Author: Amanda Ahne

The 2026 Outlook: Implications of the New Techno-Industrial State (December 11, 2025)

by Patrick Fearon-Hernandez, CFA, Bill O’Grady, Thomas Wash, and Mark Keller, CFA

Summary of Expectations | PDF

The Economy

Economic Growth

- We expect these trends to be bolstered by stimulative fiscal and monetary policies, ongoing enthusiasm for the promises of AI, and less policy uncertainty.

Recession Risk

- Importantly, we do not expect a recession in 2026, although “tail risks” (e.g., geopolitical events), could trigger an unexpected downturn. However, it should be noted that policymakers have demonstrated they can act aggressively to counteract downturns, which suggests that investors should not over-index to such events.

After its big slowdown in early 2025, we expect the US economy to reaccelerate in the coming quarters, leading to good growth in 2026.

The New Techno-Industrial State

Policy Shifts

- We believe the economy is increasingly being dominated not just by the AI-investment boom, but by a broader policy shift in which government officials more enthusiastically wield influence over the economy, often using industrial policy to advance national security, resilience, or other goals beyond profit maximization.

Navigating a New Era

- With the dawn of this new techno-industrial state, investors need to pay closer attention to the goals and plans of powerful officials in order to understand the evolving investment environment.

Market Outlook

Our asset class expectations call for more moderate performance returns than in 2025, but with balances tipped to the upside, especially for US and foreign stocks.

Fixed Income

- SHORT-TERM

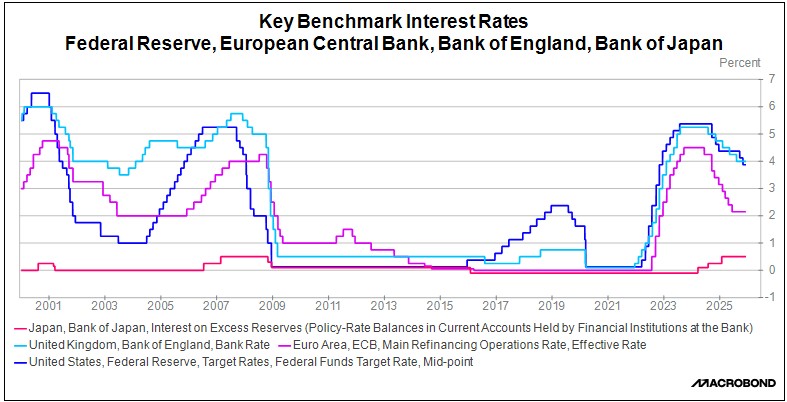

Against the backdrop of a more interventionist techno-industrial state, the Federal Reserve will be under strong pressure to cut its benchmark short-term interest rate more aggressively in 2026 than in 2025. This is especially the case given that the US administration will likely replace several key policymakers at the Fed with more dovish officials. That will likely give a boost to short-term bonds, while weighing on obligations with longer maturities, putting some upward pressure on long-term bond yields. - LONG-TERM

Nevertheless, we expect the government will redouble its efforts to cap long-term yields. Longer-term bonds are therefore expected to produce returns similar to their current yields, while the yield curve should steepen only modestly.

US Equities

- BASE CASE FORECAST

Incorporating our expectations for economic growth, financial conditions, and other factors, our quantitative models suggest that overall corporate profit margins should moderate in 2026 versus their record-high in 2025. We project that S&P 500 operating earnings will equal about 6.3% of gross domestic product, which would put S&P 500 operating earnings at $235.33 per share. - CAPITALIZATION & GROWTH/VALUE

Based on the strong influence of index investing, we expect large cap stocks and growth stocks to continue performing well.

Foreign Equities

- WEAKENING DOLLAR

While our expectation for US stock performance is modest for 2026, we believe that the weakening US dollar and more stimulative fiscal and monetary policies abroad will bode well for foreign stocks. - FOREIGN VS. DOMESTIC

As such, we expect returns on foreign stocks will exceed those of US stocks. Among foreign equities, we continue to favor defense stocks.

Commodities

- We expect global central banks to continue buying gold aggressively, creating continued tailwinds for the yellow metal. However, our modeling suggests gold prices are already stretched, especially if the Fed’s interest rate cuts are backloaded until late 2026. Gold prices may not rise as fast in 2026 as they did in 2025.

- Other major commodities, such as oil, may also struggle against high levels of supply. On the other hand, we think the continuing AI boom will buoy natural gas and uranium prices as those commodities are essential to generating much of the electricity needed for AI data centers.

Daily Comment (December 11, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with an analysis of the Federal Reserve’s latest rate action and the 2026 policy outlook. We then assess rising US-Venezuela tensions and their implications for US foreign policy. This is followed by other market moving events such as China’s strategic dilemma over US chip restrictions, investor skepticism toward Oracle’s AI buildout, and the US-China tax standoff that is delaying the global minimum tax framework. Finally, we include a roundup of essential domestic and international data releases.

Fed Decision: The Federal Reserve delivered a quarter-point reduction to its benchmark rate, setting the new target range at 3.50% to 3.75%. The decision was highly controversial, featuring the most contentious vote of Federal Reserve Chair Powell’s tenure with three dissents — a split not seen in six years. To address persistent strain in the repo market, the Fed concurrently announced the imminent resumption of Treasury Bill purchases. Despite these stimulative actions, the central bank clearly signaled a cautious and potentially restrained trajectory for future monetary easing.

- The Federal Reserve’s latest Summary of Economic Projections (SEP) indicates a more confident economic outlook since September. Officials materially upgraded their median forecast for 2026 GDP growth from 1.8% to 2.3% and modestly improved their inflation projection, lowering it from 2.6% to 2.4% for the year. This brighter picture for output and prices was not extended to the labor market, where the unchanged projection implies policymakers still anticipate tepid hiring in the coming year.

- Despite the official vote, significant internal divisions persist within the Federal Open Market Committee (FOMC). Although the rate decision garnered only three formal dissents, SEP revealed a much deeper disagreement. Five officials favored maintaining interest rates at their previous level, while three others projected that the federal funds rate should be higher than the current target range by the end of 2026.

- In his press conference remarks, Chair Powell framed the committee’s internal divisions as a reflection of differing estimates for the long-run neutral rate — the theoretical policy setting that neither spurs nor slows economic activity. He further elaborated that officials’ growth projections rely significantly on productivity gains, which could result in slower hiring. Speaking on inflation, Powell characterized the recent uptick as likely temporary, attributing it primarily to tariff impacts.

- Heading into 2026, the central debate will be whether the Federal Reserve opts to cut interest rates to below the neutral rate. This decision will largely depend on whether inflation continues to ease and if the labor market cools as expected over the coming year. If these conditions materialize, the Fed may have the necessary impetus to implement deeper rate cuts before the next chair assumes leadership.

US Foreign Policy Turns Hawkish: The United States’ seizure of an oil tanker en route to Cuba has heightened diplomatic tensions with Venezuela. Washington justified the action by declaring the vessel stateless, despite its last known registration being from Venezuela. This intervention directly impedes Caracas’s ability to export oil — its primary source of government funding — and raises the potential for a direct conflict within the region.

- This US action marks the latest in a series of escalations with Venezuela. The pattern began with US airstrikes on Venezuelan vessels suspected of drug trafficking. It escalated further with presidential threats of a land invasion, and most recently, with Caracas accusing Washington of sending fighter jets to intrude on its airspace.

- The recent escalation of rhetoric and actions against Venezuela may be viewed as a bid for regional supremacy. Regardless of whether the US intends to intervene directly, its current behavior — characterized by increased external pressure and military signaling — echoes the pattern of strategic aggression seen in Russia’s approach to Ukraine and China’s persistent actions regarding Taiwan.

- Due to the White House’s unwillingness to create volatility leading into the midterm elections, a direct military attack is not expected. Crucially, though, these actions are designed to normalize the view of the Western Hemisphere as a US sphere of influence. The successful establishment of this precedent will likely lead to a more permanent and greater level of US engagement and assertiveness throughout the region.

Immigration Crackdown: New measures from the Trump Administration aim to restrict migration by tightening enforcement in two key areas. First, the White House has mandated a strict English proficiency requirement for commercial truck drivers, allowing for their immediate removal from service. Second, it has proposed using social media screening to deport visa holders. Collectively, these actions may reduce the supply of labor as it will remove or deter foreign workers from seeking work in the US.

China Chip Dilemma: Chinese firms’ continued demand for high-end US chips is straining Beijing’s push for domestic alternatives, as no local product can match the capabilities of NVIDIA’s H200. Recent disclosures — such as DeepSeek’s use of banned chips and a government review of NVIDIA demand — highlight the gap. Regulators now face mounting pressure as they decide how to allocate export permits after President Trump’s limited sales approval. Chinese firms’ need for US made chips is a reminder of the White House’s leverage in talks.

Oracle Disappoints: The cloud computing company reported disappointing financial results on Thursday, missing sales and profit estimates while raising its capital expenditure plan. This lackluster performance has amplified existing market concerns, specifically, that the aggressive spending on AI infrastructure is outpacing the immediate returns and earnings growth. This growing disconnect between investment and realization will likely lead to greater investor scrutiny and a push for more realistic valuations across the technology sector.

Global Pushback: The White House’s aim to exempt US multinationals from the global minimum tax has met with resistance from OECD nations, led by China. The group was set to finalize this arrangement as part of the second pillar of the global tax regime. While the full plan was expected to be released this year, objections from Beijing, which is advocating for a similar exemption for its firms, have delayed its publication. This holdup has led to speculation that the US could revive the retaliatory tax measures that it contemplated earlier this year.

Daily Comment (December 10, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment begins with an analysis of President Trump’s decision to push for new governance in the EU. Next, we provide a primer for today’s pivotal Fed rate decision. We then offer an overview of critical global developments, including Denmark’s security concerns regarding the US, China’s restrictions on US chip sales, and a breakthrough in French government budget talks. Finally, we include a roundup of essential domestic and international data releases.

Trump on the EU: The US president expressed significant displeasure with current EU governments during a recent Politico interview, signaling a potential rupture in transatlantic relations. He levied specific criticism against the bloc’s leadership, citing its inability to control migration flows and its hesitation to fully back his strategic objectives for Ukraine. The president then intensified the statement by announcing he will openly endorse European candidates who share his outlook, suggesting an increasingly interventionist US foreign policy in the domestic politics of its allies.

- His remarks come as the US is embroiled in several disputes with European leaders, including disagreements over trade, technology regulation, and the approach to ending the Ukraine-Russia conflict. These setbacks have hampered President Trump’s efforts to pivot foreign policy toward containing China’s growing global influence. This tension suggests that the administration may not view its European counterparts as equals, but rather as subordinates to core US interests.

- While an alliance with right-leaning parties in Europe is imperfect, these groups nonetheless are facilitating several policy initiatives that the White House favors. This alignment stems from shared objectives, notably the desire for a swift end to the Ukraine war, a preference for greater national sovereignty within the EU bloc, and a rollback of climate change regulation.

- Despite shared political goals, the informal coalition between right-wing European parties and the US faces some internal friction. This stems from allegations that members within groups such as the Alternative for Germany (AfD) have been compromised, with some members reportedly passing sensitive data to Beijing. Furthermore, some members have pushed for closer energy ties with Russia to secure access to inexpensive resources, a position that directly conflicts with the US strategy of expanding its market share in the European energy sector.

- That said, the president’s statement that he will endorse right-leaning governments appears to be part of a growing trend of political statecraft. The US is actively seeking to reshape its relationships with foreign governments to facilitate deals that may benefit its broader strategic goals. Overall, this increased US involvement could make election outcomes in targeted countries far less certain, as past US interference has yielded mixed results, potentially introducing volatility into the equities of those nations.

- Additionally, the president’s stated aim is likely intended to encourage the EU to become more autonomous, urging the bloc to reduce its reliance on US influence and chart its own path forward. While we suspect the EU will continue to prefer strong ties to the United States, it may seek to balance this influence by entertaining closer relations with China and could even begin competing directly with the US for geopolitical influence in third countries.

Fed Primer: As its two-day meeting concludes, the FOMC is anticipated to lower the benchmark rate by 25 basis points, with future guidance being seen as critical for markets. Deliberations that have occurred since the November meeting have revealed a struggle within the Committee over whether to prioritize the price stability or the maximum employment side of its dual mandate. This tension culminated in unusual, conflicting dissents last time, as one policymaker pushed for a deeper cut while another favored maintaining the current rate.

- This division is likely to dominate the chair’s press conference, as markets remain uncertain about the future policy path. The latest CPI report revealed that core inflation is now rising at the same pace as headline inflation, signaling a potential broadening of price pressures. Meanwhile, the October JOLTS data showed an increase in job openings, even as hiring and quit rates stagnated — a mixed signal for the labor market.

- This policy dilemma unfolds against a backdrop of political pressure from the White House. The president has hinted at nominating Kevin Hassett for Fed chair, while also considering candidates like former Fed Governor Kevin Warsh and current Governor Christopher Waller. Notably, the president has publicly advocated for lower rates, a position echoed by Hassett, who has argued for a cut larger than 25 basis points.

- The market has shown a mixed response to the prospect of Fed rate cuts. While the anticipation of lower rates has boosted equities, concern over the possible loss of Federal Reserve independence — fueled by the potential appointment of a politically-aligned figure like Kevin Hassett as Fed chair — has provided support to 10-year Treasury yields, a development arguably more significant than the equity rally.

- The market will likely be paying close attention to the forward guidance provided by the Fed as it reviews the Summary of Economic Projections and the subsequent press conference. The prevailing expectation is that the Fed will cut rates by 25 basis points but signal an indefinite pause while it awaits further economic data. While we agree that a rate cut is more probable than not at this meeting, we suspect the Fed will continue to be less concrete on the path forward but will likely still leave the door open for additional cuts.

Denmark Fears the US: For the first time, the Danish Intelligence Agency (FE) has described the US as a potential security risk in its annual threat assessment. This unusual designation follows the US’s public pursuit of acquiring Greenland, a Danish territory. The agency’s report explicitly noted that the US is increasingly prioritizing its own self-interest, often at the expense of its allies. While this development is unlikely to have immediate market ramifications, it is a clear indicator of growing strategic mistrust between the US and its long-standing partners.

Pentagon Picks Google: Defense Secretary Pete Hegseth announced that the department has selected Gemini for its government systems to address its artificial intelligence (AI) needs. This selection is another example of the growing coordination between the US government and the technology sector, and it underscores the increasing reliance of tech companies on government contracts for sales. This major purchase is likely to boost Google’s stature as a significant and capable challenger to OpenAI in the competitive AI space.

China Blocks Nvidia: Beijing is reportedly preparing new limits on companies seeking to purchase the H200 chips recently cleared by the White House for export. The move is intended to push Chinese firms toward domestically produced alternatives, consistent with China’s broader goal of strengthening technological self-sufficiency. It also carries a political dimension as Beijing aims to avoid the appearance of yielding to US pressure — particularly amid reports that roughly 20% of the chip revenue is expected to go to the US government.

French Budget Passed: The French parliament passed the 2026 social security budget on Tuesday, a critical step toward approving the full state budget by year’s end. While the move was welcomed, concerns remain that Prime Minister Sébastien Lecornu may lack the votes needed for the broader bill, having alienated key allies with concessions to the Socialist Party. Nevertheless, finalizing the budget should help ease pressure on French bond yields.

Daily Comment (December 9, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with changes to Washington’s policy limiting Chinese access to advanced US computer chips and what the changes say about power dynamics in the US and between the US and China. We next review several other international and US developments that could affect the financial markets today, including a shift in investor expectations regarding foreign interest rates and an update in US artificial intelligence policy.

United States-China: President Trump yesterday said his administration will lift its ban on Nvidia selling its nearly cutting-edge H200 artificial-intelligence computer chips to China. In return, the US will get a 25% cut on all Chinese revenue from the H200s. The deal marks the federal government’s latest extraordinary intervention into private markets and suggests the administration is continuing to favor the “tech bros” element of its political coalition over its “China hawks” element.

- Nevertheless, reports this morning say Beijing plans to limit access to the H200 chips as it focuses on achieving self-sufficiency in semiconductor production. Sources say Chinese firms will likely have to apply to the government to buy the chips and show why they can’t rely on domestic semiconductors.

- Taken together, these developments illustrate a changing, complex balance of power within and between the US and China. Domestically, the US government is sharply expanding its power over the private sector and has become much more willing to flex its muscles. Internationally, however, the US this year has often discovered that it has less leverage against China than it thought, and that China is less dependent on US goods and technology than previously expected.

European Union Immigration Policy: The EU’s national internal affairs ministers yesterday signed off on a dramatic tightening of the bloc’s immigration policy, making it easier to deny asylum claims and allowing failed asylum seekers to be detained and deported to “return hubs” outside the EU. The modifications still must be negotiated with, and approved by, the European Parliament. However, whatever their final form, they are likely to herald much tighter immigration into the EU, despite the region’s low birth rates and weak population growth.

European Union Environmental Policy: EU officials early today agreed to sharply curtail the bloc’s controversial supply-chain regulations, which aimed to address environmental and social concerns throughout supply chains touching the EU. The changes will sharply limit the rules to a relatively small number of huge enterprises that will be more able to absorb their costs. As we note in our upcoming Geopolitical Outlook for 2026, the shift reflects a nascent, politically driven trend toward deregulation in the EU that could help boost the region’s economic growth.

Eurozone Monetary Policy: For the first time, swap market trading suggests investors now think the European Central Bank is more likely to hike its benchmark interest rate in 2026 than to cut it. Investors also expect the Canadian and Australian central banks to start hiking their rates next year, while the Bank of England is expected to stop cutting its rate by mid-2026. The change in sentiment reflects less pessimism about economic growth and more concern about price inflation and debt. The Bank of Japan began slowly hiking its interest rates in early 2024.

- Even if the key foreign central banks do start hiking their interest rates, we continue to believe the Fed will cut its benchmark fed funds rate more aggressively in 2026 than in 2025 as it faces a softening US labor market and outside political pressure.

- Any rise in foreign interest rates while US rates are falling would likely put additional downward pressure on the dollar. As we have noted many times in the past, periods when the greenback is depreciating have typically led to better returns for foreign stocks than for US stocks.

US Monetary Policy: The Fed today begins its latest policy meeting, with its decision due tomorrow at 2:00 PM ET. This meeting will also include the policy committee’s updated economic and financial projects (the “dot plots”). Based on futures prices, investors are virtually unanimous in expecting the policymakers to cut their benchmark fed funds short-term interest rate by 25 basis points to a range of 3.50% to 3.75%.

US Artificial Intelligence Policy: President Trump yesterday said he will sign an executive order this week to prevent US states from imposing their own regulations on the AI industry. Instead, the order will give the federal government the sole right to impose a uniform set of regulations, with the goal of fostering a rapid build-out of the industry.

- The order will be further evidence that the administration is favoring the tech industry over other interests, including states’ rights.

- The administration’s preference for the tech industry is probably one reason why tech stocks have performed so well this year.

US Energy Policy: A district court judge in Massachusetts yesterday nixed President Trump’s January order freezing federal approvals of new wind energy projects, arguing that the order was “arbitrary and capricious.” Despite the setback, however, the order is likely to be appealed, and the ban could well be reinstated. In other words, the court decision doesn’t definitively clear the road for further green energy projects in the US.

US Agriculture Industry: President Trump yesterday announced a $12-billion federal bailout of US farmers, who have been struggling with low prices due to record production and weaker purchases by China. According to the American Farm Bureau Federation, more than half of US farmers are currently losing money. The new aid will likely help buoy demand for a range of agricultural inputs and help support the stock prices of firms ranging from agricultural equipment manufacturers to seed and fertilizer producers.

US Stock Market Strategy: According to the Wall Street Journal yesterday, banking giant JPMorgan Chase has not only launched its $1.5-trillion fund to invest in US defense firms and other enterprises building US innovation and resiliency, but it has also formed a panel of outside advisors for the fund ranging from Amazon CEO Jeff Bezos to former US Secretary of State Condoleezza Rice.

- We at Confluence have long argued that the growing US-China rivalry and global fracturing will create investment opportunities in defense firms and companies related to economic resiliency.

- JPMorgan’s establishment of a large fund dedicated to the theme, along with an advisory board stocked with high-level executives and national security experts, is evidence that the opportunities are finally being recognized even by big, traditional financial firms.

Global Energy Market: According to the chief economist at commodities trading giant Trafigura, the global oil market could face a “super glut” in 2026 as huge new supplies arrive and global demand weakens. For example, the economist cited the completion of big, new production projects in Brazil and Guyana but slowing demand growth in China as it relies more heavily on electric vehicles.

- The top oil trader at Trafigura recently said that he expects Brent crude prices to fall below $60 per barrel in the near term, versus about $62.50 today and more than $80 in early 2025.

- If the current oil glut does worsen as Trafigura expects, it would naturally help hold down consumer price inflation, but it would also weigh on global energy equities.

Daily Comment (December 8, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with new developments regarding the global and US equity markets, as well as gold. We next review several other international and US developments that could affect the financial markets today, including a dangerous military standoff between Japan and China northeast of Taiwan and a preview of the Federal Reserve’s latest policy meeting coming up this week.

Global Public and Private Equity Markets: Reflecting the push to allow everyday investors to take positions in private equity markets, MSCI has launched a new index to track the returns on a combined portfolio of global stocks and private equity funds. The new MSCI All-Country Public + Private Equity Index blends stocks and unlisted assets into a single benchmark, with unlisted assets set at 15% of the portfolio. The new index could further fuel investors’ interest in private equity and debt investments and new funds to meet that interest.

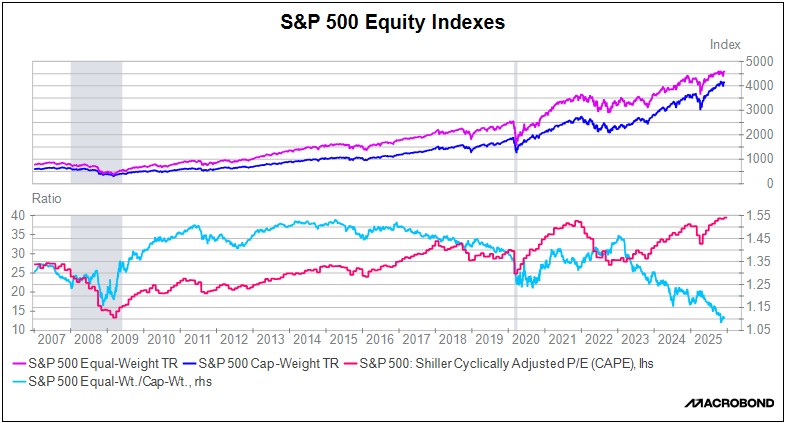

US Stock and Precious Metals Markets: The Bank for International Settlements, often called the “central banks’ central bank,” today issued a report warning that both US stocks and gold are showing signs of being in a bubble. The report notes that the current period is the only instance in the last 50 years when both US stocks and gold have appreciated rapidly at the same time. Of note, the BIS said its research shows the rapid price gains are being driven by “exuberance” among retail investors.

- Clearly, US stock and gold prices are very high and are trading at extraordinarily high valuations. Whether or not they are in a bubble, there is probably a growing risk of a sharp re-pricing at some point in the coming year or two. In addition, US stock prices would be at risk of a correction if corporate profits begin to falter in the face of issues such as tariff disputes, supply chain disruptions, excess investment, or consumer caution.

- We discuss all these issues in our Economic and Financial Market Outlook for 2026, which we expect to publish this week.

China-Japan: Amid the growing tensions over Prime Minister Takaichi’s recent comments that a Chinese blockade of Taiwan would prompt Japan to intervene militarily, Tokyo said Chinese jet fighters on Saturday twice locked their fire-control radars on Japanese fighters northeast of Taiwan. The radar locks could have potentially been a prelude to firing missiles at the Japanese jets. Beijing responded on Sunday by saying the Japanese planes had come too close to a Chinese aircraft carrier.

- Beijing’s responses to Takaichi’s statements so far have focused on sharp rhetoric and various trade and travel restrictions, but it has avoided deploying its most powerful economic sanctions and has kept a lid on military responses.

- Nevertheless, the incident on Saturday is a reminder that the current tensions carry a risk of boiling over. Investors have seemed complacent over the China-Japan tensions, but they should remember that it would only take a small miscalculation or accident to spark a more serious crisis or even conflict between the two nations, which would almost certainly disrupt the global economy and financial markets.

- As the US continues to shift its foreign policy away from the global hegemony it practiced for decades, and as the rise of revisionist states such as China and Russia continues to spur global fracturing, we have long asserted that geopolitical tensions will worsen over time. This new, tension-filled backdrop to the global investment environment is a key reason we favor assets such as Asian and European defense stocks and gold.

Japan-Australia: Underscoring the geopolitical tensions mentioned above, the Japanese and Australian defense ministers announced a new “framework for strategic defense coordination” between their respective countries on Sunday. Although short of a full mutual defense treaty, the new program aims to boost national security coordination between Japan and Australia as the two countries face the challenge of China’s rising geopolitical aggressiveness and a cooler commitment from the US.

China-Southeast Asia: Research by the Financial Times shows that Chinese exports to the Southeast Asian countries of Indonesia, Singapore, Malaysia, Thailand, Vietnam, and the Philippines in the first nine months of 2025 were up 23.5% from the same period one year earlier, about double the growth rate in the previous four years. The figures suggest the new US import tariffs against China are indeed prompting Chinese firms to dump or reroute their goods to nearby countries, which could weigh on those nations’ economies and firms.

Thailand-Cambodia: The Thai military today launched airstrikes against positions in Cambodia, claiming Cambodian troops had fired across the disputed border in violation of a truce brokered by the US in July. Thailand has evolved in recent decades as an important manufacturing hub in the region, and China is now routing many final goods and manufacturing components to it (see discussion immediately above). The fighting therefore has the potential to disrupt local and international supply chains, possibly affecting Thailand’s economy and stock market.

US Monetary Policy: The Fed holds its latest policy meeting this week starting on Tuesday, with its decision due on Wednesday at 2:00 PM ET. This meeting will also include the policy committee’s updated economic and financial projects (the “dot plots”). Based on futures prices, investors are virtually unanimous in expecting the policymakers to cut their benchmark fed funds short-term interest rate by 25 basis points to a range of 3.50% to 3.75%.

US National Security Policy: In a speech to the Ronald Reagan Defense Forum in California on Saturday, Secretary of Defense Hegseth said the US government is now prioritizing defense of the homeland and the Americas region. The statement is consistent with the administration’s new National Security Strategy released last week, which de-emphasized the military threats from Great Powers such as China and Russia or rogue nuclear states such as Iran and North Korea.

- The new, regionally focused security strategy likely implies major changes in the size of the US armed forces, what weapons the armed forces buy, and how they operate.

- For example, prioritizing the interdiction of drug-running boats or immigrants close to US shores while maintaining a smaller deterrent force for non-regional threats could potentially require fewer troops, less expensive operating tempos, and fewer major weapons systems. That is one reason why we think foreign defense stocks may offer better returns than US defense firms in the coming years.

US Food Industry: Amid rising political pressure over the cost of living, President Trump yesterday signed an order creating task forces to probe price-fixing and other anticompetitive behaviors in the food supply chain. The order calls for a particular focus on the market behavior of foreign-controlled companies. We suspect such an effort will have little direct effect on food prices. However, it could present regulatory risks for consumer staples firms, especially if they are headquartered abroad.

Asset Allocation Bi-Weekly – What Catch-Up Economic Reports Say About the AI Boom (December 8, 2025)

by Patrick Fearon-Hernandez, CFA | PDF

Now that the federal government’s record-breaking shutdown over budget issues has ended, agencies have been releasing batches of delayed economic reports. In some cases, officials have warned the reports may never be released, given that statisticians can’t go back in time and collect certain data. The prime examples of that are the consumer price index and the monthly unemployment rate, which is based on a nearly real-time survey of households. Nevertheless, other reports are coming out now, and even though we have written up some of them with a quick, concise analysis in our Daily Comment, we think it would be useful to provide a more in-depth analysis of some of these catch-up reports, along with their implications for investors. We will focus on the recently released data for August construction spending and September durable goods orders, which together show a nuanced impact from today’s big boom in artificial intelligence (AI) investment.

August construction spending rose modestly by a seasonally adjusted 0.2%, following a similar gain of 0.2% in July and a 0.5% rise in June. Private residential construction spending jumped 0.8%, accelerating from its July gain of 0.7% and marking its third straight monthly increase. In contrast, August public works spending was flat. Even more interesting, August spending on private nonresidential construction fell 0.3%, after a decline of 0.5% in July. In fact, this proxy for commercial construction has only posted two monthly gains (of 0.1% each) over the last year. Total construction spending in August was down 1.6% from the same month one year earlier, with public works spending up 1.8% but private residential outlays down 1.5% and private nonresidential outlays down a whopping 4.3% (see chart on next page).

Given all the news stories about artificial intelligence firms spending massively on data centers, cooling equipment, and other AI infrastructure, some investors might be surprised at the recent relative weakness in commercial construction outlays. What explains this weakness? In large part, the problem appears to be that the big AI boom hasn’t been enough to offset this year’s anemic corporate investment outside the AI sector. One reason for that has probably been the uncertainty over US trade policy this year, which has discouraged some new investment despite the lucrative tax incentives in this year’s “Big, Beautiful” tax and spending bill. We think that another likely reason has probably been the weak consumer spending by lower-income households.

Separately, September durable goods orders rose by a seasonally adjusted 0.5%, marking their second straight monthly gain but slowing from their increase of 3.0% in August. Of course, durable goods orders are often driven by transportation equipment, where just a few airliner orders can have a big impact. September durable goods orders excluding transportation rose 0.6%, marking their fifth straight monthly increase and accelerating from their rise of 0.5% in the previous month. Finally, the durable goods report also includes a proxy for corporate capital investment. In September, non-defense capital goods orders ex-aircraft rose by 0.9%, after similar gains of 0.9% in August and 0.7% in July. Overall durable goods orders in September were up 9.6% year-over-year, while durable orders ex-transport were up a more modest 4.6% and non-defense capital goods orders ex-aircraft were up 5.3%.

The chart below shows the year-over-year change in non-defense capital goods orders ex-aircraft since just before the Great Financial Crisis (GFC). The chart does show how this proxy for corporate capital investment has strengthened over the last couple of years. All the same, the annual growth in this spending is decidedly modest compared with the booms that occurred after the coronavirus pandemic, in the late 2010s, and in the years right after the GFC. Coupled with the relative weakness in commercial building discussed above, this data points to overall weakness in commercial equipment spending and is further evidence that most firms have become quite cautious about new investment, at least for the moment. Headwinds from policy uncertainty and weakness in some consumer sectors have weighed not only on building activity but also on equipment investment.

What does all this imply for investors looking forward to 2026? In our view, this year’s policy uncertainty is likely to dissipate in 2026 as the US strikes more trade deals and key court decisions are reached. Moreover, the Federal Reserve looks set to keep cutting interest rates. If these developments encourage a catch-up in corporate investment spending beyond the AI sector, it should support some re-acceleration in economic growth. Of course, lower-income households are still likely to be husbanding their resources, and that could limit overall growth in 2026. All the same, we see reason for optimism regarding overall economic growth, which could support US stock prices.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Asset Allocation Bi-Weekly – #153 “What Catch-Up Economic Reports Say About the AI Boom” (Posted 12/8/25)

Daily Comment (December 5, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with an assessment of the US effort to guarantee smooth economic relations with China. Next, we turn to the fine that the EU levied against X for violating its controversial new tech rules. We then provide an overview of critical global developments, including Japan’s bond market concerns, US lawmakers’ attempt to curtail advanced chip exports to Russia and China, and the latest indicators of a regional arms build-up in the Indo-Pacific. Finally, we close with a roundup of the essential domestic and international data releases.

Tensions Cool: The US and China trade tensions appear to have cooled after extending the deadline for trade talks last month. US Trade Representative Jamieson Greer stated that the US is prioritizing a stable trade dynamic with China as it seeks to prevent a new conflict. His comments are likely to reinforce the view that the White House is looking to calm fears of ongoing trade disruption as they seek to reduce uncertainty that could potentially hinder growth in a midterm election year.

- Greer’s comment comes as the US and China work to fully implement an understanding reached during trade talks in early November. While a written agreement has not been formalized, the US announced plans to lower certain trade tariffs. In a reciprocal move, China committed to suspending export restrictions on rare earth elements vital for technology manufacturing, and the White House confirmed that China also promised to increase its purchases of US soybeans and other farm products.

- Following the talks, Chinese officials called on the US to honor commitments to curb rhetoric related to Taiwan’s independence. This has complicated the regional security landscape and has forced the US to navigate heightened tensions stemming from Japan’s claim that a Chinese takeover of Taiwan poses a national security risk. Also, similar concerns were voiced by Taiwanese leader Lai Ching-te regarding President Xi Jinping’s rumored desire for the Chinese military to be ready for an invasion by 2027.

- Stable relations with China are likely crucial for the White House’s goal of retaining control of both houses of Congress in the upcoming election year. To avoid voter backlash, the administration must ensure no disruptions in trade — such as the loss of rare earth elements that has historically caused a pull-back in equities — while also securing China’s continued purchases of US agricultural products.

- That said, we view the US stance of prioritizing stability and avoiding tensions with China as particularly favorable for domestic equity markets heading into next year. The suspected resumption of trade consistency and the avoidance of new tariffs are expected to bolster corporate confidence, encouraging companies to pursue expansion, especially given the considerable tax incentives provided by recent legislation.

EU Fines: The European Union imposed a penalty on Elon Musk’s X for failing to comply with its Digital Services Act (DSA). Despite the fine being less than anticipated, estimated at 120 million EUR ($140 million), it provoked swift criticism from the White House. The US administration asserted that the EU’s action unfairly targets American tech firms and encroaches upon principles of free expression. The divergent approaches to tech regulation continue to pose a significant challenge to transatlantic relations even as both sides work toward resolving trade disputes.

Japan Bond Problems: Prime Minister Sanae Takaichi is closely monitoring the bond market as she attempts to chart a course for restoring growth in Japan. Her concern has intensified due to rising bond yields and a weakening yen, both driven by skepticism that her proposed $137 billion stimulus package will adequately boost growth without triggering inflation. This concern has prompted a renewed effort to cut government waste and support tight monetary policy. Should these initiatives prove successful, they could put downward pressure on the US dollar.

Canada Pushes Back: The Canadian government has served a default notice to Stellantis after the automaker announced its intention to move its manufacturing plant from Ontario to Illinois. This relocation may constitute a breach of the loan agreement under which Stellantis received forgivable financing to maintain operations in the region. Canada’s enforcement action may, in turn, provoke a US reaction as Washington seeks to remove barriers to its national reindustrialization agenda.

Block AI Chips: A day after Nvidia successfully lobbied to defeat a provision that would have required it to prioritize American firms for its chip sales, the Senate introduced a separate, bipartisan piece of legislation. This new bill proposes to halt export licenses for selling advanced chips to US adversaries China and Russia for a minimum of 30 months. This legislative action is a reminder that even as trade tensions between the US and China have cooled, there remains little tolerance for American chip companies aiding Beijing’s AI ambitions.

Macron and Xi Talk: French President Emmanuel Macron and Chinese President Xi Jinping met on Thursday to discuss ongoing relations between Europe and China, a talk held ahead of France taking over the G7 presidency in 2026. France reiterated its position that China needs to boost its investment in Europe. Meanwhile, Beijing stressed that France should not align with US efforts to contain China. Xi maintained that Europe could be included in its anticipated five-year plans, but the talks ultimately ended without a formal agreement.

Indo-Pacific Arms Race: Following White House approval, South Korea has decided to proceed with the development of its own nuclear-powered submarine. This military initiative is expected to strengthen South Korea’s ability to counter threats from North Korea. However, the move is also likely to heighten tensions with China and place pressure on Japan to develop similar capabilities. This pursuit of advanced military technology by South Korea underscores the growing importance of defense companies as the world continues to fragment into blocs.