by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with an analysis of conflicting economic data before examining the president’s shift toward populist objectives. We also assess the stabilizing diplomatic relations between the US and Latin America, rising momentum for the extension of ACA subsidies, and new restrictions on Chinese imports of Nvidia chips. Lastly, the report includes a roundup of key domestic and international data releases for the coming period.

Mixed Signals: Economic uncertainty remains high as recent data releases provide contradictory signals. The December ISM Services PMI showed the sector expanded more than expected, reaching a 2025 high of 54.4%. Conversely, the JOLTS report revealed that job openings fell to 7.1 million in November — the lowest level in over a year. This divergence complicates the economic outlook, particularly as investors try to gauge what its overall direction will be over the next few months.

- The latest ISM Services PMI offered significant reassurance, showing a robust increase in sector activity to finish 2025. The report highlighted a sharp pickup in both new orders (57.9%) and business activity (56.0%), alongside a welcomed easing of price pressures. This data suggests that the policy uncertainty that weighed on non-tech investment spending throughout 2025 may finally be dissipating as we enter the new year.

- The decline in job openings presents a starkly different narrative. Although the data reflects labor conditions from November, it confirms that labor demand remains subdued. Not only did job openings retreat during the month, but there was also a notable slowdown in US hiring. This suggests that while business optimism may be rising, firms remain cautious about the future and are hesitant to expand their headcounts.

- Over the past year, a noticeable divergence has emerged between resilient economic activity and a softening labor market. This decoupling likely reflects an economy still adjusting to the rapid implementation of trade tariffs and the escalating integration of generative AI. Consequently, we are entering a period that reaffirms the “two-speed” market narrative, where the record-breaking performance of Wall Street stands in sharp contrast to the cooling conditions on Main Street.

- Over the coming months, a convergence in data will likely settle the debate between economic optimists and skeptics. That said, subdued layoff activity bodes well for the bullish outlook, suggesting the economy can withstand current pressures. With market valuations stretched to historic levels, a “risk-off” approach is prudent. We recommend a tactical shift toward higher-quality, less volatile assets.

Populist Pivot: As the country approaches the midterms, President Trump has begun pushing less market-friendly initiatives to placate his populist base. On Wednesday, he announced plans to prevent institutional investors from purchasing single-family homes and signaled a push for defense firms to suspend dividends and stock buybacks. These moves likely serve as the first signs of a rebranding effort as the president seeks to energize his supporters ahead of the upcoming elections.

- These actions have caught the market largely off guard. Although the president (famed for the “put” that bears his name) has a reputation for driving equities higher, his recent maneuvers suggest a pivot toward corporate accountability. This shift indicates a willingness to curb specific business practices and prioritize national objectives over investor returns.

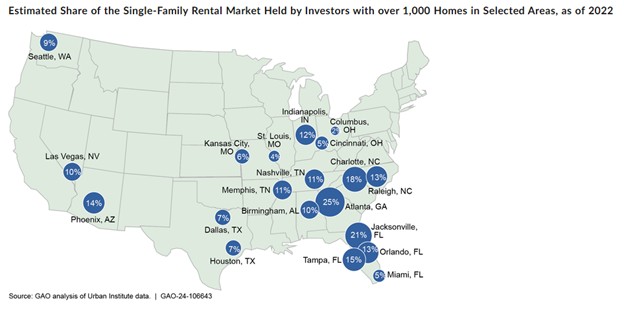

- Advocates for affordable housing have spent years pushing for a ban on corporate home buying, a movement sparked by the fallout of the Great Financial Crisis. Following the 2008 collapse, institutional investors moved in to purchase distressed homes in massive quantities. A 2024 GAO study highlights the scale of this shift. Before 2010, no investor held a portfolio exceeding 1,000 single-family homes. Since 2015, that figure has exploded, particularly in the Sun Belt states as shown in the figure below.

- Furthermore, the president’s push to curb dividends and stock buybacks among defense contractors comes as he proposes a record $1.5 trillion in military spending. These restrictions appear designed to prevent market speculators from profiting from increased government outlays. This is a move that directly addresses a long-standing populist critique regarding corporate war profiteering.

- While there are compelling reasons for optimism in the equity markets — driven largely by expectations of continued monetary and fiscal stimulus — we have observed a notable underpricing of political risk ahead of the 2026 midterm elections. Consequently, we recommend that investors prioritize diversification into value-oriented sectors. This rotation serves as a strategic hedge against a potential shift in market sentiment, especially as both domestic and foreign policy agendas evolve rapidly.

Colombian Crisis Avoided? Tensions between Washington and Bogotá are cooling after a constructive call between the two leaders. Just days ago, markets were rattled by threats of military action against Colombia; however, President Trump’s new conciliatory tone and invitation for a White House meeting have provided much-needed relief. This diplomatic pivot is a tailwind for both US and Latin American equities, as it reduces the immediate risk of geopolitical conflict.

ACA Extension: The House is moving toward a vote to reinstate ACA tax credits for the next three years. Despite a partisan deadlock over abortion funding, nine Republicans voted with Democrats on Wednesday to advance the legislation. The White House has taken an active role in negotiations, with the president pressuring his party to compromise on Hyde Amendment protections to avoid further political fallout from rising healthcare premiums ahead of the midterms.

No Climate Agreement: The White House announced its intention to withdraw from the UN global climate agreement and to reduce funding for climate research agencies. The president justified the decision by stating the agreement no longer served US interests. This move marks a significant shift toward unilateralism, prioritizing national interests over international alliances. Consequently, progress in clean energy research and development is likely to be adversely affected.

China Limits Nvidia Chips: China’s access to advanced semiconductors is becoming increasingly constrained by both its own government and foreign suppliers. In a limited concession, Beijing has authorized the commercial import of certain Nvidia H200 chips, prohibiting their use in state or military applications. However, Nvidia has stipulated that Chinese buyers must pay upfront without the possibility of refunds. This dynamic reinforces a critical trend: Chinese companies are being pushed toward greater technological self-reliance.