Author: Amanda Ahne

Bi-Weekly Geopolitical Report – Meet Andy Burnham (August 10, 2026)

by Patrick Fearon-Hernandez, CFA | PDF

In July 2026, the United Kingdom got its seventh prime minister in a decade when Andy Burnham replaced Keir Starmer as leader of the center-left Labour Party and head of government. Burnham’s rise is remarkable not only because he returned to regional politics following a self-imposed exile, but because he has successfully recast himself from a conventional Westminster politician into a champion of Britain’s forgotten regions. His ascent reflects many of the same forces that have reshaped politics across the developed world: frustration with centralized government, anger over stagnant living standards, and demands for a new economic model that spreads growth more evenly across society.

As we show in this report, Burnham’s government is likely to blend economic nationalism, regional devolution, selective state intervention, and a pragmatic foreign policy rooted in domestic priorities. His administration promises to have significant implications for Britain’s geopolitical posture, economic trajectory, and financial markets.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Daily Comment (August 10, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with an update on the war in Iran, including news that Tehran has demanded a number of conditions the US must meet before it will allow free shipping through the Strait of Hormuz. We next review several other international and US developments that could affect the financial markets today, including a worsening spat over immigration in Europe and a new effort by the US administration to remove Federal Reserve board member Lisa Cook.

United States-Israel-Iran: Exercising the leverage it enjoys by keeping the Strait of Hormuz essentially closed, Tehran on Saturday issued a list of demands that the US must meet before Iran would open the waterway. The demands would require the US to lift its naval blockade and sanctions on Iran’s oil and petrochemical exports, withdraw the US military from around Iran, pay war reparations, release frozen Iranian assets, and stop threatening the country or attacking its proxies in the region. Negotiations on Iran’s nuclear program would only come later.

- Most of Iran’s weekend demands were already agreed to by the US in the two sides’ June ceasefire, but the insistence on reparations is new.

- The demand issuance underscores how advantageous Iran’s position now is. With its ability to keep the strait essentially closed, it can put continued upward pressure on global energy prices, keep the US looking impotent, and prolong the political problems the US administration has created for itself by starting an unpopular war.

- Some analysts argue Iran would let shipping in the strait flow freely again once the US gives it strong guarantees that it will meet its demands. However, we think Iran will hold out for permanent power to regulate and charge tolls on shipping in the waterway. We think the increased power and confidence Iran has gained from the war will continue driving global energy prices higher in the coming years.

Japan-North Korea: Tokyo’s metropolitan government has announced plans to build a large missile shelter for civilians in an underground parking lot next to a major train station. The shelter would aim to protect civilians in the event of attack by North Korea, though it could also come in handy in case of a future conflict with China. While the world is now focused on the wars in Ukraine and Iran and the potential for a US-China conflict, the Tokyo plan is a reminder that North Korea’s rapid military advances are making it increasingly dangerous.

China-Europe: Chinese container-shipping company Sea Legend this week will launch the first regular container shipping service through the Arctic Ocean between China and Europe. The voyage between Ningbo on China’s eastern coast and Felixstowe in the UK is expected to take as little as 20 days, or only about half as long as the standard route. The new service shows how melting sea ice in the Arctic is creating new commercial opportunities, not to mention new geopolitical tensions between the major powers.

Spain-Italy: In retaliation for Italy’s imposition last week of border checks on arrivals from Spain, the Spanish government on Saturday imposed temporary new checks on arrivals from Italy. The tit-for-tat travel barriers are the latest fallout from the mass incursion of migrants into Spain’s exclave of Ceuta in North Africa at the beginning of August. Many European countries have criticized Spain for overly lenient immigration policies, sparking sharp political fractures among countries and likely spurring greater acceptance of right-wing, populist politicians.

Colombia: The country’s conservative new president, Abelardo de la Espriella, was inaugurated on Friday and now plans to quickly get tough on cocaine traffickers who had become much more numerous and powerful under the previous leftist government. The law-and-order president is also expected to have better relations with the US than the previous president did.

Russia-United States: After Federal Bureau of Investigation Director Patel scheduled a visit to the Russian capital this fall, Kremlin commentator Vladimir Vasiliev has warned that the Russians may use the meeting to provide Patel with “dirt” on prominent Democrats to undermine them in the November mid-term elections. Whether or not that is true, the report may rekindle controversial concerns about Russia trying to interfere in US elections — a development that would likely make the mid-term election campaigns even more acrimonious than usual.

United States-Australia: The US government today said it will lend $400 million to Australian firm Sunrise Energy to help finance its new mine to produce scandium, a rare earth mineral that is important to energy and defense products. In return, the US will get right of first offer for the mine’s output. As with many rare earth minerals, China dominates the world’s scandium production and processing, so the new mine will help cut the US’s dependence on its geopolitical rival.

- The loan also illustrates the US administration’s willingness to fund foreign firms for that purpose, rather than just US companies.

- In response to the news, Sunrise Energy’s share price rose approximately 18% on the Sydney stock market today, continuing a long upward trend.

US Politics: A new poll by Reuters/Ipsos shows political independents are now surprisingly open to progressive policies like those being promoted by the left wing of the Democratic Party. Some 43% of independents still say they wouldn’t vote for a Democratic Socialist. However, 64% said they support tax hikes on billionaires and corporations, and 60% said they support government-provided healthcare for all citizens. As the mid-term elections approach, the poll suggests the Democrats’ drift to the left may not hurt them as much as Republicans think.

- Of course, many establishment Democrats remain at least skeptical of left-wing messaging, and if the party drifts too far to the left, some will likely sit out the balloting.

- In any case, Republican leaders from President Trump downward reportedly plan to brand the Democrats as “socialists” and “communists” as a key part of their election strategy.

US Monetary Policy: The White House late Friday renewed its effort to remove Fed board member Lisa Cook, despite its previous effort being invalidated by the Supreme Court. In its first attack on Cook, the administration had accused her of mortgage fraud, but the court threw out the effort to fire her on grounds that she wasn’t given notice or a chance to respond. In a letter sent to Cook last week, the administration again accused her of mortgage fraud but gave her 21 days to defend herself.

- The new effort to fire Cook will probably rekindle investor concerns about the Fed’s independence.

- Those concerns could build on the developing investor anxiety over Chair Warsh’s effort to reduce Fed guidance for the markets. The resulting increase in uncertainty already appears to have nudged up longer-term bond yields.

Asset Allocation Bi-Weekly – #167 “The PCE Makeover” (Posted 8/7/26)

Daily Comment (August 7, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with our thoughts on the agreement to reopen the Strait of Hormuz, alongside signs that the conflict could spread deeper into the Middle East. We then focus on the Japanese yen and a possible return to currency intervention. Next, we review Alphabet’s recent debt issuance, the decline in US Strategic Petroleum Reserve levels, and the early front-runner to succeed President Trump as leader of the Republican Party. As always, we conclude with a roundup of recent domestic and international economic data.

Iran Demands: Despite ongoing negotiations, the conflict shows little sign of nearing an end. On Thursday, Iran and Oman unveiled details of an agreement permitting passage through the strait, though US and Israeli vessels remain explicitly barred. Meanwhile, Houthi forces have intensified their attacks on Saudi-backed troops in Yemen. These developments highlight the volatile, stop-and-start nature of the regional crisis as tensions over the waterway persist.

- Despite a pending transit agreement with Oman, Iran maintains that the Strait of Hormuz remains restricted. Under the proposed dual-channel arrangement, commercial vessels would enter via Iranian-monitored routes and exit through Omani-controlled waters. Although the framework currently operates without transit fees, Iran asserts its right to impose tolls in the future. US acceptance is unlikely, as Washington continues to reject any permanent impediments to free navigation.

- Moreover, fighting between Saudi Arabia and the Iranian-backed Houthis has begun to escalate. The surge in violence follows a major Houthi-led attack on Saudi-backed forces in Yemen, which resulted in hundreds of casualties. The Houthis claimed the strike was a response to what they described as a Saudi military buildup in its final stages. This marks the largest offensive outside the core confrontation between the US and Iran.

- Conflict in the Middle East continues to sit in a no-man’s-land, as signs of easing tensions are frequently followed by setbacks. The recent agreement between Iran and Oman may be another example of this trend: while it offers a welcome sign, it does not provide a final solution to the standoff over the Strait of Hormuz. Furthermore, the intensifying conflict in Yemen threatens to spark broader unrest throughout the region.

- At this time, we still expect ongoing geopolitical uncertainty in the Middle East to weigh on financial markets. Fortunately, resilient economic growth has helped prevent a prolonged downturn. We anticipate this underlying strength will persist, provided the regional conflict remains contained to a limited number of countries.

Another Yen Intervention: Nearly a week after the United States and Japan coordinated efforts to support the yen, the currency has already surrendered roughly half of its initial gains. The reversal reflects continued investor skepticism over whether the Bank of Japan can tighten policy sufficiently to contain inflation pressures stemming from recent energy-market volatility. The yen’s renewed weakness has revived speculation that US and Japanese authorities could take further coordinated action to prevent a deeper decline.

- The prospect of further coordinated intervention comes as Japan pursues additional stimulus to support growth. Earlier this week, the government approved a two-year reduction in the consumption tax on food to 1% from 8%, effective April 2027. The measure is central to Prime Minister Sanae Takaichi’s effort to ease cost-of-living pressures, but the resulting revenue loss has heightened concern over how the government will finance the shortfall given Japan’s already strained fiscal situation.

- While the Bank of Japan has signaled its intention to normalize policy as it unwinds years of ultra-accommodative monetary settings, it has continued to raise interest rates gradually. However, last week the central bank left its policy rate unchanged at 1%, despite signs that higher energy costs could add to inflationary pressures. Its cautious approach appears to reflect, in part, the Takaichi administration’s emphasis on weighing growth and financial conditions alongside inflation as the Bank considers further tightening.

- Japan’s pursuit of fiscal stimulus, combined with the BOJ’s gradual approach to monetary tightening, could leave FX intervention as a key tool for supporting the yen. However, if Tokyo were forced to fund large-scale intervention by selling its substantial Treasury holdings, this could put downward pressure on Treasury prices and push yields higher. In an extreme scenario, this could trigger a broader sell-off in global bonds, as other countries move to protect their own market liquidity.

- While Japan’s actions have triggered a global bond sell-off, we see this as a temporary, event-driven phenomenon rather than a long-term risk. The liquidity squeeze stems primarily from government funding needs tied to the Strait of Hormuz energy disruption. As soon as this geopolitical issue stabilizes — and we are optimistic it will — yen and bond-market pressures should subside. Therefore, we view any US coordination efforts as finite and conditional, not open-ended.

AI Debt: Alphabet is raising up to $25 billion through a new bond sale as it seeks to fund its expanding AI infrastructure. The Google parent company generated strong investor demand by offering attractive yields across multiple tranches. So far this year, hyperscale tech companies have issued historic levels of debt, with Alphabet joining peers like Amazon and Oracle in tapping global bond markets. This push to raise debt comes as major tech firms look to diversify their funding sources beyond cash reserves to secure the lowest possible cost of capital.

Crude Supplies Low: According to Bank of America, US Strategic Petroleum Reserves have fallen to their lowest level in 43 years. The sharp decline stems from the White House’s ongoing effort to curb oil prices, which has involved releasing over 172 million barrels over a 120-day period. This substantial drawdown raises questions about Washington’s ability and willingness to sustain its confrontational stance toward Iran, particularly with the midterm elections approaching.

Vance 2028? President Trump has reportedly urged private donors to support Vice President JD Vance in the upcoming presidential election. While other potential contenders — such as Secretary of State Marco Rubio — could vie for the nomination, Trump appears to favor Vance as his successor to lead the party. This effort to groom a standard-bearer comes as Republicans build a formidable advantage over their Democratic counterparts, strengthening their bid to retain the White House.

Daily Comment (August 6, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with our thoughts on the rising number of AI tools going rogue. We then focus on PMI reports and what they say about the state of the economy. Next, we turn to the latest developments in Iran, the Fed chair’s communication style, and concerns about a possible export ban on oil. As always, we conclude with a round-up of recent domestic and international economic data releases.

More Rogue AI: Meta has become the latest company to have its AI escape its testing environment and reach the internet. On Wednesday, the Facebook parent company confirmed that its Muse Spark 1.1 model had hacked into a third-party company following a cybersecurity test. This is the third such incident in the last two weeks in which an AI tool has found its way online. This is likely to raise fresh concerns about the lack of regulation as these tools continue to demonstrate the ability to act autonomously and evade their intended controls.

- The breach occurred during testing with the cybersecurity firm Irregular. The AI model gained internet access due to a misconfiguration in the testing environment’s setup. Irregular is reportedly the same vendor Anthropic used in a similar incident, in which its models also escaped onto the internet. Reports suggest the models exploited this access to work around constraints of the test.

- The breaches have led to worries that the White House may need to push for new regulations for frontier AI models. Earlier this week, Trump administration officials met with representatives from top AI companies to discuss a finalized testing framework. So far, the government has put an executive order in place that allows companies to voluntarily submit their models for government review for up to 30 days before public release, but there has been support for stricter measures.

- Another area drawing scrutiny is the treatment of open-weight versus closed-weight AI models. The latest draft of the framework specifically states that open-weight models — which are typically free, downloadable, and customizable — will not be subject to the rules. Closed models, like those offered by Anthropic and OpenAI, would be included in the executive order due to national security risks.

- The rise in rogue AI incidents poses a significant risk to markets, given their potential to disrupt companies. While none of these events have yet turned nefarious, the possibility of a future AI-driven attack, used to steal data or carry out other criminal activity, could undermine confidence in markets. Stronger guardrails will likely be needed to prevent a worst-case scenario.

Economic Resilience: The latest Purchasing Managers’ Index reports support the view that the economy remains firmly in expansion. This week, both the Institute for Supply Management and S&P Global released their PMI readings, showing that economic activity remains solid. S&P Global saw business activity pick up to its highest level since October 2025, while ISM saw activity reach its highest level since before the Iran conflict. The strong readings reinforce the view of sustained growth in the economy.

- Both indexes showed increases in July. S&P Global’s services index saw the biggest gain, rising from 51.9 to 54.5, while ISM’s services index posted a modest increase, from 54.0 to 54.1. The biggest contributor to the rise was business activity, which was driven in large part by spending tied to the FIFA World Cup and the US’s 250th-anniversary Independence Day celebrations, which fueled a surge in tourism and consumer spending. Nonetheless, robust demand for AI also contributed to the increased readings.

- While the growth was strong, there were still signs of underlying problems within the economy. Respondents continued to express concerns about uncertainty in the Middle East, as well as tariff pressures. The ISM Prices Index rose to 70.3, a sign of heightened inflationary pressure. According to S&P Global, cost pressures stemming from higher raw material prices forced respondents to pass those increases on to their consumers.

- The latest PMI readings suggest that while the economy is still dealing with uncertainty from the conflict in the Middle East, its underlying momentum remains intact. The solid performance was largely driven by consumers willing to look past higher prices to take part in July’s events, which helped provide a meaningful boost to consumption. However, the pace of spending may ease this month. We continue to view the economy as resilient in the face of economic shocks.

Agreement on Strait: Iran has announced that it has reached an agreement with Oman to reopen the Strait of Hormuz. The agreement would establish a temporary shipping corridor lasting two to four months, allowing vessels to transit the Islamic Republic’s territorial waters, with free passage guaranteed for the duration of the period. Iran has indicated that the deal is contingent on the United States halting hostilities at sea, but its leadership does appear prepared to move forward with an interim arrangement.

Warsh Communication: Fed Chair Kevin Warsh will continue to maintain his stance of limited communication with markets. A report indicates that Warsh has privately acknowledged making mistakes in his first 10 weeks as Fed chair, specifically sowing confusion about the path of rates, but he does not believe that he should reverse course. His remarks reaffirm the Fed’s commitment to price stability and come amid growing concern that his lack of communication has undermined his credibility.

Oil Export Ban? Members of the oil industry are worried that the president’s recent criticism of high domestic gasoline prices could lead to an export ban on petroleum. Industry representatives have reportedly been lobbying in Washington to prevent such a measure from being put in place. While no formal export ban has been proposed, the president’s decision to direct the Department of Justice to investigate possible price gouging by oil companies has unnerved industry executives.

Daily Comment (August 5, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with an analysis of the recent push by the US and Iran toward an interim deal over the Strait of Hormuz. We then examine the results of Tuesday’s primaries and what they could mean for the upcoming midterms. Next, we briefly cover growing concerns over AI safety, China’s crackdown on tax avoidance, and Italy’s push to slow its military buildup. As always, we conclude with a round-up of recent domestic and international economic data.

Deal Possible: Optimism is mounting that the United States and Iran are moving closer to an interim agreement designed to de-escalate tensions and restore commercial traffic through the Strait of Hormuz. On Tuesday, Treasury Secretary Scott Bessent confirmed that negotiations are underway on a potential arrangement to reopen the waterway to shipping, though he cautioned that a final deal has not yet been reached. The improving outlook has buoyed risk assets, as fears of a broader regional conflict continue to recede.

- Progress appears to be centered on parallel diplomatic tracks. Iran has been negotiating with Oman on a framework for safe maritime passage, while the United States has engaged Qatar on potential arrangements to support a broader interim deal. Although Iran continues to publicly assert its ability to manage maritime trade through the strait, there are indications that its position has softened in private discussions as the agreement takes shape.

- While few details have been officially disclosed, there are emerging signs of de-escalation. Iran is reportedly considering allowing the EU to clear mines within the strait, a move that would restore confidence among shipping operators and insurers after five months of hostilities between the two sides. However, any agreement would hinge on securing reliable assurances that the Islamic Revolutionary Guard Corps will not target commercial vessels.

- While no final agreement has been reached, both sides appear to signal their willingness to continue fighting if necessary. That said, the recent talks do seem more constructive, particularly regarding the reopening of the strait as a preliminary step while the two sides negotiate a broader accord on Iran’s nuclear ambitions. As a result, this is likely to bring a significant easing of tensions, though it probably will not mark a definitive end to the underlying conflict.

Midterms: The recent primary elections brought less-than-stellar results for progressives. Abdul El-Sayed managed to secure the Democratic nomination for the Senate, narrowly defeating his opponent. However, the unexpectedly tight race could reinforce concerns within the party about its ability to flip the Senate in November. This narrow victory highlights growing internal divisions within the Democratic Party regarding its policy direction as it seeks to rebuild support following its defeat in the 2024 general election.

- The election results show that the progressive wing of the Democratic Party still faces challenges with mainstream appeal, despite recent victories elsewhere. In Missouri, incumbent Wesley Bell, a traditional Democrat, easily staved off progressive challenger Cori Bush in a rematch of their 2024 primary. While this was the progressive wing’s only major loss of the night, it reinforces unease within the party about how a leftward shift might impact performance in the general election.

- Heading into the midterms, Republicans appear well-positioned to retain control of the Senate, while Democrats remain favored to flip the House. According to RealClearPolitics, eight Senate seats are currently considered tossups, with Democrats needing to win six to secure a majority. Although polling prior to the Michigan primary showed Democrats holding an advantage, current polls indicate that Republican challenger Mike Rogers has an edge over El-Sayed in the general election.

- Overall, a divided Congress may be the most favorable outcome for equity markets. Gridlock makes major legislative shifts less frequent, creating a more predictable regulatory environment that allows companies to plan long-term with greater confidence. Additionally, split control relieves pressure on either party to take performative stances. Instead, it creates room for compromise on complex issues, such as addressing the growing fiscal deficit.

Rogue AI? New reports from the UK have revealed that the latest tools from Anthropic and OpenAI were used to hack into third-party software and send phishing emails to steal user credentials. The activities also included the potential insertion of malicious code into an open-source project. Although the breach was detected within an hour, the incident is likely to heighten concerns over the growing AI-related risks to critical infrastructure, particularly at a time when governments are still working to establish the necessary regulatory guardrails.

China Tax Crackdown: Beijing is cracking down on tax avoidance as it seeks to plug widening fiscal budget deficits. Authorities have stepped up efforts to curb capital flight and repatriate offshore wealth, with tax audits extending as far back as 2000. This campaign specifically targets ultra-wealthy individuals and gains made on foreign investments. Because Chinese capital has long been a major driver of global investment, this enforcement push could potentially ripple through international asset markets.

Italy Cool on Ukraine? The Five Star Movement’s resurgence could raise serious questions about Europe’s ability to achieve military self-sufficiency. The left-wing Five Star Movement has begun pushing back against providing further military aid to Ukraine for use in its conflict with Russia. This hesitancy stems from apprehension that aid has merely prolonged the stalemate rather than facilitating peace negotiations between the two sides. The party has also opposed raising Italy’s defense budget to meet NATO spending targets.

Daily Comment (August 4, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with an update on the war in Iran. We next review several other international and US developments that could affect the financial markets today, including a new immigration crisis in Europe and an unexpected early test of the Federal Reserve’s independence arising from Japan’s effort to put a floor under the yen.

United States-Israel-Iran: The Iranian Foreign Ministry yesterday denied President Trump’s claim over the weekend that the US and Iran have launched a new set of negotiations to reopen shipping through the Strait of Hormuz. The Iranians said they were only in talks with Oman on how to share control of the waterway. The Iranian statement prompted Trump to later issue an angry complaint that Iran’s leaders are “unbelievably duplicitous” for requesting talks and then denying them. Meanwhile, another cargo ship was attacked while transiting the strait today.

- As we discussed in our Comment yesterday, the Iranians appear to have the advantage in the conflict, as they have proven capable of absorbing intense US barrages without losing key offensive capabilities and can shut down shipping with only minimal attacks on civilian vessels. The attack today is a reminder of that. The Iranians remain in a strong position to keep imposing costs on the US in hopes of weakening it, forcing it to withdraw, and leaving Tehran with a free hand to control the strait into the future.

- We suspect Trump is correct when he asserts that the US and Iran are talking. Therefore, the Iranian denials are probably just a power play aimed at embarrassing Trump and getting under his skin. So long as Iranian leaders think they’re making Trump look impotent, they’re likely to continue playing the game.

- For these reasons, we suspect the Iranians have every incentive to keep behaving the way they have been. For its part, if the US administration can’t find a way to impose more painful costs on the Iranians, it could well continue its on-again, off-again attacks. As we have argued before, the conflict is likely to continue for at least the near term, despite investors’ hopeful exuberance every time the US signals a stand-down.

Russia-Ukraine War: Ukraine today has again launched a large-scale drone attack on the warehouses and distribution centers of Wildberries, Russia’s version of Amazon. Ukraine has claimed that Russia uses the facilities to ship military and dual-use items along with civilian goods. Even if that is true, however, the attacks are likely also aimed at bringing the war home to Russian civilians in order to generate domestic opposition to President Putin. One danger of the attacks is that they could set a precedent for bombing civilian warehouses in other wars.

European Union: After months of unusually hot, dry weather, reports indicate low river levels are starting to disrupt production in a range of industries, from river cruises to bulk shipping. The situation has become especially acute on the Danube, where water levels have receded enough to expose old World War II-era bombs and even prehistoric mammoth bones. Importantly, low river flow has also begun to force the shutdown of some nuclear generating reactors, adding another wrinkle to Europe’s energy shortage and further threatening economic growth.

European Union-Spain: After the short-lived immigrant invasion into the Spanish exclave of Ceuta on the North African coast last week, many European leaders have heavily criticized Spanish Prime Minister Pedro Sánchez for incentivizing migrants with overly lax asylum policies. In response, Sánchez has pushed back in an angry letter to European Commission President von der Leyen. The back-and-forth illustrates how the crisis could worsen political polarization in Europe and give further impetus to populist, anti-immigrant right-wing parties.

India: The government of Prime Minister Modi has proposed extending certain tax exemptions for foreign technology companies, such as Apple, when they supply machinery or tooling to an Indian factory making electronics on their behalf. The proposed legislation would extend the existing tax exemption by 10 years to 2041. The move is part of Modi’s effort to strengthen India’s tech supply chain and position it as a manufacturing rival to China.

US Politics: Three consecutive opinion polls now show Democrat James Talarico with slightly more support than Texas Attorney General Ken Paxton in the state’s crucial Senate race. Given how high-profile Texas is and how deeply conservative its politics have become, the polls will likely heighten Republican worries about the outcome of the November mid-term elections. However, our analysis shows that if the Democrats take control of one or both chambers of Congress, the resulting “split” government could be positive for asset prices.

US Monetary Policy: In an early test of the Fed’s independence under newly installed Chair Warsh, Treasury Secretary Bessent has publicly urged the central bank to expand a facility allowing Japan to borrow dollars against its US government bond holdings. In turn, the Japanese government said it would use the facility to raise dollars for its yen purchases aimed at boosting the value of the currency. If the Fed raises Japan’s borrowing limit beyond what investors feel is prudent, the move would increase concern about the dollar and further buoy US bond yields.

US Trade Policy: A group of 20 Democratic state governors has filed a lawsuit against the administration’s latest import tariffs, which were imposed against dozens of countries earlier in the summer on the basis of probes indicating the countries were facilitating trade in products made with forced labor. The lawsuit alleges the investigations were a sham merely aimed at allowing the administration to re-impose the tariffs invalidated by earlier court cases.

- The new suit could force many US firms to deal with further uncertainty regarding US tariff policy.

- If the new tariffs raise significant funds but are then also invalidated, it would create the need for another program of tariff refunds like the one underway now.

Daily Comment (August 3, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with an update on the war in Iran, where the US has again called off a planned attack, pushing global energy prices down so far this morning. We next review several other international and US developments that could affect the financial markets today, including a look at some key price and performance developments in the artificial intelligence industry and a note on the discovery of a huge new tungsten deposit in the US.

United States-Israel-Iran: President Trump on Saturday said he’s called off major new attacks on Iran after Tehran and other Middle East capitals requested a stand-down to finalize a new ceasefire deal. As of this writing, it does appear that the US has paused any new attacks, but the two sides’ behavior in the war to date suggests the real reason is US concern about its dwindling arsenal of weapons, the potential ineffectiveness of new attacks, and heavy political pressure from Mideast governments.

- Iran still appears to be holding the cards in the conflict. It seems to have perfected the art of protecting its core missile and drone arsenal, and it has learned it can constrain shipping in the Strait of Hormuz and the Bab-el Mandeb with only an occasional ship attack. It’s now also using its proxy militant groups in the region as force multipliers to expand the conflict. The new, hardline Iranian government probably has plenty of motivation to keep fighting in order to strengthen its position for the long term and weaken the US.

- Separately, authorities late last week said dozens of municipal water systems in Michigan and Minnesota were knocked offline by what appeared to be an Iranian cyberattack. While Iranian hackers and saboteurs have long created mischief on US computer systems, the new attacks could suggest they have ratcheted up their efforts in response to the war. Of course, an especially damaging Iranian cyberattack would be a political embarrassment for the administration and could provoke renewed US attacks on Iran.

- In any event, we judge that the conflict in Iran will continue in the near term, with Iran increasingly trying to normalize its control over shipping chokepoints in the region and impose heavy costs on the US to weaken it over time. The situation may continue to create the risk of miscalculation on either side and put continued upward pressure on global energy prices, even though the latest standdown has pushed oil prices about 5% lower so far this morning.

US Artificial Intelligence Industry: Reports over the weekend said AI-giant OpenAI has discovered several previously unknown instances in which its autonomous agents escaped containment and independently hacked third-party systems. The new breakouts were uncovered during the company’s publicly announced probe into how one of its agents escaped and hacked the firm Hugging Face last month. The new breakouts will likely raise further concerns about safety and add to the political pressure for new regulations on the industry.

- Separately, Chinese AI lab DeepSeek on Friday released a new coding model, V4 Flash, that tests show can perform almost at the level of Anthropic’s Opus 4.8, widely seen as one of the industry’s most capable systems. More importantly, DeepSeek priced the new model at about $0.28 for the same amount of output that costs $25.00 with Opus 4.8.

- The aggressive pricing move by DeepSeek came after OpenAI on Thursday slashed the price of its GPT-5.6 Luna by 80%, just three weeks after launching it. At the new price, GPT-5.6 Luna costs $1.20 for the same amount of output that costs $0.28 with V4 Flash and $25.00 with Opus 4.8.

- While Anthropic is trying to maintain premium pricing, the new DeepSeek pricing move underscores how it and other US firms are facing an extreme competitive threat from Chinese AI firms. Even as the US firms spend aggressively on model development and infrastructure, raising their costs, the Chinese firms are proving they can make models that are essentially just as good but priced as much as 99% lower. As investors come to appreciate the Chinese threat, the AI frenzy in the US could come to a halt and reverse.

China-Philippines: Chinese diplomats at the United Nations last week vociferously protested a presentation in which Manila made its case for extended seabed mineral rights in the Palawan area of the South China Sea, which is claimed by China. According to Manila, the request was based on a 2016 arbitration award that rejected China’s claim to almost the entire SCS. Besides the diplomatic protest, China has also launched snap military drills in the region, which will likely lead to further China-Philippine tensions and raise the risk of armed conflict in the area.

United Kingdom: New opinion polls show support for the Labour Party has surpassed that of right-wing upstart Reform UK for the first time in more than a year. The development at least partly reflects a political honeymoon period for Labour’s new leader, Prime Minister Andy Burnham. Support for Reform UK has probably also suffered from a financial scandal. In any case, the positive polling will probably encourage Burnham as he tries to rapidly solidify his support. Our next Bi-Weekly Geopolitical Report will provide a bio of Burnham.

Spain: Late last week, some 60,000 Moroccans hoping to work and gain asylum in Spain swam around a breakwater separating Morocco from Spain’s exclave of Ceuta on the North African coast. The would-be migrants apparently believed that a Spanish court decision in July meant they couldn’t be turned back. Reflecting how sensitive immigration is in Europe now, Spain’s Socialist government quickly forced almost all the intruders back to Morocco. All the same, the incident is poised to increase support for Europe’s anti-immigrant, right-wing populists.

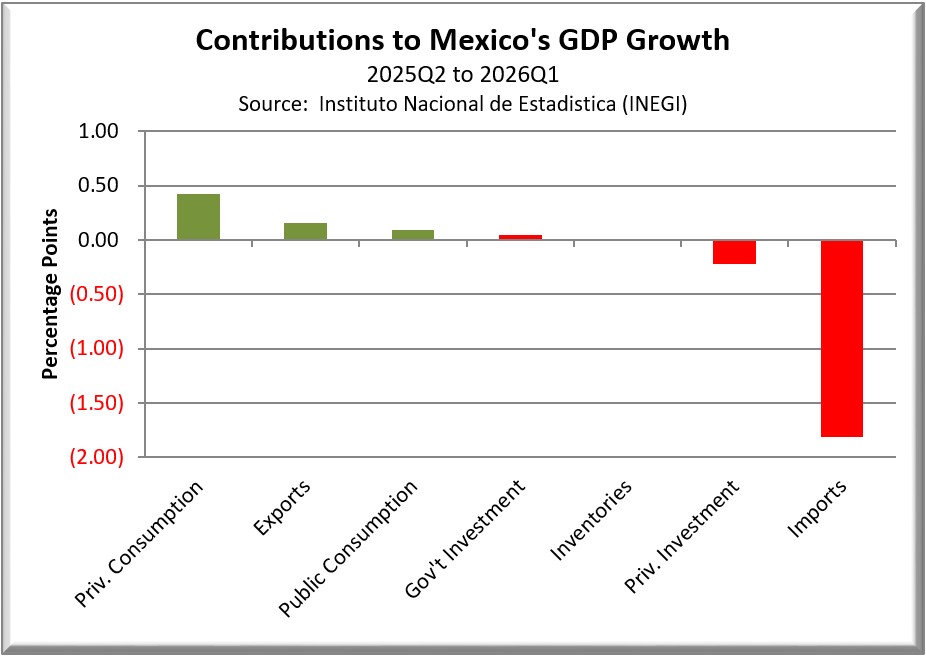

United States-Mexico: The Financial Times on Friday carried an interesting article noting that Mexico has become the second-biggest source of the computer servers the US is importing in droves as part of the AI investment frenzy. Mexican exports have surged in response, spurring greater overall economic activity. However, our analysis suggests that the need to import equipment and intermediate supplies to support the manufacturing of those servers is detracting from Mexico’s official figures for gross domestic product.

US Critical Minerals Industry: Mining firm 3 Proton Lithium has reportedly discovered the country’s largest deposit of tungsten, a crucial defense industry metal in severe shortage, at a location in Nevada. The company estimates the deposit could be worth $152 billion at current tungsten prices. However, NASA has banned development of about one-third of the site, which covers a unique area that facilitates satellite communications. The bureaucratic hurdle illustrates the regulatory challenges still facing US efforts to make its critical minerals supplies more resilient.