by Thomas Wash | PDF

You never really appreciate a good thing until it’s gone. May 15 will be the final day in office for Federal Reserve Chair Jerome Powell, one of the most effective consensus builders in Fed history. Despite an extraordinary series of shocks during his tenure — from the 2019 repo market turmoil and the COVID‑19 pandemic to Russia’s invasion of Ukraine, the collapse of Silicon Valley Bank, new tariffs, and most recently the war in Iran — Powell’s ability to forge agreement on policy has stood out during the most aggressive hiking cycle since the Volcker era. It will likely be more difficult to sustain such unity when rates begin to ease.

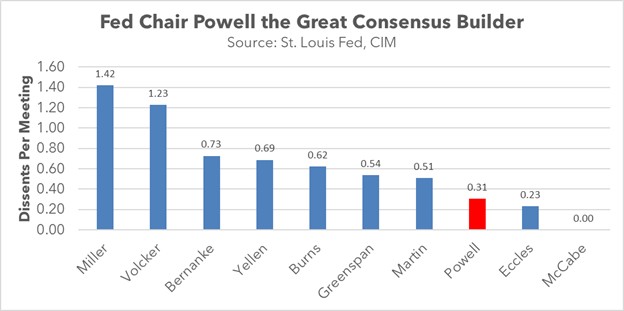

Despite the controversy surrounding the Fed’s characterization of post‑pandemic inflation as “transitory,” Powell has still been able to set policy with near‑unanimous support on the FOMC. His ability to forge consensus is even more striking when set against that of his immediate predecessor. Based on available FOMC voting data, only two Fed chairs — Marriner Eccles and Thomas McCabe (who only served roughly three years as chair, 1948-1951) — have recorded fewer dissents per meeting.

While disagreements among policymakers were evident in speeches, projections, and occasional dissents, those differences were never significant enough to keep most members from ultimately backing major policy moves. That cohesion is all the more striking given the unusual amount of changes under Powell’s more than eight years as Fed chair, during which the Fed introduced a range of new liquidity facilities — both temporary and standing — to address and prevent bank runs, raised rates from the effective lower bound to their highest levels in over two decades, and oversaw a sharp expansion followed by a significant reduction of the Fed’s balance sheet.

The lack of dissent has likely helped provide markets with greater clarity on the overall direction of policy, even as investors have continually repriced the size and timing of moves in response to incoming data and Fed communications. While expectations for the magnitude of individual rate changes have fluctuated, the broad directional signal from the FOMC has generally remained aligned with subsequent policy decisions.

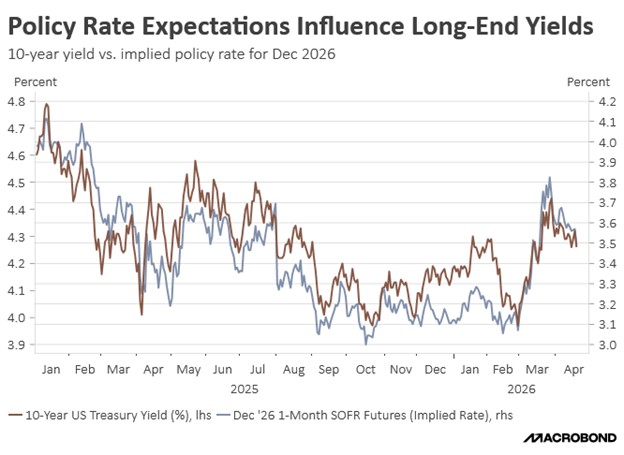

This relative certainty has made it easier for the Fed to influence long‑term interest rates by shaping expectations for the path of short‑term rates, particularly through its guidance and published projections. That influence is evident in the close co‑movement between pricing in overnight policy‑rate futures and the 10‑year Treasury yield over recent cycles, even though other factors such as term premia and global risk sentiment also play an important role.

Powell’s ability to build consensus is closely tied to the nature of the crises that defined his tenure and the clarity they gave to the Fed’s mandate. In the early phase of the pandemic, lockdowns and a sudden collapse in activity and employment made the case for cutting rates to near zero and deploying emergency tools to support a severely stressed labor market. Later, the need to raise rates was driven by an unprecedented surge in inflation that posed a direct threat to price stability, giving the FOMC a strong shared rationale for an aggressive tightening campaign.

Powell’s named successor, nominee Kevin Warsh, is likely to find it much harder to limit dissents if he pushes for the deeper rate cuts that he has argued will support the AI buildout. Even though the Fed has already begun lowering rates, its inability to return inflation to its 2% target for more than five years has heightened concerns about moving too aggressively. The war in Iran further complicates the outlook, as renewed supply chain disruptions and higher energy prices are already showing signs of adding upward pressure to inflation.

As Powell departs the chair position and potentially the Board of Governors as well, bond markets are likely to face more volatility if Warsh were to press for rate cuts while inflation remains elevated. In our view, there is ample evidence that many FOMC members are prepared to resist cuts they see as unwarranted when inflation is drifting higher, a dynamic that could translate into greater instability in longer‑duration Treasurys as investors grapple with a less predictable policy path. By contrast, if inflation resumes a clear downward trend, Warsh’s job of building consensus could become much easier, allowing the Fed to retain meaningful influence over longer‑term yields.

View PDF

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify