by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with an update on the war in Iran, including discussions on Iran’s remaining weapons arsenal and potential planning for a US ground operation. We next review several other international and US developments that could affect the financial markets today, including discussions in Congress about cutting federal healthcare spending to help pay for the war and a government move in Japan to ease rules on coal-fired power plants to ease the impact of higher energy prices.

United States-Israel-Iran: As the US and Israel continued to attack Iran over the weekend, the Iranian military continued to respond with missile and drone attacks against Israel and other countries in the region. The Iranian counterattacks raise further concerns about the country’s deep arsenal of weapons and whether significant new capabilities are still being held in reserve. Meanwhile, diplomats from Turkey, Egypt, Saudi Arabia, and Pakistan met to discuss peace proposals over the weekend but with no breakthroughs.

- The New York Times yesterday quoted an unnamed US official as saying Iran likely retains thousands of Shahed attack drones and hundreds of ballistic missiles. Although the official acknowledges that no one knows for sure how many weapons Iran still has, anything in that range would suggest it can still attack and potentially keep the Strait of Hormuz closed for some time.

- In a potentially ominous development in recent days, Houthi rebels in Yemen have fired at least two ballistic missiles at Israel. Both were intercepted, but the development shows how the war could expand further. The Houthis’ military capabilities are widely seen as weakened, but their firepower could still help Iran make up for assets destroyed by US and Israeli bombardment.

- Given the Iranians’ success in hitting critical weapons systems at US military bases in the Middle East, military observers are increasingly convinced that Russia and perhaps China are providing detailed targeting coordinates to the Iranians and may also be providing knowledge or equipment to defeat US air defense systems. Such aid could expand the war, but the US has not lodged a significant public protest against it yet.

- Meanwhile, in an interview with the Financial Times yesterday, President Trump said he’d like to “take the oil in Iran,” suggesting he may send ground troops to seize control of Kharg Island, the center of Iran’s oil export industry. In what may have been an effort to prepare the US public for a prolonged occupation, he also said, “It would also mean we had to be there [in Kharg Island] for a while.”

- Separately, the Wall Street Journal has reported that President Trump is mulling a US operation to seize the 1,000 lbs. or so of partially enriched uranium that Iran is believed to have. Such an operation deep in Iranian territory would require ground troops and be extremely risky, potentially prolonging the war and impacting the president’ political fortunes in the midterm Congressional elections later this year.

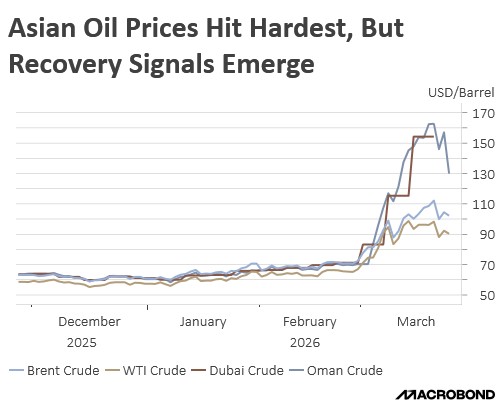

- Iran’s effective closure of the Strait of Hormuz not only continues to drive up energy prices, but it is also creating shortages and boosting prices for other commodities. For example, Middle Eastern helium producers have declared force majeure and warned customers that they won’t be able to honor contracts due to the conflict. Global shortages of helium could lead to production disruptions and raise prices for semiconductors.

- In response to the developments over the weekend, global energy prices are up modestly so far this morning, with Brent crude oil changing hands at $107.37 per barrel, up 1.9%.

US Fiscal Policy: Republicans in Congress are reportedly considering cuts to federal healthcare spending to help pay for a budget bill providing as much as $200 billion to fund the Iran war and immigration enforcement. The healthcare cuts would be couched as reducing fraud and abuse, but some Republicans are concerned that the move would open the party up to election-year attacks that they’re cutting health care to pay for an unpopular war. If offsetting spending cuts or tax hikes aren’t passed, the enormous cost of the war would be added to the federal deficit and debt.

US Politics: A poll taken at last week’s Conservative Political Action Conference found that 53% of attendees support Vice President JD Vance to be the Republican Party’s presidential nominee in 2028, while 35% support Secretary of State Marco Rubio. No other Republican contender had support beyond the single digits. The results suggest Vance currently remains the leader in the race despite Rubio’s growing support.

US Private Credit Industry: New analysis reveals that four large private-credit funds marketed to individual investors by Apollo, Ares, Blackstone, and Blue Owl Capital have more exposure to the software industry than their filings suggest. Amid fears that software firms are threatened by artificial intelligence, the analysis helps explain why investors are now so eager to withdraw their funds from private-credit managers. If AI does materially undercut software firms, the funds’ high exposures would raise the risk of financial contagion, tighter credit, and a recession.

Japan: In a meeting on Friday, the government took steps to let less-efficient coal facilities take part in capacity market auctions in the fiscal year starting in April. Previously, such plants had been restricted from the auctions, where generators sell supply, in order to help tackle climate change. The new move illustrates how countries around the world are now backing away from climate stabilization policies to ensure a more diversified energy mix and better absorb the energy price hikes arising from the Iran war.

Canada: As they try to regroup from their poor third-place showing in last year’s parliamentary elections, the left-wing New Democrat Party over the weekend chose Avi Lewis as its new leader. Lewis, a filmmaker, is a scion of a leftist political dynasty that has been influential at both the national and the provincial level in Ontario. By pushing progressive policies on issues such as the environment and the fate of the Palestinians, Lewis aims to win back voters who abandoned the NDP for the Liberal Party of Prime Minister Carney.

Russia-United Kingdom: The Russian government has declared an official at the UK Embassy in Moscow persona non grata and ordered him expelled from the country for having unofficial meetings with Russian economists. The incident is likely to further strain UK-Russian relations. It will also further reduce the combined US and UK diplomatic presence in Moscow, which has made it difficult for the allied governments to understand and influence Russian foreign policy.