by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment begins with our take on the latest Federal Reserve announcement, followed by an update on the conflict in the Middle East. We then turn to key market developments, including the US softening its assessment of China’s ambitions toward Taiwan, the Bank of Japan’s decision to hold rates steady, and an Apple supplier’s move to diversify its rare earth supply chain. As always, we also include a summary of recent US and international economic data releases.

Fed Stands Pat: The Federal Reserve kept rate cuts on the table after its two‑day meeting, while signaling that officials are still digesting the implications of the ongoing conflict. On Wednesday, the Fed voted 11–1 to leave the policy rate unchanged at a target range of 3.50% to 3.75%, with Governor Stephen Miran dissenting in favor of an immediate cut. While the rate announcement appeared to have a dovish tilt, the forward guidance from the press conference and the Summary of Economic Projections made clear that policymakers have not yet settled on a firm policy path.

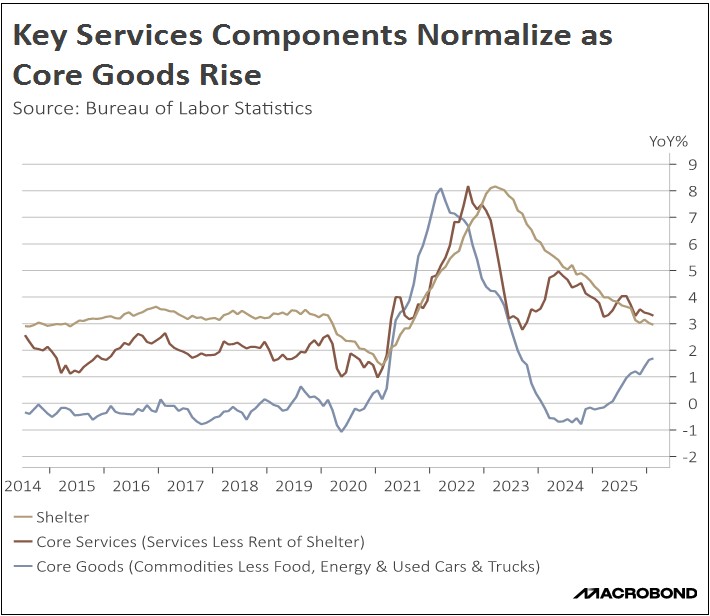

- During the press conference, Fed Chair Jerome Powell emphasized that while the committee expects higher energy prices to put upward pressure on both headline and core inflation, it does not yet have a clear sense of how large or persistent that impact will be. He also noted that tariff‑related goods inflation remains a key driver of current price pressures and said policymakers are watching for signs that those effects begin to fade over the coming months, even as the war adds a new layer of uncertainty to the outlook.

- Powell further cautioned against the over‑interpreting of the Summary of Economic Projections, stressing that the evolving conflict and associated oil shock could significantly alter the outlook in the near term. That uncertainty is reflected in the new SEP, where Fed officials marked up their 2026 forecasts for growth and inflation while leaving their unemployment estimate broadly unchanged and still signaling just one rate cut this year.

- While the inclusion of a rate cut in the Fed’s projections may look dovish at first glance, Powell made clear it is far from guaranteed. He stressed that the committee will not begin easing until it has “greater confidence” that inflation is moving sustainably toward the 2% target. That caveat weighed on market sentiment, reinforcing speculation that, with the Middle East conflict likely to push prices higher in the near term, inflation could drift further from target and make even a single 2026 cut harder to deliver.

- Moreover, given that this is likely to be Chair Powell’s final Summary of Economic Projections, we see it as carrying limited weight for the future policy path. While a sharp policy shift could become necessary if the growth or inflation outlook changes materially, we expect Powell and the Committee to refrain from major adjustments at that meeting, preferring instead to hand over a clean slate to his successor. In our view, this reduces the likelihood of the Fed moving rates, in either direction, before the summer.

A Push for Calm: Attacks on energy facilities around the Red Sea and the Persian Gulf have prompted President Trump to call for calm. On Wednesday, both Israel and Iran struck critical energy infrastructure in the region, with key natural gas and oil installations in Iran, Qatar, and Saudi Arabia reportedly affected. The resulting supply disruptions pushed Brent crude above $115 a barrel, with prices at risk of testing $120 if the conflict continues to escalate.

- The rise in energy prices comes as the war continues to intensify. President Trump has used the latest attacks to urge both sides to stop striking energy infrastructure, while tying that restraint to a new threat of US retaliation. He has pledged that Israel will carry out no further attacks on Iran’s South Pars gas field unless Tehran hits Qatar again, and he warned that in that case the United States would “massively blow up” the field itself.

- The call for calm comes amid growing signs that the war could trigger a broader global energy crunch. European countries have already seen a sharp rise in energy costs, with benchmark gas prices jumping since Iran’s attacks on natural gas facilities in Qatar. At the same time, several Asian governments are exploring ways to conserve fuel to avoid straining supplies, and there is mounting concern that some African nations could face outright shortages if disruptions persist.

- The longer facilities remain damaged or shut in, the more protracted the process of restoring normal production will be. Because many petroleum extraction and storage sites are not designed for extended periods of inactivity, prolonged downtime can complicate maintenance, accelerate equipment degradation, and ultimately make it more difficult and costly to bring capacity fully back online once the conflict subsides.

- The timing of any resolution to the conflict remains highly uncertain, but its economic aftershocks are likely to persist for weeks, and in some cases months. In our view, this raises the risk of an uptick in inflation as supply disruptions and precautionary buying push energy prices higher. Against this backdrop, we expect energy companies to fare relatively well, as tighter supply and elevated prices are likely to support margins for producers.

US Reduces Alarm: The US intelligence community’s latest Annual Threat Assessment marks a notable shift in its outlook on Taiwan, stating that Beijing does not currently plan to execute an invasion by 2027. While Beijing remains committed to reunification, the report suggests that China has no fixed timeline for this objective and maintains a strong preference for a peaceful resolution over military conflict. This more tempered outlook also reflects a softening of tensions between the US and China as both sides explore the possibility of another trade agreement.

Bank of Japan: The Bank of Japan left its benchmark interest rate unchanged at 0.75%, citing heightened uncertainty stemming from the conflict in the Middle East. In his press conference, Governor Kazuo Ueda indicated that policymakers are trying to look through the short‑term effects of the turmoil and keep the option of an April rate hike on the table. The decision, coming shortly after the Federal Reserve also chose to hold rates steady, underlines that major central banks are inclined to be patient and data‑dependent as the conflict unfolds.

US Decoupling: Apple supplier Murata Manufacturing plans to reduce its reliance on Chinese rare earth elements over the next three years. This shift comes as nations increasingly seek to insulate their supply chains from geopolitical volatility, particularly after China utilized its rare earth dominance as leverage in trade negotiations. Diversification is expected to become a defining global trend as industries strive to mitigate vulnerability to future supply shocks.