflation. In 1995, he lowered rates strategically to avoid a recession. The seamless transition from a tightening cycle to an easing cycle led some to believe the Fed could pull the strings in the economy in a way that could both prevent a recession and tame runaway inflation.

The market took notice. Greenspan’s policies helped quell investor anxieties about a repeat of the inflationary surges that plagued the 1970s and early 1980s. Emboldened by this newfound confidence, investors poured money into smaller, unproven companies with strong earnings growth potential. This sentiment was epitomized in 1995, when tech guru Marc Andreessen and his partner Jim Clark did the unthinkable by taking their company, Netscape, public before it had turned a profit, paving the way for what is now viewed as the dot-com bubble.

Today’s elevated interest rate environment has sparked nostalgia for another soft landing. Eager for a repeat of Greenspan’s success, investors were waiting for a decline in rates to re-enter the market. However, their hopes were dashed in June 2023. Not only did Fed policymakers raise rates following the collapse of Silicon Valley Bank, but they also signaled their intention for two additional hikes that year. This spooked markets as investors were concerned that the central bank may keep rates high for long enough to tank the economy.

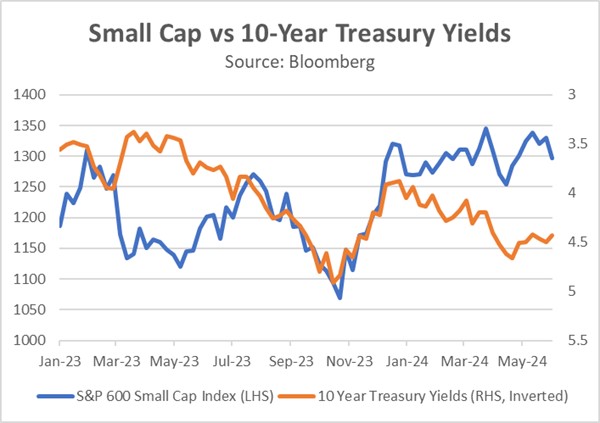

This commitment to raising interest rates discouraged investors from holding riskier assets, particularly those with floating rate exposure. Further pressuring the market were concerns about the rising national debt, which prompted Fitch to downgrade the US credit rating. Investors responded by offloading riskier assets within their portfolios. As a result, the 10-year Treasury yield soared to approximately 5%, a level not seen in over two decades, while the S&P SmallCap 600 Index plummeted to a nine-month low.

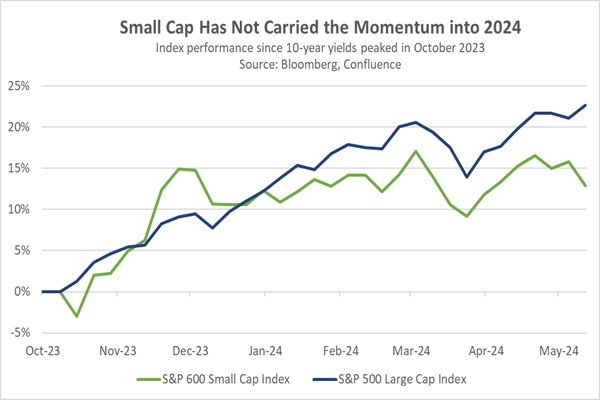

The tide began to turn in late October of last year. The US Treasury’s reallocation of bond issuance toward shorter maturities, coupled with Fed officials signaling an indefinite pause in rate hikes, significantly impacted market sentiment. Investors piled into longer-term bonds and risk assets in anticipation of the Fed’s next move, positioning themselves for an imminent rate cut, which they thought could take place in the first quarter of 2024. From October to December, the S&P SmallCap 600 Index outperformed the S&P 500, with a return of 21.5% compared to 13.7%, respectively.

Unfortunately, the early strength of small caps faded quickly as the S&P 500 recaptured its leadership position at the beginning of 2024. This new weakness in small caps stemmed from concerns that the Fed wouldn’t cut interest rates as deeply as the market anticipated, following a series of strong Consumer Price Index reports in the first quarter and a persistently tight labor market. This situation led investors to reduce their holdings of longer-term Treasurys and refocus on large cap companies due to their relatively strong earnings potential and resilience to changes in financial conditions.

In fact, recognizing this trend early on prompted us to take action in the second quarter. We strategically reduced our exposure to small cap stocks within the conservative portfolios of our Asset Allocation program. This decision also reflected our growing concern that small cap stocks may face longer-term challenges due to certain structural market factors, including the rising popularity of passive funds that funnel money into large cap stocks and the increasing ability of private equity firms to acquire the most promising small cap startups. Hence, an emphasis on quality while screening for indicators such as profitability, leverage, and cash flow should mitigate some of these factors.

Currently, the S&P SmallCap 600 Index has been in a holding pattern as investors await signals regarding the Fed’s next policy move. Should Chair Powell manage to orchestrate another soft landing in the coming months, it could attract investors back to small cap stocks. With the current multiples for the S&P 500 outpacing those of the S&P SmallCap 600 by the widest margin since the dot-com era, small cap stocks present appealing valuations compared to their larger counterparts. With that in mind, we think small cap stock values could rebound in the coming months if US economic growth remains healthy and both inflation and interest rates fall.