by Patrick Fearon-Hernandez, CFA | PDF

Since the launch of the US-Israeli war against Iran on February 28, if there’s been one dramatic feature, it’s that the conflict and official statements about it have shifted dramatically almost on a daily basis. By the time this report is published, the war could be going in a wholly different direction from when we started writing it. Nevertheless, we do think we can make some predictions about how the conflict will affect the global economy over the long term. One such prediction touches on how corporate behavior may change in the future. Specifically, we think the war will spur companies to once again embrace high inventories to shield themselves against supply disruptions and associated price jumps. A broad return to higher inventories will likely have important implications for corporate profitability, facility-site decisions, and stock valuations.

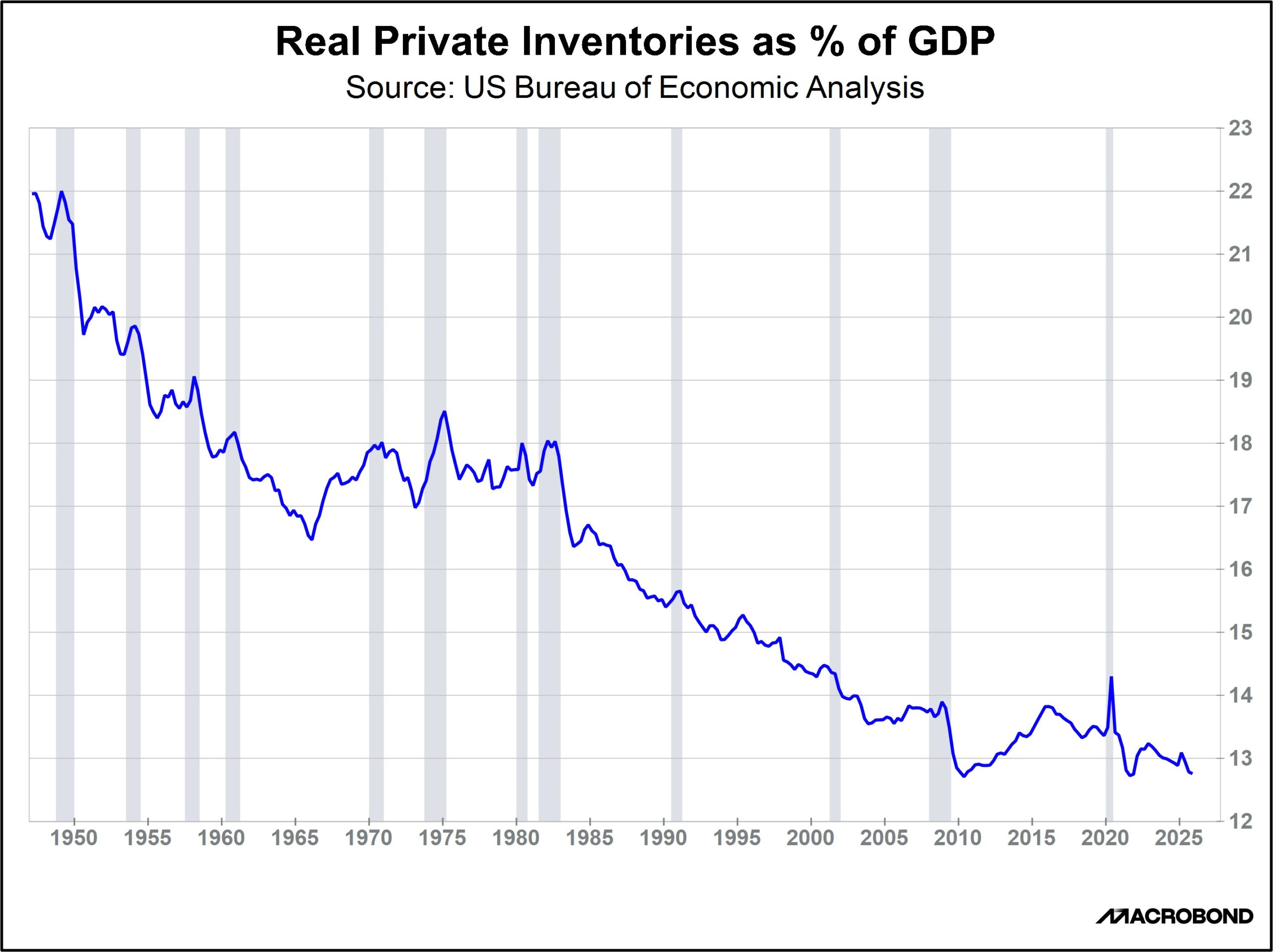

The chart above shows the inflation-adjusted value of US private sector inventories as a share of gross domestic product (GDP) since the end of World War II. Clearly, the overall trend has been for companies to hold less inventory compared with their sales. What explains this? We believe many factors are responsible. For example, the extremely high inventories around World War II and the Korean War probably reflected hoarding at a time of limited consumer sales. Inventory holdings would have naturally fallen as the end of those conflicts allowed for normalized supply dynamics and rebounding consumer spending. At the same time, innovations in transportation quickened delivery times and reduced freight costs, while the information technology revolution improved the ability of firms to optimize inventory holdings. And, as we’ve argued many times before, the end of the Cold War convinced many business managers that global peace was at hand and that competing in the era of globalization required using just-in-time inventory management.

Equally noteworthy, the decline in price inflation since the early 1980s has made inventories less needed. Indeed, the chart above shows a long, steep decline in inventory ratios starting in the early 1980s when the Federal Reserve under Chair Paul Volker hiked interest rates and Congress passed a series of deregulation bills, both of which slashed price pressures on the economy. Just as important, the chart clearly shows how rising inflation in the 1960s and the energy crises of the 1970s prompted a big jump in inventory holdings equal to about 1% of GDP. The chart also shows that after commodity prices surged around 2005, firms boosted their inventory holdings. That inventory investment was short-circuited by the US housing crisis, but once the recovery started, inventories climbed back to almost 14% of GDP.

This review of history suggests that as company management internalizes the commodity supply shocks and rising prices associated with the war in Iran, there will likely be a rebuilding of inventories. More broadly, as it becomes increasingly clear that the war reflects a wider geopolitical change marked by a US retreat from hegemony, global fracturing, and increased international tensions, we think the rebound in inventories could be bigger and longer lasting than the one in the early 2000s. We also believe this trend will extend beyond the US, with companies around the world incentivized to boost their inventory holdings again.

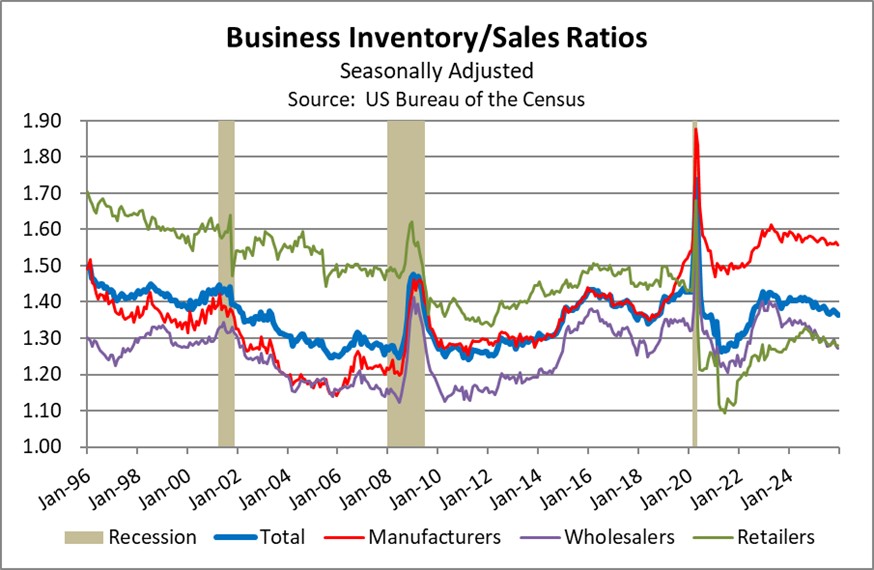

What firms will be most affected? In the chart above, we focus on the US Census Bureau’s current series of monthly business sales and inventory data, in nominal terms, which allows us to trace corporate inventory/sales ratios by sector. The chart clearly shows that the rise in the overall inventory/sales ratio since the early 2000s has come from higher manufacturing stockpiles. This makes sense to us, as supply disruptions and higher costs for inputs and components are probably more important for manufacturers than for wholesalers or retailers. Going forward, we suspect that the Iran war will especially boost inventory holdings at the factory level.

In our view, any broad, sharp rise in manufacturers’ inventories from here on out will have significant investment implications. For example, holding more inventories will tie up more of manufacturers’ capital and increase costs. Investors are therefore likely to put higher valuations on the stocks of manufacturing firms that can better control their inventory levels, all else being equal. Given that the US is now a net energy exporter and has significantly greater levels of secure supplies of oil, gas, and other key commodities, we expect many foreign manufacturers to move production to the US, helping to reindustrialize the US economy and stimulating business for US suppliers. The need to store more inventory could also lead to increased demand and stronger rents for firms that own commercial warehouses. All the same, higher inventories will generally result in a less efficient economy than in the just-in-time world of globalization, so price inflation is still likely to be higher and more volatile than in years past, and the same will likely be true for interest rates.