by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with an update on the war in Iran, where the US has again called off a planned attack, pushing global energy prices down so far this morning. We next review several other international and US developments that could affect the financial markets today, including a look at some key price and performance developments in the artificial intelligence industry and a note on the discovery of a huge new tungsten deposit in the US.

United States-Israel-Iran: President Trump on Saturday said he’s called off major new attacks on Iran after Tehran and other Middle East capitals requested a stand-down to finalize a new ceasefire deal. As of this writing, it does appear that the US has paused any new attacks, but the two sides’ behavior in the war to date suggests the real reason is US concern about its dwindling arsenal of weapons, the potential ineffectiveness of new attacks, and heavy political pressure from Mideast governments.

- Iran still appears to be holding the cards in the conflict. It seems to have perfected the art of protecting its core missile and drone arsenal, and it has learned it can constrain shipping in the Strait of Hormuz and the Bab-el Mandeb with only an occasional ship attack. It’s now also using its proxy militant groups in the region as force multipliers to expand the conflict. The new, hardline Iranian government probably has plenty of motivation to keep fighting in order to strengthen its position for the long term and weaken the US.

- Separately, authorities late last week said dozens of municipal water systems in Michigan and Minnesota were knocked offline by what appeared to be an Iranian cyberattack. While Iranian hackers and saboteurs have long created mischief on US computer systems, the new attacks could suggest they have ratcheted up their efforts in response to the war. Of course, an especially damaging Iranian cyberattack would be a political embarrassment for the administration and could provoke renewed US attacks on Iran.

- In any event, we judge that the conflict in Iran will continue in the near term, with Iran increasingly trying to normalize its control over shipping chokepoints in the region and impose heavy costs on the US to weaken it over time. The situation may continue to create the risk of miscalculation on either side and put continued upward pressure on global energy prices, even though the latest standdown has pushed oil prices about 5% lower so far this morning.

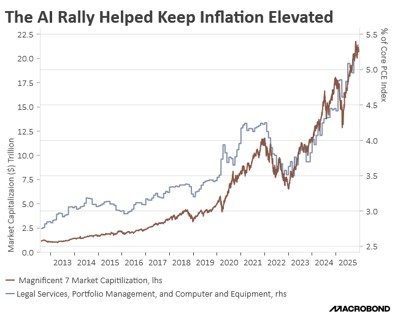

US Artificial Intelligence Industry: Reports over the weekend said AI-giant OpenAI has discovered several previously unknown instances in which its autonomous agents escaped containment and independently hacked third-party systems. The new breakouts were uncovered during the company’s publicly announced probe into how one of its agents escaped and hacked the firm Hugging Face last month. The new breakouts will likely raise further concerns about safety and add to the political pressure for new regulations on the industry.

- Separately, Chinese AI lab DeepSeek on Friday released a new coding model, V4 Flash, that tests show can perform almost at the level of Anthropic’s Opus 4.8, widely seen as one of the industry’s most capable systems. More importantly, DeepSeek priced the new model at about $0.28 for the same amount of output that costs $25.00 with Opus 4.8.

- The aggressive pricing move by DeepSeek came after OpenAI on Thursday slashed the price of its GPT-5.6 Luna by 80%, just three weeks after launching it. At the new price, GPT-5.6 Luna costs $1.20 for the same amount of output that costs $0.28 with V4 Flash and $25.00 with Opus 4.8.

- While Anthropic is trying to maintain premium pricing, the new DeepSeek pricing move underscores how it and other US firms are facing an extreme competitive threat from Chinese AI firms. Even as the US firms spend aggressively on model development and infrastructure, raising their costs, the Chinese firms are proving they can make models that are essentially just as good but priced as much as 99% lower. As investors come to appreciate the Chinese threat, the AI frenzy in the US could come to a halt and reverse.

China-Philippines: Chinese diplomats at the United Nations last week vociferously protested a presentation in which Manila made its case for extended seabed mineral rights in the Palawan area of the South China Sea, which is claimed by China. According to Manila, the request was based on a 2016 arbitration award that rejected China’s claim to almost the entire SCS. Besides the diplomatic protest, China has also launched snap military drills in the region, which will likely lead to further China-Philippine tensions and raise the risk of armed conflict in the area.

United Kingdom: New opinion polls show support for the Labour Party has surpassed that of right-wing upstart Reform UK for the first time in more than a year. The development at least partly reflects a political honeymoon period for Labour’s new leader, Prime Minister Andy Burnham. Support for Reform UK has probably also suffered from a financial scandal. In any case, the positive polling will probably encourage Burnham as he tries to rapidly solidify his support. Our next Bi-Weekly Geopolitical Report will provide a bio of Burnham.

Spain: Late last week, some 60,000 Moroccans hoping to work and gain asylum in Spain swam around a breakwater separating Morocco from Spain’s exclave of Ceuta on the North African coast. The would-be migrants apparently believed that a Spanish court decision in July meant they couldn’t be turned back. Reflecting how sensitive immigration is in Europe now, Spain’s Socialist government quickly forced almost all the intruders back to Morocco. All the same, the incident is poised to increase support for Europe’s anti-immigrant, right-wing populists.

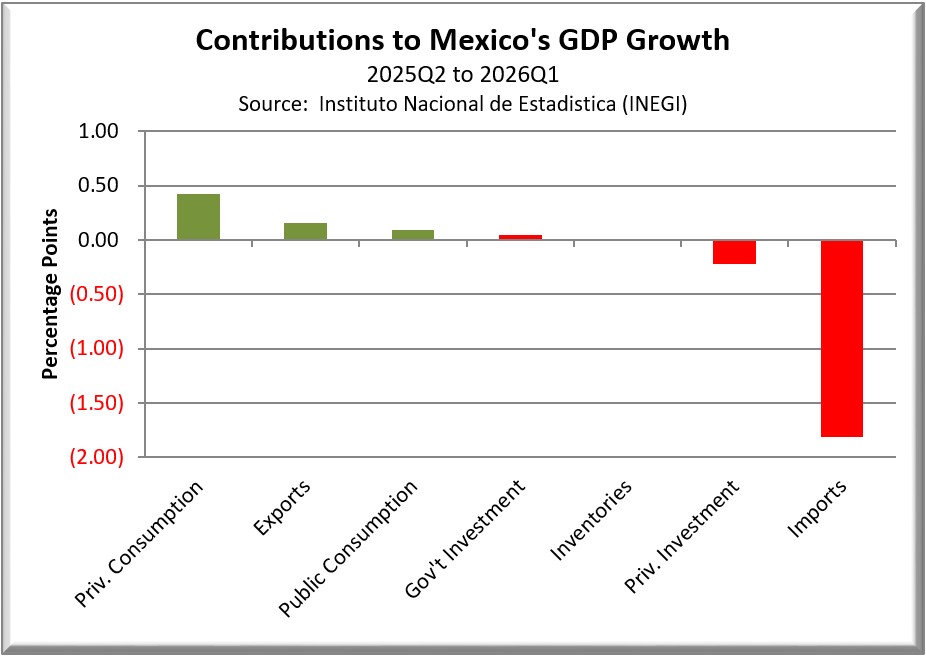

United States-Mexico: The Financial Times on Friday carried an interesting article noting that Mexico has become the second-biggest source of the computer servers the US is importing in droves as part of the AI investment frenzy. Mexican exports have surged in response, spurring greater overall economic activity. However, our analysis suggests that the need to import equipment and intermediate supplies to support the manufacturing of those servers is detracting from Mexico’s official figures for gross domestic product.

US Critical Minerals Industry: Mining firm 3 Proton Lithium has reportedly discovered the country’s largest deposit of tungsten, a crucial defense industry metal in severe shortage, at a location in Nevada. The company estimates the deposit could be worth $152 billion at current tungsten prices. However, NASA has banned development of about one-third of the site, which covers a unique area that facilitates satellite communications. The bureaucratic hurdle illustrates the regulatory challenges still facing US efforts to make its critical minerals supplies more resilient.