by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment begins with an analysis of the escalating feud between the White House and the Federal Reserve. Next, we examine key global developments, including an unexpectedly strong consumer confidence reading for August, new US commitments for supporting Ukraine in its post-war security, and the imposition of fresh tariffs on Indian goods. We conclude with an overview of other critical domestic and international factors shaping the current financial landscape.

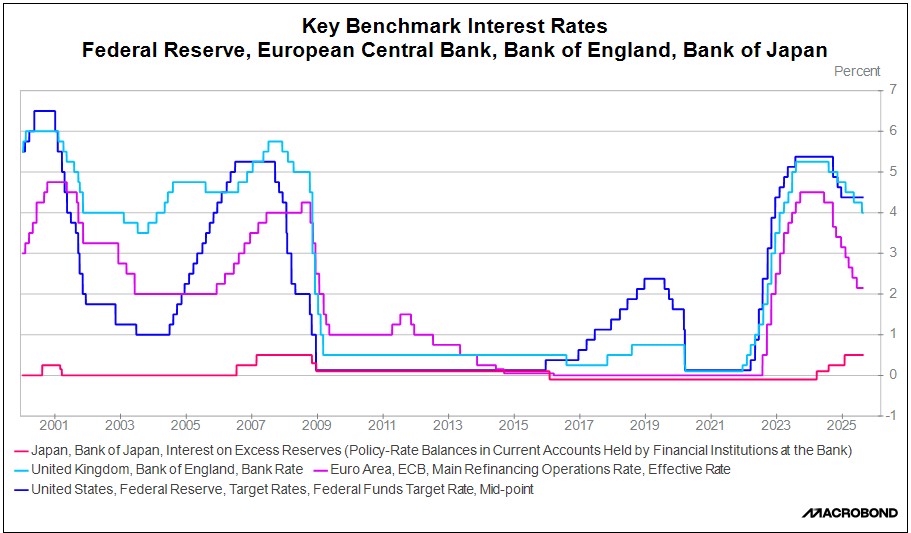

Reshaping the Fed: Uncertainty over monetary policy is causing the yield curve to steepen. Increased expectations of rate cuts have pushed down the short-term yields, while growing concerns about a potential shift away from inflation control has lifted long-term yields. This sentiment follows President Trump’s announcement that he will seek a replacement for Fed Governor Lisa Cook due to allegations of mortgage fraud. Although her departure is considered unsettled, the move signals that the administration intends to reshape the Federal Reserve.

- The administration is reportedly considering former World Bank Group President David Malpass as a potential nominee to replace Cook on the Federal Reserve Board. This effort coincides with the upcoming Senate confirmation hearing for Stephen Miran to fill a separate vacancy left by Adriana Kugler’s resignation. If he fills both positions, then the president would have appointed a majority of the sitting Federal Reserve Board governors, potentially giving him more control of its objectives.

- Lisa Cook’s lawyer has stated that she will file a lawsuit to challenge her removal by the president, arguing that the action is unlawful. This legal battle could allow her to remain in her seat and participate in upcoming Federal Open Market Committee (FOMC) meetings, including the one scheduled for September 16-17. The Federal Reserve has issued a statement on the matter stating that it will comply with any judicial ruling on the matter.

- By appointing loyalists to the Federal Reserve Board of Governors, the White House appears to be pressuring Chair Jerome Powell. This strategy has a historical basis as a chair’s role becomes untenable without the board’s support. The last significant resignation of this kind was in 1979 when G. William Miller stepped down after reportedly failing to mesh with his fellow governors.[1]

- Increased executive branch control over the Federal Reserve would likely have a ripple effect on both the dollar and the bond market. Doubt about the central bank’s ability to independently combat inflation could prompt foreign investors to reduce their exposure to US assets. Such a move would be a strategic effort to mitigate risk in a potentially inflationary environment.

Consumer Confidence: The Conference Board’s August consumer confidence index surpassed expectations, despite a month-over-month decline. This more optimistic reading was influenced by an upward revision of the previous month’s report, indicating that consumers were more confident in July than initially thought. However, there is growing pessimism about the labor market among households. While this could signal consumers becoming more cautious, there is no evidence of widespread layoffs.

Chip Wars: Chinese chipmakers are set to triple their production of AI processors by next year, a strategic move by Beijing to lessen its dependence on advanced US chips. This aggressive expansion follows the US government’s decision to tighten restrictions on chip sales to China, which has significantly impacted companies like NVIDIA. The escalating competition for AI supremacy is expected to be a major factor shaping market trends in both the US and China.

Energy Strain: The rise in utility prices, driven in part by energy-intensive data centers, is impacting a growing number of households. As electricity costs escalate, an increasing number of regions are voicing concerns. In response to these pressures, some companies are exploring alternative energy strategies. For example, Meta is reportedly investing in a new $50 billion data center and developing its own energy plan to help mitigate these rising costs. We think this could present opportunities for energy companies in the future.

Ukraine Postwar Backing? The US has announced its readiness to contribute to a European-led defense shield in a post-war Ukraine. This commitment would include providing intelligence assets and offering battlefield oversight. This agreement is part of what appears to be an intensified US effort to broker a deal that could end the conflict between Ukraine and Russia. The shift in US policy follows recent statements from Vice President J.D. Vance, who indicated that Russia’s President Putin has also made some concessions.

India Tariffs: On Wednesday, the US imposed secondary tariffs on goods from India, a move that has put pressure on the Indian economy. The tariffs, set at 50%, are designed to penalize India for its continued purchase of Russian oil. In response, Indian firms are seeking government support to manage the financial burden of these new levies. India’s prime minister has encouraged citizens to “buy domestically” to mitigate the economic impact, but it remains uncertain whether this strategy will be sufficient without additional government aid.

EU Removing Tariffs? EU officials are reportedly preparing to pass legislation that would eliminate tariffs on all US industrial goods. This move is intended to persuade the US to lower its current 27.5% tariff on European automobile exports to a more favorable rate of 15%. The automotive industry, which is a key export for the European Union (particularly for Germany), has been under significant pressure from the elevated US tariffs. If the legislation is approved, the new 15% tariff on autos could be applied retroactively.

Spy Allegations: Danish authorities have contacted US diplomats to address concerns that American individuals associated with the Trump administration are conducting influence operations in Greenland. The alleged objective of these campaigns is to rupture the relationship between Greenland and Denmark. This move aligns with the president’s publicly stated interest in bringing the strategically crucial Arctic Island under US influence. The allegations risk triggering significant diplomatic friction between the US and the EU.

[1] Greider, William. (1987). Secrets of the Temple: How the Federal Reserve Runs the Country. New York, NY: Simon & Schuster, p. 66.