Asset Allocation Weekly (May 18, 2018)

by Asset Allocation Committee

In our asset allocation process, we focus on cyclical trends; that doesn’t mean we pay no attention to secular trends but it isn’t our primary emphasis. The lack of clarity around what these terms mean can lead to confusion. And so, over the next few weeks, we will examine the difference between the two trends and how we address them in our asset allocation process.

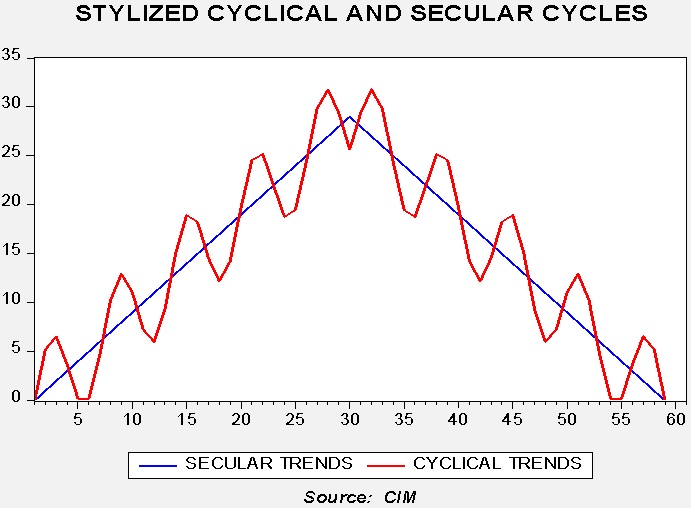

This chart shows a stylized example of cyclical and secular cycles. It’s simply for illustration purposes, but it does express the general view of how we view markets. In reality, cyclical trends are not this smooth or regular, but rather often exhibit varying length and amplitude. Secular trends are not necessarily constant either. But, in general, as we will look at in the coming weeks, financial and commodity markets exhibit both trends.

Depending on the market, cyclical trends tend to run three to 10 years. It is the most important trend in our asset allocation process. The business cycle is the primary factor in our analysis. The business cycle is the normal tendency for the economy to move from expansion to decline, recession, recovery and back to expansion. This cycle clearly affects financial and commodity markets. Financial market conditions, monetary and fiscal policy and geopolitical events are all important contributors to cyclical trends as well.

On the other hand, secular trends can last generations. These trends tend to be driven by societal factors. For example, public attitudes toward the balance between efficiency and equality are critical as these are affected by regulatory and tax policy. Long-term geopolitical stability is mostly a factor of hegemony; if a superpower vacuum is developing or a new hegemon is emerging, secular trends can adjust. What makes secular trends important is that because they last a long time, they become part of the background, leading investors to assume that these trends never change. And so, in the early part of a reversal in secular trends, actual market performance can vary widely from what is expected. The other factor that matters in secular trends is that, unlike our stylized model, they don’t always clearly shift, causing a degree of uncertainty as to whether the change actually occurred. Only with the hindsight of history can we definitively know when and if the secular change happened. Still, we pay attention to secular trends because, at inflection points, the impact on financial and commodity markets can be significant.

Therefore, over the next few weeks, we will examine the cyclical and secular trends in commodity, equity and debt markets. In general, this analysis will offer insights into our allocation process, discussing the important cyclical elements of each asset class along with the potential impact of a change in secular trends.