Author: Amanda Ahne

Daily Comment (May 26, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with an update on the Iran war, where the optimism over a potential new peace deal late last week has started to give way in the face of new US attacks on Iran’s military over the last 24 hours. We next review several other international and US developments that could affect the financial markets today, including new data showing that rising prices are starting to push down consumer purchasing power around the world and new research indicating that deregulation has opened up huge new lending opportunities for US banks.

United States-Israel-Iran: Despite statements late last week by President Trump and other US and Iranian officials indicating a 60-day ceasefire extension was in the works, the president, starting on Saturday, suggested the deal could still take several days to be finalized. Of course, the hints of a new deal could be mostly political posturing as in the past. It would not be a surprise if no deal materializes this week. The US yesterday also launched attacks on Iranian missile sites and mine-laying boats, further undermining hopes for a more permanent end to the fighting.

- In any case, the key point is probably that even if a peace deal is struck, normalizing global energy and commodity flows in the Middle East would likely take a year or more. That suggests global energy and commodity prices are likely still at risk of further increases, which would potentially weigh on economic growth around the world, drive government bond yields even higher, and cause important political implications.

- Separately, Israeli Prime Minister Netanyahu ordered his military to step up its attacks on the Islamist militant group Hezbollah in southern Lebanon. The move came after far-right members of Netanyahu’s cabinet demanded a full-scale resumption of Israel’s offensive there in defiance of the US administration’s preference that they stand down to support the current US-Iranian ceasefire.

- While global oil prices had fallen sharply into the weekend on hopes for a peace deal, the new US strikes on Iran and Iranian threats to retaliate have given a boost to oil prices this morning. Near futures prices for Brent crude are up some 2.9% so far today to about $96.20 per barrel.

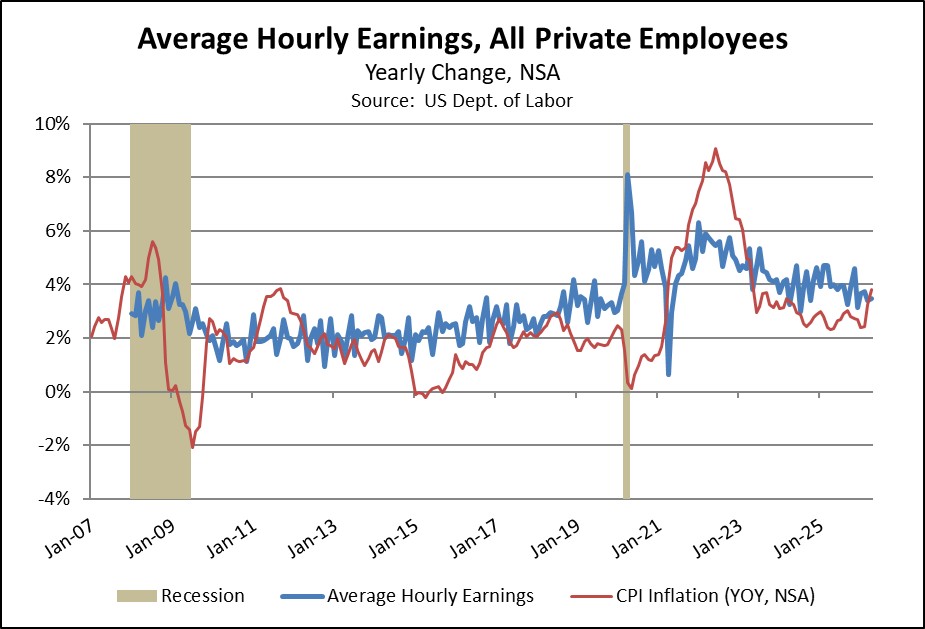

Global Labor Market: An article in the Financial Times today notes that spiking prices for energy and other commodities are threatening to cut the total purchasing power of workers around the world. In the US, for example, we have noted that the consumer price index in April was up 3.8% from the same month one year earlier, while average hourly earnings were only up 3.5%. The FT article notes that the trend is moving in the same direction in economies such as the UK and the eurozone, which will likely weigh on growth and asset values.

European Union-China: Five key EU countries have signed a paper calling for the bloc to respond more aggressively to “systemic and structural industrial overcapacity,” a phrase that is often taken as shorthand for China. The paper by the Netherlands, France, Spain, Italy, and Lithuania illustrates how the EU is increasingly riven by disagreements over whether to engage more closely with Beijing to offset a fraying US relationship or erect strong trade barriers to protect domestic industries.

- The issue will be discussed at an EU summit on Friday.

- For investors, the risk is that if trade and investment flows between the EU and China remain relatively unfettered, EU companies could gradually be weakened, even if they preserve some economic opportunities in the short term. However, tougher trade and investment barriers could lead to a trade war that results in immediate disruptions.

United States-Japan: The US has reportedly warned Japan that its purchase of 400 Tomahawk cruise missiles will be severely delayed as Washington works to rebuild its depleted arsenal after the Iran war. Japan’s Tomahawk purchase was meant to give it advanced strike capabilities and help it defend itself against China while it worked to develop its own missiles. The delay will likely spur Japan to redouble its missile development efforts, potentially giving further impetus to its expanding defense industry and creating new investment opportunities.

United Kingdom: New data yesterday said bank lending to non-financial companies fell to 59% of the UK’s GDP in the third quarter of 2025, marking the lowest level in almost 30 years. The figures were especially weak for lending to small- and medium-sized firms. The reduced bank lending reflects both weak economic growth and tougher bank regulation.

Indonesia: In a little noticed announcement last week, President Prabowo said the government will take control of the country’s major commodity exports. The first two commodities brought into the plan will be coal and palm oil. By taking the control of foreign commodity sales away from legions of middlemen, Prabowo’s goal is to curb tax evasion and improve efficiency. However, few details have been released, leaving producers and current middlemen unsure of how to proceed.

US and UK Banking Industries: New research by consultancy Alvarez & Marsal has found that deregulation allowed major banks in the US and UK to expand their balance sheets by a cumulative $1.3 trillion over just the last two quarters, giving them a significant leg up on their more constrained rivals in the eurozone and Switzerland. The figure illustrates the under-appreciated impact of recent reforms in the US and UK, which should be supportive of those countries’ bank stocks.

Daily Comment (May 22, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with our perspective on why lawmakers are struggling to regulate AI. We then examine the latest developments in the US-Iran conflict. We also briefly address the spread of the Ebola outbreak to additional countries, the US’s decision to delay certain weapons sales to Taiwan, and early indications that governments are moving to reassure bond investors. As always, we conclude with a comprehensive roundup of the latest international and domestic economic indicators.

Rising AI Pushback: Lawmakers are still struggling to balance the push to promote AI with the need to protect their communities. On Thursday, the president chose to delay the signing of an executive order that would have imposed stricter oversight on the development of AI tools. He is far from the only official wrestling with how best to regulate the technology, yet his hesitation underscores how optimistic government officials remain about AI’s potential benefits. Even so, growing unease among voters is starting to pressure lawmakers to act.

- One factor behind the postponement appears to be divisions within the White House itself. Treasury Secretary Scott Bessent has taken a leading role in advocating for rules to govern AI in the wake of Mythos, which has demonstrated an ability to expose vulnerabilities in the nation’s core infrastructure and financial system. He has been pressing the national security team to move more quickly to put these guidelines into place.

- On the other hand, there are also concerns that imposing too many rules could leave the United States at a competitive disadvantage to China in the AI race. This camp, reportedly led by National Cyber Director Sean Cairncross, has sought to slow the process, arguing against new regulations without a clearer sense of the potential costs. To bridge the divide, officials have pushed for more feedback from outside the White House on how prospective rules might affect both the private and public sectors.

- Public debate over AI regulation is intensifying just as public sentiment toward the technology begins to deteriorate. Opposition to new data centers has been particularly strong in parts of Texas, which now hosts the largest facility of its kind globally. Concerns range from noise and environmental impact to significant energy consumption, with surveys indicating that these projects rank among the least popular local developments.

- While AI continues to exhibit strong momentum, it is likely to encounter increasing political and regulatory headwinds. We suspect such resistance could moderate the pace of earnings growth these firms have recently delivered and potentially weigh on investor sentiment toward the sector. In this context, we continue to advocate maintaining some exposure to value as a potential buffer against a shift in market momentum.

Iran Deal Close? There are growing signs that the US and Iran are moving closer to a potential agreement that could lead to the reopening of the Strait of Hormuz. Iranian officials have signaled that the latest US proposal has helped bridge key gaps between the two sides as indirect negotiations continue. Remaining points of contention appear to center on Iran’s right to uranium enrichment and the authority to impose transit tolls. While talks are still ongoing, the prospect of a deal has begun to ease market tensions as participants await further clarity.

- Signs of progress come as Iran approaches the US deadline for potential strikes within the next few days. Earlier this week, the president warned that an attack was under consideration but extended the timeline following pushback from Middle Eastern countries concerned that they could become targets in the event of a strike on Iran. However, Trump indicated that military action could begin as early as this weekend.

- On Friday night, a UAE power plant was targeted in a drone attack launched from Iraq, forcing the facility to rely on backup generation to avoid broader disruptions. Although Iran did not claim responsibility, the incident is widely viewed as a signal of the potential escalation risks should the US resume military action.

- The prolonged duration of the conflict is beginning to exert a more pronounced drag on the economy. The latest ISM report shows a sharp rise in inventory accumulation, suggesting that demand pressures are broadening. As firms compete more aggressively for limited inputs, this dynamic could contribute to more persistent inflationary pressures and further weigh on global economic growth.

- While signs of progress in the conflict are encouraging, a resolution does not appear imminent, as neither side appears willing to make meaningful concessions. Meanwhile, rising inflationary pressures are likely to weigh on bond prices, prompting investors to reduce duration exposure. In this environment, private credit and business development companies could benefit from their floating-rate structures, particularly as default rates and spreads remain relatively contained.

Ebola Outbreak: Concerns are growing that the Ebola outbreak could spread across Africa. While currently confined to the Democratic Republic of the Congo and Uganda, experts fear the virus may reach three additional countries on the continent. The situation remains critical, with over 500 confirmed cases and 150 fatalities reported to date. Although there is no evidence that the outbreak has reached other continents, international medical response is active; notably, one American citizen is currently receiving treatment for the virus in Germany.

Taiwan Sales on Ice: The Pentagon has informed Taiwan that it will delay certain weapons sales amid the conflict in Iran. While officials maintain that US stockpiles are sufficient, the move reflects a desire to preserve readiness ahead of potential escalation. It may also signal an effort to avoid straining ties with China as Washington seeks Beijing’s support in easing Middle East tensions. That said, the decision could encourage Asian nations to further diversify their defense supply chains.

Bond Yields Ease: Japanese and UK bond yields have eased amid signs that policymakers may act to address supply-demand imbalances. In Japan, the Ministry of Finance has signaled a reduction in long-duration issuance. In the UK, potential Labour challenger Andy Burnham has indicated he would maintain existing fiscal targets if he were to replace Prime Minister Keir Starmer. We expect continued bond market pressure to push governments toward policies aimed at containing further increases in yields.

Note: Due to the holiday, the Comment will not be published on Monday.

Daily Comment (May 21, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with our assessment of the latest Fed meeting minutes and their implications for incoming Chair Kevin Warsh. We then examine the political backlash stemming from the energy crisis and how Europe is attempting to manage it. We also briefly touch on Nvidia’s earnings, the US indictment of former Cuban president Raúl Castro, and early signs that the EU is building out its security industry. As always, we provide a comprehensive roundup of the latest international and domestic economic indicators.

Hawkish Fed: The April 28-29 FOMC meeting minutes suggest policymakers were more open to the possibility of additional rate hikes than the official statement implied. Participants also expressed ongoing concern about the economic and inflationary risks associated with the conflict in Iran. At the same time, some members favored preserving optionality for future rate cuts, noting that the labor market has yet to demonstrate clear, sustained strength. This divergence will likely complicate the efforts of incoming Fed Chair Kevin Warsh to develop a consensus on policy.

- Overall, the meeting minutes seemed to suggest that hawks may be in the driver’s seat. While the recent Fed announcement showed that three officials dissented in favor of dropping an easing bias in the statement, the minutes revealed that a majority of members believed that “policy firming” would be appropriate if inflation were to persistently run above the Fed’s 2% target.

- However, there did seem to be at least some openness for a rate cut. The minutes revealed that one member, outgoing Fed Governor Stephen Miran (the only dovish dissenter) had argued for a rate cut to help address fragility in the labor market. While he stood alone in that specific effort, other members expressed support for possible rate cuts in the future if inflation were to return to its downward trajectory.

- Given the ongoing concerns about the Middle East, Warsh will have limited time to make the case for easing policy. Before his confirmation, he argued that the Fed should incorporate AI‑driven productivity gains into its framework and was explicit about his openness to lower rates. But his claim that “inflation is a choice” and criticism that the Fed has drifted from its price‑stability mandate could complicate that effort, given lingering concerns about his independence from the White House.

- The Fed is not on a preset path and will likely seek clearer confirmation before moving rates in either direction. While some FOMC members may be open to further tightening, we think the committee will ultimately favor keeping rates steady, particularly given the political backdrop. If inflation stays elevated, longer‑duration bonds could see continued volatility, though we still expect 10‑year Treasury yields to trade broadly range‑bound around the mid to low 4% area.

Hormuz Unrest: The energy shock stemming from the standoff in the Strait of Hormuz is fueling rising political tensions across a number of countries. Governments have tried to calm nerves over potential shortages of energy and, in some cases food, to contain public anxiety. While political pushback in most developed economies remains limited for now, several emerging markets are already showing how severe the fallout could become if conditions do not improve.

- More governments are weighing measures such as stockpiling and price controls to avert a potential food crisis. Recent reports indicate that the EU is exploring the stockpiling of fertilizer to safeguard future harvests and reduce the risk of shortages. Likewise, the UK has floated temporary caps on select staple foods to help ease the pressure from the increasing costs of living on households.

- Rising political risks also appear to be pushing the EU, in particular, to soften its stance toward both the US and Russia. In an effort to avoid an escalation in trade tensions that could further weaken its economic outlook, EU leaders have finally agreed to put the US trade deal to a vote next month. At the same time, Brussels is seeking a more prominent role in talks with Moscow, positioning the EU to pursue a resolution to the conflict even in the absence of direct US involvement.

- Although risks remain elevated, there are signs of a broader push to finally resolve the Strait of Hormuz standoff. While US-Iran negotiations are ongoing, recent developments suggest both sides may be edging closer to an agreement. At the same time, several Middle Eastern producers are investing in infrastructure to reduce their reliance on the strait. For example, the UAE has indicated that a new pipeline project designed to roughly double its export capacity is already about halfway complete.

- We see a risk that the Strait of Hormuz crisis could spill over into broader global instability and potentially trigger a new migration wave, though this is not our base case. We remain cautiously optimistic that a deal can be reached in the coming weeks to reopen the strait and ease pressure on energy and commodity markets. In that scenario, we would expect European equities to be among the main beneficiaries, given their sensitivity to energy prices and vulnerabilities to rising geopolitical risks.

Nvidia Earnings: The world’s largest chipmaker and key bellwether for the AI boom beat expectations in the first quarter. The company reported revenue of $91 billion, ahead of the $87 billion consensus estimate. On the earnings call, CEO Jensen Huang highlighted that the firm is broadening its revenue base beyond data centers to areas such as robotics and autonomous vehicles, underscoring how AI demand is expanding beyond core infrastructure.

Castro Indictment: The US has indicted former Cuban President Raúl Castro over the 1996 incident in which two civilian planes were shot down, marking a significant escalation in Washington’s approach to Havana. In our view, this move fits into a broader effort to pressure authoritarian leaders in the region and, more broadly, to reassert a modern version of the Monroe Doctrine — what some have dubbed the “Donroe Doctrine” — as the US seeks to counter rival powers in its hemisphere.

European Defense: In a further sign of rising European defense outlays, Germany has acquired a 40% stake in tank maker KNDS. The move should help strengthen Europe’s domestic armored‑vehicle industry while reducing the region’s reliance on US defense capabilities. We continue to see European defense as a key structural growth area as governments assume a larger share of their own security burden.

Bi-Weekly Geopolitical Podcast – #87 “The Trade Trilemma Revisited” (Posted 5/21/26)

Daily Comment (May 20, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with our views on how rising bond yields are creating new openings in the market, including in private credit, followed by an update on intensifying tensions in Iran. We also cover increasing Congressional scrutiny of Middle East policy, the US troop drawdown in Poland, and the impact of AI on the labor market. As always, we provide a comprehensive roundup of the latest international and domestic economic indicators.

A New Hope: There is a global sell-off in bonds as markets grapple with rising deficit spending and persistent inflation. On Tuesday, the 10‑year US Treasury yield climbed to its highest level in 19 years, while yields in Japan, the UK, and France also rose to multi‑year highs. The move reflects investors stepping back from sovereign debt amid mounting concerns over fiscal sustainability and the cost of funding measures intended to cushion the impact of higher rates. However, the rising uncertainty may prompt a rethink of private credit.

- In the US, the rise in yields reflects investors grappling with several mounting risks at once. A combination of war‑related energy shocks feeding inflation, large fiscal deficits, and a still‑resilient economy has led markets to demand a higher risk premium on government debt. This, in turn, has fueled concerns that the Federal Reserve may need to keep interest rates at current levels for even longer.

- For the rest of the world, concerns center more on expanding fiscal spending alongside a potential slowdown in growth. Governments across Europe and Asia have begun rolling out energy subsidies to help households cope with higher prices. To finance these measures, they are expected to issue additional debt, prompting investors to demand higher compensation to absorb the increased supply.

- However, there have been some clear winners. Rising bond yields have fueled a renewed bid for the AI trade, which investors increasingly view as a relative haven amid higher interest rate expectations. This rotation has supported markets with heavy technology exposure — most notably US large-cap equities, but also South Korea and Taiwan, which remain key exporters of components critical to AI infrastructure.

- Additionally, private credit sentiment may also improve meaningfully as software companies have staged a notable rebound. Software issuers that were effectively written off earlier in the year on “going concern” fears tied to AI disruption are now beginning to stabilize. In particular, large platforms such as ServiceNow, Workday, and Salesforce — initially caught up in the “SaaSpocalypse” narrative — have posted a marked recovery over the past several weeks.

- While higher interest rates create headwinds for the global economy and select sectors, we still see areas that are compelling for investment. AI‑linked equities, though crowded, continue to deliver strong performance. At the same time, private credit and business development companies (BDCs) look attractive in this environment, supported by their floating‑rate debt exposure, meaningful links to a recovering software sector, and the recent re‑rating of many software names.

New Conflict: President Trump has warned that time is running out for Iran to reach an agreement before he authorizes additional strikes. The threat comes as both sides continue to spar over the terms for reopening the Strait of Hormuz. In a show of defiance, Iran has said it is prepared to defend itself against any attack. The growing impasse has prompted regional and global powers to take a more active role in mediating the conflict, while global markets brace for a resolution.

- The president’s latest threat came after he said he had received assurances from China that it would not supply weapons to Iran. His remarks referenced last week’s meeting with President Xi, in which the two leaders discussed issues ranging from trade and intellectual property to AI and foreign policy. President Trump suggested those talks also included a commitment from Xi not to provide arms to Tehran.

- As the president prepares additional measures against Iran, he appears to have helped nudge NATO toward considering a larger role. The alliance has reportedly discussed deploying naval forces to the strait if it remains closed into early July. While there are still no clear signs of the unanimous backing required for such an operation, the debate itself suggests momentum is starting to move in that direction.

- The growing involvement of additional countries has increased the risk that the conflict could widen beyond Iran. China’s role raises the prospect of the war evolving into a proxy confrontation with the United States, potentially driving a further deterioration in bilateral relations if tensions escalate. At the same time, possible NATO involvement could draw European states more directly into the crisis, adding another layer of complexity and heightening the risk of broader regional instability.

- In a world where conflict risks are rising, we expect these conditions to favor hard assets and broad-based increases in defense spending. Precious metals look particularly appealing as non‑US‑aligned countries, including China, seek to hedge their exposure to the dollar. Defense companies, especially in Europe, may also benefit as governments are forced to shoulder a greater share of their own security burden.

Congressional Pushback: There is growing pressure in Washington to bring the US standoff with Iran to an end. On Tuesday, Republicans joined Democrats in clearing a key procedural hurdle that paved the way for a final vote on a resolution to halt the war in Iran. The bipartisan push reflects the conflict’s increasing political unpopularity and could complicate the president’s efforts to secure further concessions from Tehran. That said, we think any such bill is unlikely to become law and will remain largely symbolic.

US Withdrawal: The US military has begun reducing its troop presence in Europe as it seeks to recalibrate its foreign policy posture. This week, Washington canceled the planned deployment of 4,000 troops to Poland, bringing the regional force level back toward its pre‑Ukraine‑invasion baseline and signaling a White House push for Europe to lessen its dependence on US security guarantees. In our view, this shift is likely to spur higher EU defense spending as European governments move toward greater self‑reliance in defense.

AI Job Displacement: A growing number of technology and financial firms are turning to AI to streamline operations and reduce headcount. Standard Chartered’s CEO, for example, has signaled plans to cut nearly 8,000 roles as the bank seeks to eliminate redundancies, while Meta has pursued similar reductions in the name of efficiency. So far, AI‑related layoffs have been relatively contained, but the acceleration of investment in automation raises the risk that job cuts could broaden into other sectors over time.

Asset Allocation Bi-Weekly – #162 “The Power of Gold” (Posted 5/20/26)

Daily Comment (May 19, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with a short update on the war in Iran. We next review several other international and US developments that could affect the financial markets today, including a report of stronger-than-expected economic growth in Japan in the first quarter and several items on the US artificial intelligence and energy industries.

United States-Israel-Iran: President Trump yesterday said he’d delayed a plan for new military attacks on Iran today at the request of leaders in the Middle East. According to Trump, the delay was justified because Iranian leaders have finally entered into “serious negotiations.” However, the US has now gone through several cycles of ultimatums and threats followed by backdowns, so the latest retreat could increase investor concern that the US is having no success convincing the Iranians to reopen the Strait of Hormuz to shipping.

- If so, the continued disruptions to global energy and commodity supplies are increasingly likely to spark a fresh spike in price inflation.

- In turn, that is likely to keep undermining bond values, driving up yields, while also increasing the risk of a pullback in stock prices.

Japan-South Korea: In a summit meeting today, Japanese Prime Minister Sanae Takaichi and South Korean President Lee Jae Myung agreed to a broad program of cooperation geared at shoring up their energy supplies. The program includes joint reserves of crude oil, shared supplies of critical refined products, such as jet fuel, and swap arrangements for liquified natural gas. Besides pointing to improved Japanese-South Korean relations as the two nations face bigger external threats, the program also highlights their vulnerability to energy supply shocks.

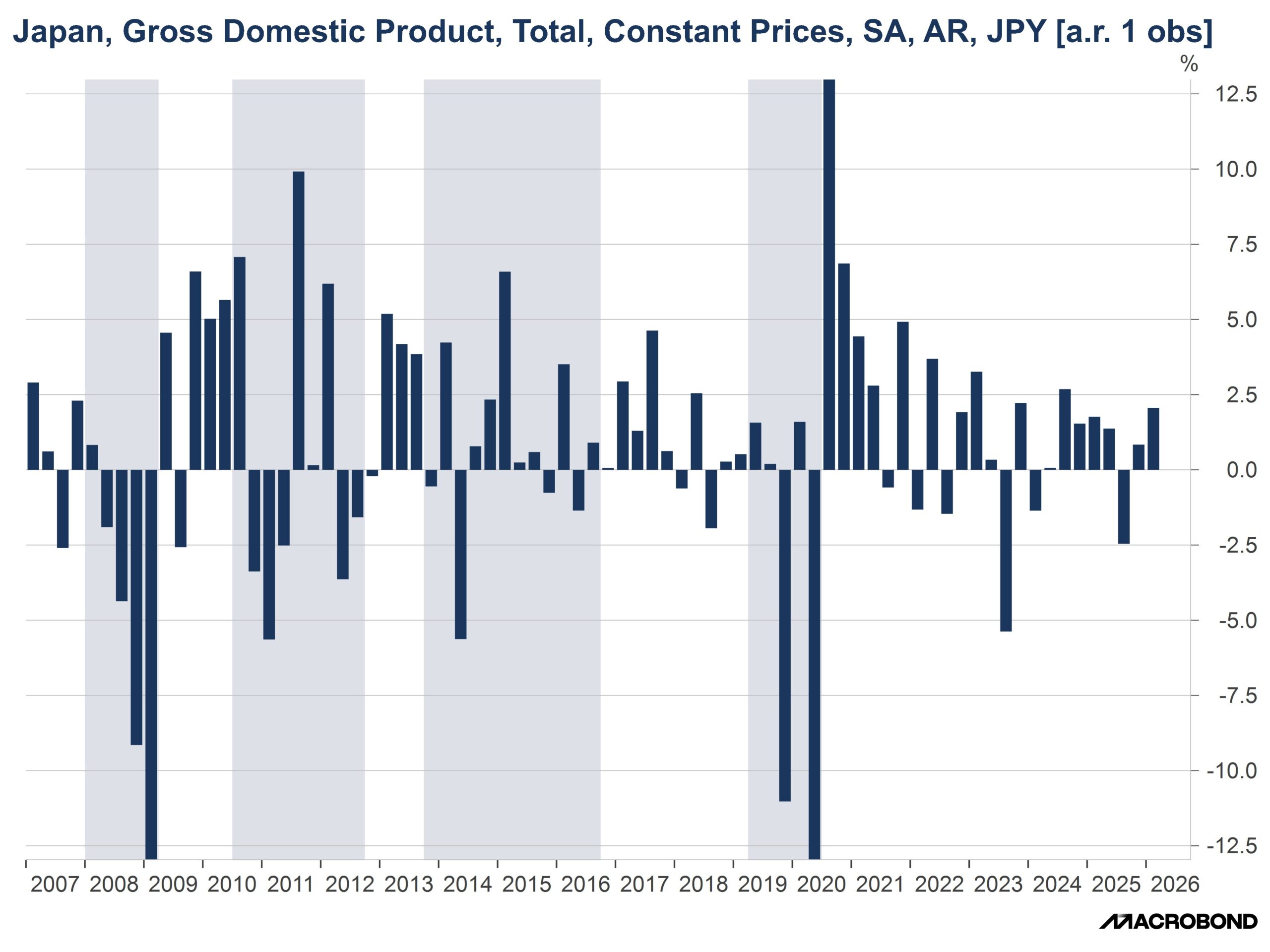

Japan: Excluding price changes and seasonal impacts, first-quarter gross domestic product grew at an annualized rate of 2.1%, far better than the anticipated increase and more than double the revised 0.8% growth rate in the previous quarter. The strong growth came mostly from surprisingly robust increases in personal consumption spending and international trade. Coupled with continued high price inflation, the GDP figure will likely help prompt the Bank of Japan to keep raising interest rates, perhaps explaining why Japanese stocks have declined on the news.

China-Russia: General Secretary Xi today will host Russian President Putin for a summit in Beijing, with much media expectation that the two leaders could sign a deal on the proposed Power of Siberia 2 natural gas pipeline, which would channel some 50 billion cubic meters of Russian gas to China each year. The leaders last year agreed to move forward with the design of the pipeline, which is a priority for Putin, but Xi is driving a hard bargain on the price of the gas and appears reluctant to make a long-term commitment as he develops China’s other energy sources.

- If Xi and Putin reach a deal on POS 2, the Chinese and Russian economies would be even more tightly integrated, replacing some of Russia’s prior focus on supplying energy to Europe and reducing China’s reliance on energy shipped through the Strait of Hormuz.

- Longer term, if Russia’s war against Ukraine ends and the Europeans want to buy more energy from Russia again, any deal for POS 2 could divert supplies that would otherwise be available for Europe.

China: In an interview with the Financial Times, the CEO of Tianqi Lithium, one of China’s biggest lithium producers, warned that even the most bullish investors were underestimating the likely demand for the mineral as battery power is applied to more industries. For example, the CEO discussed how batteries will be increasingly used in trucking, mining equipment, and ships. The CEO, Frank Ha, may well be “talking his book,” but his statement does highlight how the demand for batteries is booming (see note below regarding Ford’s new battery business).

France-Sweden: The Swedish government today selected France’s state-owned Naval Group to build four new frigates aimed at helping modernize the Swedish navy. The losing bidders were a joint effort by the UK’s Babcock International and Sweden’s own Saab and a group led by Spain’s Navantia, both of which offered newly designed vessels. Importantly, Stockholm said it awarded the contract to Naval Group because its FDI frigates are already in service with France and Greece.

- As European militaries rush to rebuild and modernize amid increasing threats from Russia and growing US reluctance to support the Continent’s defense, we continue to believe that international defense stocks are likely to perform well into the future.

- Because of today’s revolution in defense technology, including new weapons such as drones and hypersonics, much of the opportunity will likely come from start-up “defense tech” companies after they hold their initial public offerings. In the meantime, the Swedish deal shows how established defense firms with tried-and-true weapons systems will also benefit in the near term.

US Artificial Intelligence Industry: Bucking the enthusiasm for AI investments among many technology executives, the CEO of storage disk maker Seagate Technology yesterday said his firm won’t meet surging data center demand because new factory buildouts would take too long and risk future overcapacity. In response, Seagate’s stock price plunged 6.9%. We think the statement could signal the beginning of increased capital discipline and caution against the current AI frenzy. If so, it could portend a correction in tech prices in the future.

US Electricity Industry: While most investors yesterday focused on the announcement of a major AI-driven merger of electricity utilities NextEra and Dominion, we found it just as notable that Ford Motor Company has launched a new unit to build large-scale industrial batteries. In fact, the firm announced yesterday that it has struck a deal to provide up to 20 gigawatt-hours of battery energy storage capability over five years to power company EDF. Together, these transactions illustrate how the AI boom continues to spark new electricity investment and innovation.

US Stock Market: According to the Wall Street Journal today, stock buybacks by the six Magnificent 7 firms that have reported first-quarter earnings so far were down 71% from their level one year earlier. The article posits that Nvidia, the last of the Mag 7 companies to report, could buck the trend with an increase in its buybacks.

- Still, the overall figures illustrate how increased capital investment due to the AI boom is affecting the financial position of top tech firms.

- Importantly, fewer stock buybacks will be a headwind for earnings per share growth, potentially weighing on the major tech firms’ valuations.

Bi-Weekly Geopolitical Report – The Trade Trilemma Revisited (May 18, 2026)

by Thomas Wash | PDF

In February 2026, the United States Supreme Court struck down the import tariffs imposed by the Trump administration in April 2025 under the International Emergency Economic Powers Act (IEEPA), eliminating the import charges that had been applied to specific countries but leaving in place those imposed on certain products. While the White House is now working to replace those tariffs to ensure that countries follow through on the trade deal commitments they made over the last year, the time that these tariffs have been in place has helped shed light on their overall impact.

In 2025, we wrote a report called “The Tariff Trilemma,” in which we focused on three types of tariffs — reciprocal, revenue, and restrictive — and their respective trade-offs and purposes. Now that these tariffs have been in place for over a year, we have actual data to assess how the administration’s trade policies have affected the economy and what they may mean going forward, even after the Supreme Court ruled the IEEPA tariffs unconstitutional.

This report briefly reviews the three different types of tariffs and what sets them apart. We then focus on how these tariffs have changed trade flows, investment spending, and domestic inflation. We also discuss the impact of trade on financial markets, including domestic and international equity markets, global currencies, and interest rates.