Author: Amanda Ahne

Daily Comment (August 29, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with an analysis of the recent upward revisions to US GDP data. We then explore several pivotal global developments, including Japan’s potential shift away from long-duration bond issuance, Canada’s concession on US tariffs, and the sell-off in British bank shares. Finally, we conclude with an overview of other essential domestic and international factors shaping the financial landscape.

GDP Surprise: The US economy grew even faster than initially thought in the second quarter, with GDP revised up to a robust 3.3% annualized rate. This upgrade was fueled by strong consumer spending, solid net exports, and increased business investment, which more than offset a slight dip in government outlays. Crucially, underlying domestic demand — measured by Final Sales to Private Domestic Purchasers — remained sturdy, growing at a steady pace and signaling that the economy retained its momentum from the start of the year.

- The stronger-than-expected GDP data bolsters the argument that the economy is not in recession. The solid expansion in the second quarter effectively offsets the prior quarter’s contraction, signaling resilience rather than a downward trend. A key driver of this performance was household spending on durable goods, with orders for motor vehicles providing a significant lift to overall sales figures.

- Although the data is positive, it warrants cautious optimism. The labor market’s stagnation, characterized by a hiring freeze amid a lack of layoffs, indicates that firms view the economic softness as transitory. For investors, we believe this environment presents an opportunity to increase risk exposure. We advise focusing on companies with strong profitability and domestic supply chain reliability, which are critical differentiators in the current climate.

Japan Reducing Long Bond Supply: The Ministry of Finance in Japan has reportedly surveyed primary dealers regarding a potential reduction in the issuance of long-term government bonds. This action is a strategic move to address the upward pressure on domestic interest rates. It comes as the Bank of Japan (BOJ) begins to unwind its extensive quantitative easing program, and the government continues with its own fiscal expansion.

- By reducing the supply of these longer-dated bonds, the Ministry aims to stabilize the bond market and help prevent a sharp increase in government borrowing costs, which have been rising due to weak demand and the BOJ’s reduced market presence.

- This trend is indicative of a deteriorating appetite for debt among bond investors. While we have not yet witnessed a failed auction, the clear pushback from the market is a cause for vigilance. In response, major sovereign debt issuers like Japan, the US, and the UK have indicated a strategic pivot towards shortening the maturity of their debt issuance to accommodate investor demand.

Jumbo Cut in September? Fed Governor Christopher Waller stated he is prepared to cut interest rates aggressively if upcoming jobs data shows further labor market softening. His comments come amid growing market expectations for a September rate cut, fueled by recent downward revisions to payrolls that have raised doubts about the labor market’s strength. This highlights the ongoing tension within the Fed over whether to prioritize its price stability or maximum employment mandates.

Brazil Response: In response to recent US tariffs that imposed duties as high as 50% on Brazilian exports, the administration of President Lula da Silva is preparing retaliatory measures. The Brazilian Chamber of Foreign Trade has been tasked with assessing the tariffs’ economic impact and developing a list of potential countermeasures. The government is scheduled to officially announce this retaliatory investigation later today. The rise in trade tensions between the two countries will likely impact Brazilian equities more than their US counterparts.

Canadian Tariffs: The Canadian government now concedes that it will not secure the complete removal of US tariffs on its exports. This pessimistic outlook follows Canada’s commitment to unilaterally lift its retaliatory tariffs on American goods by September 1, among other concessions made to ease trade tensions. Although the majority of bilateral trade flows freely, persistent US tariffs on Canadian steel continue to inflict economic damage.

Taiwan-US: Two US senators have reignited the debate over America’s commitment to Taiwan. Mississippi Senator Roger Wicker and Nebraska Senator Deb Fischer have voiced strong support for the island’s freedom and its right to self-determination. Their statements come during a fact-finding trip to the region, aimed at assessing the security situation amid heightened military pressure from China, which seeks to assert its control over Taiwan.

UK Banks Under Fire: Shares of British financial services firms are facing selling pressure due to investor concerns over potential tax increases. The government is exploring options to address a 20 billion GBP ($26.9 billion) budget deficit, and a recent think tank proposal to raise taxes on bank profits has fueled fears that the sector will bear a significant burden. This approach signals a potential policy shift, as the governing party appears to be moving away from the idea of a wealth tax to instead concentrate fiscal measures on specific industries.

Taliban-Pakistan: The Taliban has warned of retaliation against Pakistan after airstrikes hit two provinces in Afghanistan. The strikes, which Pakistan is believed to have conducted, threaten to escalate tensions between the two Muslim nations. Pakistan has accused Afghanistan of sheltering militants responsible for recent terrorist attacks on its soil. While the conflict is likely to remain localized, it contributes to the broader instability that has kept global oil markets on edge.

Business Cycle Report (August 28, 2025)

by Thomas Wash | PDF

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. The intention of this report is to keep our readers apprised of the potential for recession, updated on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

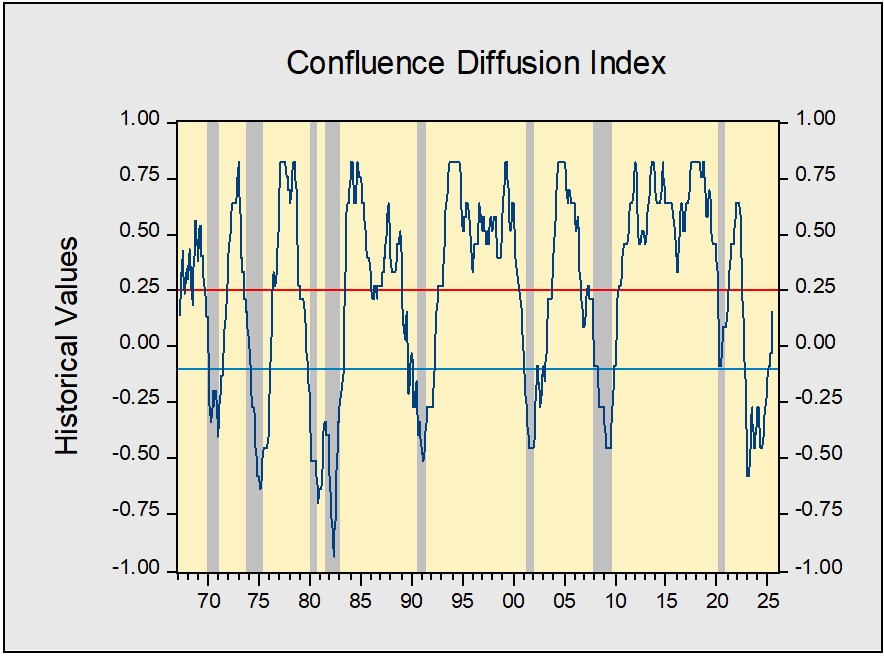

The US economy sustained its expansion in July, and our proprietary Confluence Diffusion Index stayed out of contraction territory for the sixth straight month. Two indicators entered expansion territory, which helped lift the overall diffusion index. Despite initial concerns, the equity markets were positively affected by the reduction in trade uncertainty. Bond markets, however, showed concern about the potential removal of Federal Reserve Chair Powell. Signs of improvement were also seen in the real economy, with both business spending and construction showing growth. The labor market remained stable but did show some signs of weakening.

Financial Markets

Equity markets are proving resilient, with the ongoing trade friction having little apparent impact on investor sentiment. This optimism has spurred a rally, led by strong performances in the Utilities and Information Technology sectors. In the bond market, yields are rising, a reflection of growing investor unease over a potential threat to the Federal Reserve’s independence. The concern is that if its autonomy is compromised, the Fed could be pressured to prioritize maximum employment over its core mandate of price stability, an outcome that would have significant implications for monetary policy.

Goods Production & Sentiment

July brought encouraging signs of resilience across key economic sectors. The goods production and sentiment segments notably improved, marked by the first expansion in our indicator that tracks the three-month average of new orders for core nondefense capital goods since 2022. This industrial strength was complemented by a significant jump in housing starts, driven by a pivot toward larger multi-family projects. Furthermore, consumer confidence rebounded noticeably as expectations began to normalize following earlier tariff-related shocks, although the indicator remains in contraction territory.

Labor Market

The labor market was the sole category exhibiting signs of weakness, but conditions remain broadly healthy. A slight increase in the unemployment rate weighed on the index, pulling it further into contraction territory. However, downward revisions to July’s nonfarm payrolls pushed the indicator to just above the contraction threshold. Some of this weakness is attributable to firms adopting a more risk-averse approach amid ongoing trade uncertainties; this should improve as greater policy clarity emerges.

Outlook & Risks

The economy is on solid footing, with some metrics reaching post-pandemic highs. This trend is expected to continue, provided policy remains predictable. Markets are likely to focus on the potential for monetary easing. While lower rates could mitigate the impact of tariffs on businesses, they also risk fueling inflation by stimulating consumption. Consequently, we are cautiously optimistic on risk assets due to strong fundamentals but await confirmation that this growth is sustainable for the medium term.

The Confluence Diffusion Index for August, which encompasses data for July, remains well above the recovery indicator. However, two of the 11 benchmarks remained in contraction territory from last month. Using July data, the diffusion index rose from -0.0303 to +0.1515, above the recovery signal of -0.1000.

- Equities softened due to trade tensions but remain elevated.

- Business spending showed signs of picking up.

- Revisions hurt job numbers but not enough to enter contraction territory.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is in recovery. The diffusion index currently provides about six months of lead time for a contraction and five months of lead time for recovery. Continue reading for an in-depth understanding of how the indicators are performing. At the end of the report, the Glossary of Charts describes each chart and its measures. In addition, a chart title listed in red indicates that the index is signaling recession.

Daily Comment (August 28, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment begins with our analysis of Nvidia’s recent earnings and what they suggest about the ongoing AI boom. We then examine key global developments, including a strategic move by US allies to boost investment in rare earths production, Mexico’s decision to raise tariffs on Chinese goods, and a discussion of a recent Russian attack that damaged buildings housing EU officials. The report concludes with an overview of other critical domestic and international factors shaping the current financial landscape.

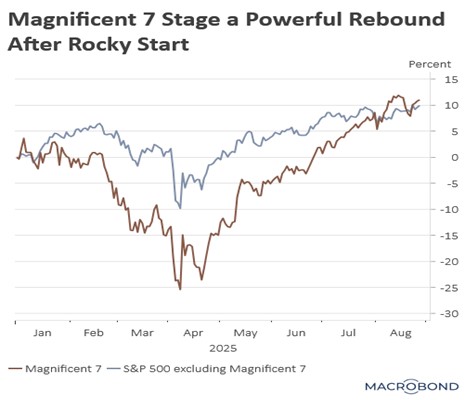

Tech Momentum: Nvidia, the world’s largest chipmaker by market capitalization, reported another strong quarter, demonstrating that the AI boom continues to offset the headwinds from trade friction. The tech giant’s revenue reached $46.7 billion in the previous quarter, a notable increase from $46.1 billion. Despite this success, concerns persist about the sustainability of AI-related spending. There are also doubts surrounding its sales to China due to US government regulations and scrutiny from Beijing.

- Despite strong quarterly results, Nvidia struck a cautious note by forecasting a sales deceleration. This near-term pessimism contrasts with its long-term optimism for AI spending, which it estimates will reach $3-4 trillion by 2030. The warning was underscored by data center revenue of $41.1 billion, which narrowly missed estimates of $41.3 billion, suggesting companies may delay investments in large-scale AI infrastructure if financial returns fail to materialize.

- This cautious outlook raises concerns about the AI boom that has fueled equity markets over the last three years. A recent MIT study showed that 95% of AI deployments fail to significantly boost revenue or productivity, validating concerns that the AI rally may be overdone. While the low success rate has been attributed to poor implementation rather than the technology itself, it suggests infrastructure investment is outpacing companies’ ability to use it effectively.

- While it may be too soon to declare the AI rally over, we believe it is prudent to identify opportunities in other market segments. In fact, excluding the Magnificent 7, the broader S&P 500 has performed quite well. This strength is partly due to shifting sentiment around trade policy, but more attractive valuations have also been a key driver. Consequently, we view this as an opportune moment to broaden investment exposure.

US Rare Earths Mining: Lynas, the world’s largest rare earths miner outside of China, is planning to raise $500 million to fund an expansion of its operations and acquire a stake in US magnet manufacturers. This strategic move is part of a broader effort by the US and its allies to establish a rare earths supply chain independent of China, which currently dominates the market. The move is another sign of the government’s growing involvement in the broader economy.

- In a significant effort to incentivize domestic production and reduce reliance on China, the US government has taken a major step in the rare earths market. Earlier this month, the Department of Defense entered into a public-private partnership with MP Materials, the American company that operates the country’s only active rare earth mine. It also established a price floor for key rare earth minerals at nearly double the current market rate.

- The increasing government intervention suggests that companies aligning with US policy objectives may receive preferential treatment. While this could benefit key sectors like industrial materials and technology in the long run by bolstering domestic production, it also makes these industries highly vulnerable to shifts in government leadership and policy changes.

Mexico Takes on China: The Mexican government plans to raise tariffs on Chinese goods, a move that aligns with the recent strategy of the US. Although specific rates are undisclosed, the new levies are expected to target Chinese cars, textiles, and plastics. This decision appears to be part of a broader, long-term strategy to use tariffs to force its allies to present a united front against Beijing. The goal is to counter Chinese export dumping, a practice used to address its domestic industrial overcapacity.

European Sanctions: The EU is prepared to reimpose sanctions on Iran for its failure to hold talks about its nuclear program. This move would allow the EU to penalize Iran under the snapback mechanism in the 2015 Iran Nuclear Deal. Since the attack on its facilities earlier this summer, Iran has been unwilling to resume negotiations and has not allowed access to its nuclear sites or stockpiles of 60% highly enriched uranium. While the sanctions are designed to pressure Iran’s economy and may provoke a response, the risk of near-term direct conflict remains low.

The Three Amigos: In a move signaling a unified front against what they perceive as a US-led international order, North Korean leader Kim Jong Un is set to join Russian President Vladimir Putin and Chinese President Xi Jinping at a major military parade in Beijing. This marks the first time all three leaders will attend an event together. The gathering takes place ahead of anticipated talks between each of these nations and the White House on key issues including trade, conflict, and restoring diplomatic communication.

Russian Attacks Continue: Buildings housing the EU and British Council in Kyiv were damaged in a Russian drone attack that killed at least 10 people and injured 48. Although the buildings may not have been the primary target, the EU and UK are likely to view the incident gravely and could respond with additional sanctions. The attack on diplomatic premises signals a concerning escalation, though it falls short of an action that would provoke a direct military conflict between the EU and Russia.

Milei Controversy: Argentine President Javier Milei was forced to abruptly end an election campaign event on Wednesday after protesters threw stones at him. The unrest follows allegations that members of his administration, including his sister, received illegal kickbacks from the drug distributor Suizo Argentina. This controversy has triggered a sell-off in Argentine equities, as investors express concern over the potential impact on the upcoming election scheduled for October 26, 2025.

Daily Comment (August 27, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment begins with an analysis of the escalating feud between the White House and the Federal Reserve. Next, we examine key global developments, including an unexpectedly strong consumer confidence reading for August, new US commitments for supporting Ukraine in its post-war security, and the imposition of fresh tariffs on Indian goods. We conclude with an overview of other critical domestic and international factors shaping the current financial landscape.

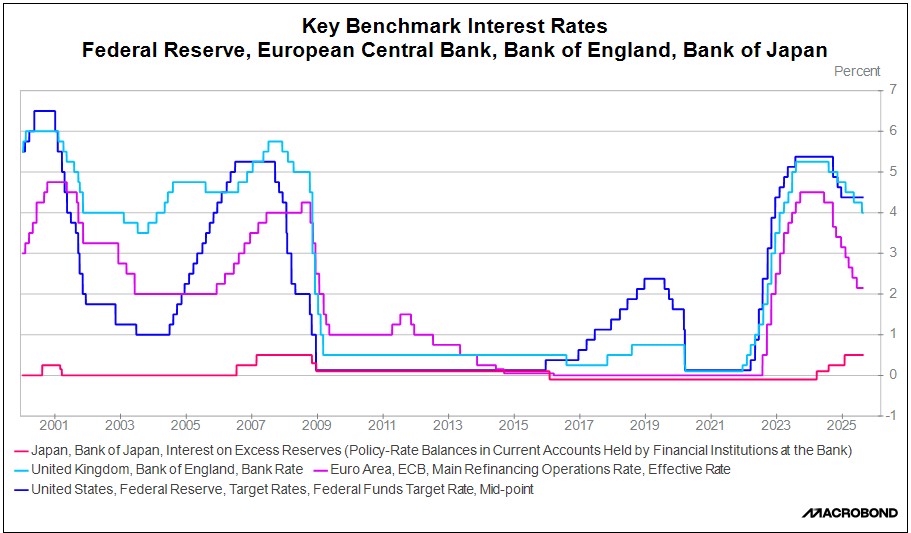

Reshaping the Fed: Uncertainty over monetary policy is causing the yield curve to steepen. Increased expectations of rate cuts have pushed down the short-term yields, while growing concerns about a potential shift away from inflation control has lifted long-term yields. This sentiment follows President Trump’s announcement that he will seek a replacement for Fed Governor Lisa Cook due to allegations of mortgage fraud. Although her departure is considered unsettled, the move signals that the administration intends to reshape the Federal Reserve.

- The administration is reportedly considering former World Bank Group President David Malpass as a potential nominee to replace Cook on the Federal Reserve Board. This effort coincides with the upcoming Senate confirmation hearing for Stephen Miran to fill a separate vacancy left by Adriana Kugler’s resignation. If he fills both positions, then the president would have appointed a majority of the sitting Federal Reserve Board governors, potentially giving him more control of its objectives.

- Lisa Cook’s lawyer has stated that she will file a lawsuit to challenge her removal by the president, arguing that the action is unlawful. This legal battle could allow her to remain in her seat and participate in upcoming Federal Open Market Committee (FOMC) meetings, including the one scheduled for September 16-17. The Federal Reserve has issued a statement on the matter stating that it will comply with any judicial ruling on the matter.

- By appointing loyalists to the Federal Reserve Board of Governors, the White House appears to be pressuring Chair Jerome Powell. This strategy has a historical basis as a chair’s role becomes untenable without the board’s support. The last significant resignation of this kind was in 1979 when G. William Miller stepped down after reportedly failing to mesh with his fellow governors.[1]

- Increased executive branch control over the Federal Reserve would likely have a ripple effect on both the dollar and the bond market. Doubt about the central bank’s ability to independently combat inflation could prompt foreign investors to reduce their exposure to US assets. Such a move would be a strategic effort to mitigate risk in a potentially inflationary environment.

Consumer Confidence: The Conference Board’s August consumer confidence index surpassed expectations, despite a month-over-month decline. This more optimistic reading was influenced by an upward revision of the previous month’s report, indicating that consumers were more confident in July than initially thought. However, there is growing pessimism about the labor market among households. While this could signal consumers becoming more cautious, there is no evidence of widespread layoffs.

Chip Wars: Chinese chipmakers are set to triple their production of AI processors by next year, a strategic move by Beijing to lessen its dependence on advanced US chips. This aggressive expansion follows the US government’s decision to tighten restrictions on chip sales to China, which has significantly impacted companies like NVIDIA. The escalating competition for AI supremacy is expected to be a major factor shaping market trends in both the US and China.

Energy Strain: The rise in utility prices, driven in part by energy-intensive data centers, is impacting a growing number of households. As electricity costs escalate, an increasing number of regions are voicing concerns. In response to these pressures, some companies are exploring alternative energy strategies. For example, Meta is reportedly investing in a new $50 billion data center and developing its own energy plan to help mitigate these rising costs. We think this could present opportunities for energy companies in the future.

Ukraine Postwar Backing? The US has announced its readiness to contribute to a European-led defense shield in a post-war Ukraine. This commitment would include providing intelligence assets and offering battlefield oversight. This agreement is part of what appears to be an intensified US effort to broker a deal that could end the conflict between Ukraine and Russia. The shift in US policy follows recent statements from Vice President J.D. Vance, who indicated that Russia’s President Putin has also made some concessions.

India Tariffs: On Wednesday, the US imposed secondary tariffs on goods from India, a move that has put pressure on the Indian economy. The tariffs, set at 50%, are designed to penalize India for its continued purchase of Russian oil. In response, Indian firms are seeking government support to manage the financial burden of these new levies. India’s prime minister has encouraged citizens to “buy domestically” to mitigate the economic impact, but it remains uncertain whether this strategy will be sufficient without additional government aid.

EU Removing Tariffs? EU officials are reportedly preparing to pass legislation that would eliminate tariffs on all US industrial goods. This move is intended to persuade the US to lower its current 27.5% tariff on European automobile exports to a more favorable rate of 15%. The automotive industry, which is a key export for the European Union (particularly for Germany), has been under significant pressure from the elevated US tariffs. If the legislation is approved, the new 15% tariff on autos could be applied retroactively.

Spy Allegations: Danish authorities have contacted US diplomats to address concerns that American individuals associated with the Trump administration are conducting influence operations in Greenland. The alleged objective of these campaigns is to rupture the relationship between Greenland and Denmark. This move aligns with the president’s publicly stated interest in bringing the strategically crucial Arctic Island under US influence. The allegations risk triggering significant diplomatic friction between the US and the EU.

[1] Greider, William. (1987). Secrets of the Temple: How the Federal Reserve Runs the Country. New York, NY: Simon & Schuster, p. 66.

Daily Comment (August 26, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with a quick overview of President Trump’s move to oust Federal Reserve Governor Lisa Cook. We next review several other international and US developments with the potential to affect the financial markets today, including the French government’s risky call for a confidence vote in September and new evidence that artificial intelligence is weighing on the US labor market.

US Monetary Policy: In a letter posted to social media last night, President Trump informed Federal Reserve board member Lisa Cook that he was immediately firing her for cause, citing allegations by Federal Housing Finance Agency Director Bill Pulte that she claimed two different properties as her “primary residence” in nearly simultaneous mortgage applications in 2021.

- Cook is likely to contest her firing in the courts. Nevertheless, if the firing stands, the president would be able to take a large step toward quickly reshaping the Fed policy board to his liking.

- If so, the Fed may start accelerating its interest-rate cuts relatively soon, helping bring US interest rate policy in line with the recent cuts from other major central banks, such as the European Central Bank and the Bank of England. That would probably give a boost to small-cap stocks, REITs, dividend payers, and cyclical equities.

- At the same time, the loss of Fed independence would likely be taken poorly by many investors, as it could portend excessively loose monetary policy and higher price inflation in the future. That could eventually push up longer-term bond yields and cap the positive impact on stocks.

France: Prime Minister Bayrou yesterday called a confidence vote on his government for September 8, in hopes that it will help push his deficit-cutting budget proposal through the divided parliament. However, the vote could also prompt the government’s downfall, paralyze policymaking, and/or usher in a right-wing populist government. French stocks and bonds are therefore selling off sharply for the second straight day.

United Kingdom: The leader of the populist Reform UK party, Nigel Farage, said in a major policy speech today that if his party comes to power, it will seek to take the UK out of the European Convention on Human Rights and start mass deportations of asylum seekers. Since Reform UK has been leading both the Conservatives and the Labour party in opinion polls, the statement suggests any future Reform UK government would enact a tough anti-immigration policy similar to that of the US government.

Russia-Ukraine Conflict: New reports say Ukraine’s stepped-up drone strikes on Russia oil refineries have led to gasoline shortages, rationing, and price spikes in some regions. The jump in gasoline prices comes just as Ukrainian attacks on Russia’s airports and railroads have forced more of the country’s citizens to travel by auto. There is no sign that the hardships will force Russia to scale back its war against Ukraine, but the situation does suggest potential political problems for President Putin down the line.

United States-China: President Trump yesterday said he is prepared to allow 600,000 students from China to study in the US each year, more than double the current quota. The statement came one day after the Chinese Embassy in Washington warned that students should be wary about intrusive immigration checks when arriving through Houston. The new quota of 600,000 student visas could be a negotiating offer to help achieve a new US-China trade deal, reflecting the administration’s new-found appreciation for China’s strong leverage in the negotiations.

US Trade Policy-Digital Services: In a social media post last night, President Trump warned that he will impose “substantial additional Tariffs” and restrict US advanced technology exports to any country “with Digital Taxes, Legislation, Rules, or Regulations,” which he said are discriminatory against US tech firms. Separately, reports say the White House is mulling the imposition of visa restrictions and other sanctions on EU officials enforcing such rules.

- The president’s warning comes despite previous indications that the new US-EU trade deal didn’t touch Europe’s digital services tax or other technology regulations.

- Therefore, it will likely rekindle investor concerns about the unpredictability of policy changes coming from the administration.

US Trade Policy-Lumber and Wood Products: The White House yesterday clarified that furniture is included in its probe of dumped lumber, wood, and derivative products, which was announced March 1. The clarification followed a statement by President Trump on Friday that the investigation would soon lead to unspecified tariffs on imported furniture. In response, furniture importers such as Wayfair and Williams-Sonoma experienced sharp drops in their share prices yesterday.

US Labor Market: New research from Bank of America shows that workers who switched jobs in the last year are now seeing no better wage growth than workers who stayed in their positions. For both cohorts, average wages are now up 4.3% from a year ago. As recently as early 2023, job switchers’ wages were up almost 8.0% year-over-year, while job stayers’ wages were up only about 5.5%. The changed dynamics are additional evidence of weaker labor demand, which could help ensure the Fed cuts interest rates in September.

- Separately, three Stanford economists today released a study showing “clear” evidence that artificial intelligence is crimping the demand for young workers in particular fields.

- Based on anonymized data related to millions of employees at tens of thousands of firms, the research finds that younger workers now make up a much smaller share of total employment in heavily AI-exposed occupations, such as software development. That is consistent with other recent reports suggesting firms are cutting their hiring of younger workers with college degrees.

Bi-Weekly Geopolitical Report – Tariff Trilemma: The Three Rs Driving US Trade Policy (August 25, 2025)

by Thomas Wash | PDF

Not all tariffs are created equal. Throughout the history of the United States, tariffs have been employed to achieve three primary objectives: (1) to pressure other governments into lowering their own trade barriers, (2) to generate revenue, and (3) to protect domestic industries. While ideally these goals would be achieved simultaneously, trade policy often presents a “trilemma,” where pursuing two of these objectives comes at the expense of the third.

This report explores the distinct types of tariffs, their impact on financial markets, and what recent trade developments indicate for the future of the American economy. As always, we wrap up with the implications for investors.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Daily Comment (August 25, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with a couple of notes on the global supply of rare-earth minerals, which are critical for many of today’s advanced technologies, weapons systems, and economic prospects. We next review several other international and US developments with the potential to affect the financial markets today, including growing tensions between China and Vietnam in the South China Sea and Federal Reserve Chair Powell’s notable speech last Friday.

China: In a little-noticed announcement on Friday, the Chinese government further tightened its control over the country’s rare-earth mining and processing industry. Most important, China’s system of export quotas for rare-earth materials will now apply not only to materials produced domestically, but also to those coming from abroad for refining. For example, companies in the rare-earth supply chain will face detailed new reporting requirements every month regarding their flows of rare-earth materials from both domestic and foreign mines.

- It is widely recognized that China holds extensive rare-earth reserves and has many large, productive mines, but its stranglehold over the world’s supply of rare-earth materials comes mostly from its near monopoly on rare-earth refining. Even when countries in the West or elsewhere can mine rare earths, the bulk of the ore must be shipped to China for processing.

- With the new reporting requirements for importing, processing, and re-exporting foreign rare earths, Beijing will be able to strategically clamp down on the business and further crimp global supplies of the critical minerals, if it so chooses.

- It can’t be stressed enough that the US-China trade war this year has brought into high relief the enormous economic leverage that Beijing enjoys from its control over global rare-earth supplies. In our view, the new administration in Washington has rightly recognized the broad economic leverage that the US derives from the fact that so many countries are dependent on exporting to it. Now that it is facing Beijing’s concentrated leverage with rare earths, a key question is how the US will shift its approach to China.

Malaysia: In another little-reported announcement last week, Malaysia said it will ban the export of unprocessed rare-earth minerals to help spur the development of its processing industries. The government said it would instead encourage foreign investment in downstream facilities if the projects involve local mineral processing, job creation, and technology transfers. It also said the export of processed rare-earth metals would be encouraged. The development illustrates the growing rush of countries and firms into the rare-earth business.

Vietnam: Based on recent satellite imagery, the Center for Strategic and International Studies says Vietnam has significantly expanded its effort to build artificial islets on reefs and outcrops in disputed areas of the South China Sea. Importantly, the report claims Vietnam’s effort will likely surpass China’s controversial island-building activity in the area. The news portends sharper territorial tensions between the countries and greater potential for a future military conflict that could disrupt global financial markets.

Japan-South Korea: At a summit in Tokyo at the weekend, Japanese Prime Minister Ishiba and South Korean President Lee promised each other that they would work to deepen their recent cooperation on military and economic issues, putting their World War II acrimony behind them. Reflecting the two countries’ new warmth, Lee’s visit marked the first time a new South Korean president has gone to Japan before the US since Tokyo and Seoul normalized diplomatic ties in 1965. Lee now heads to the US for a meeting with President Trump.

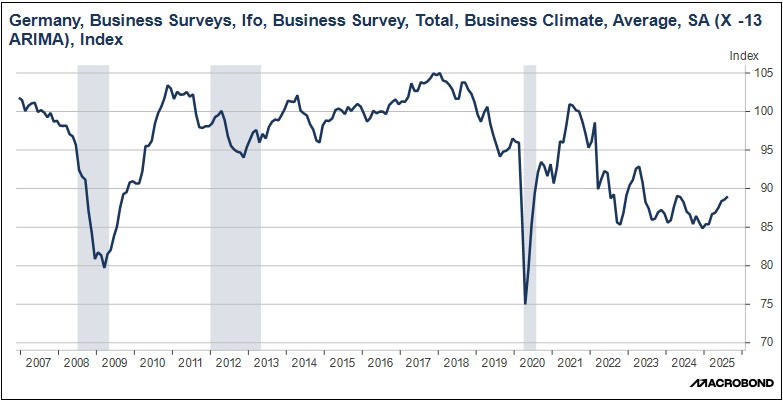

Germany: The IFO Institute today said its August business-sentiment index rose to a seasonally adjusted 89.0, beating expectations and marking its eighth straight monthly gain. The index of German businesses’ optimism about the future is now at its highest level since April 2024, despite the pressure from China’s excess capacity, the strong euro, slowing economic growth, and new US tariffs. The uptrend in optimism probably stems at least in part from Germany’s recent increase in defense spending and broader fiscal loosening.

United States-China: New reporting says Shan Liang, an award-winning HIV researcher and tenured professor at Washington University in St. Louis, will leave that institution to work in the Shenzhen Medical Academy of Research and Translation as director of its Institute of Human Immunology. Liang is the latest in a growing list of high-profile scientists leaving the US to return to his native China.

- We can’t confirm that the returns are more than in years past, but the large number of recent reports raises concerns about a widescale loss of talent to China that could threaten the US position in advanced science and technology. In turn, that could slow US economic growth and reduce investment opportunities over time.

- It also isn’t clear why more Chinese researchers might be returning to China. With the US-China geopolitical rivalry intensifying, some might feel less welcome here. China’s continued economic development could also be a draw. Other potential reasons could be more insidious. For example, Beijing may be pressuring or paying off Chinese researchers to contribute their talents to their home country. Some of the researchers could even be Chinese intelligence assets being repatriated to avoid arrest.

Canada-United States: Prime Minister Carney on Friday said he will remove Canada’s 25% retaliatory tariffs on a wide range of US food and other consumer goods, which were imposed by his predecessor. The US goods will enter Canada tariff-free starting September 1, so long as they comply with the standards of the US-Mexico-Canada trade deal. Removal of the tariffs should help reduce US-Canada trade tensions. The action is also expected to ease economic pressure on many of Canada’s small businesses.

US Monetary Policy: At the Fed’s annual symposium in Jackson Hole, Wyoming, last Friday, Chair Powell cautiously opened the door to a cut in the benchmark fed funds interest rate at the next policy meeting in September. As a result, futures trading suggests investors now see an 83.3% chance that the policymakers will implement a 25-basis-point cut next month and a high likelihood of at least one more cut by the end of the year.

- We think investors’ expectations for at least two rate cuts by the end of the year are reasonable, so long as incoming economic data cooperates.

- Importantly, the increased certainty of rate cuts appears to be broadening the stock market. For example, small-cap stocks saw out-sized price gains on Friday after Powell’s speech, while lagging large-cap sectors also performed well.

US Cryptocurrency Market: Banking lobbies such as the American Bankers Association have reportedly started warning US lawmakers that a loophole in the recent Genius Act could prompt bank customers to pull as much as $6 trillion of deposits from the banking system, tightening credit and raising interest rates. The provision in question allows crypto exchanges to pay interest to customers holding third-party stablecoins. The bankers’ complaint highlights the risk that stablecoins will draw funds from the banking system and potentially destabilize it.

Daily Comment (August 22, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment begins with new data that is showing a resurgence in US economic activity this month. Next, we delve into several pivotal global developments including the EU’s push to create a digital euro, the growing trend of tariff evasion through transshipment, and the mounting pressure on postal services to implement new trade rules. We will conclude with an overview of additional global and domestic factors shaping the financial landscape.

Stronger Growth: On Thursday, the S&P Global PMI data revealed that US economic activity accelerated in August, exceeding market forecasts and fueling optimism for a strong third quarter. The composite PMI, a key indicator of business sentiment, rose to 55.4 from July’s reading of 55.1. A value above 50 signifies economic expansion, while a reading below 50 indicates contraction. The growth is likely to add to optimism that the economy is in good shape despite tariffs.

- The most notable surprise came from the manufacturing sector, where the PMI surged to 53.3 from 49.8, far surpassing expectations of 49.5. Similarly, the services PMI also beat forecasts, moderating slightly to 55.2 from 55.7 but still well above the anticipated 54.2.

- Still, there are reasons to be cautious about whether this will last. Much of the recent improvement was driven by companies increasing their inventories. A similar trend was seen in other areas, such as the UK, eurozone, and India, which also showed an increase in economic activity.

- Further compounding economic concerns is the potential for this new inventory buildup to exacerbate price pressures. Evidence from the latest PMI data shows that firms are already raising selling prices in response to increased costs — a trend publicly corroborated by Walmart’s announcement of impending price hikes on select products.

- While the resurgence in economic activity is positive, our focus now shifts to the consumer. We believe the key factor for continued corporate success will be their ability to protect margins, whether by passing higher costs to consumers or securing discounts from foreign suppliers. However, we will monitor closely for any signs of consumer resistance. Given the elevated risk level, we maintain our stance that investors should exercise prudence.

EU Digital Stablecoin: The European Union is accelerating its development of a digital euro, driven by a desire to maintain monetary sovereignty and compete with the United States’ progress on stablecoins. The US has recently passed the Genius Act, which facilitates the creation of US dollar-denominated stablecoins. This legislation, along with the growing dominance of private, US-backed digital currencies, has prompted the EU to expedite its own digital currency project.

- A key technical distinction between the projects lies in their underlying infrastructure. While the digital euro proposal favors public blockchain technology (such as Ethereum or Solana), which emphasizes transparency and accessibility, the anticipated US approach is expected to utilize a private, permissioned ledger.

- The move to develop a digital euro as a rival to potential US initiatives exemplifies how digital currency is becoming a new arena for global economic influence. A key economic incentive for these stablecoins is their potential to create demand for short-term government bonds. This could, in turn, facilitate the financing of mounting public debt.

- We will closely monitor the development of stablecoins, as they are becoming an integral part of the financial system. Their growth necessitates adaptation and has significant implications for both monetary and fiscal policy. This area demands attention, as it presents opportunities for new rewards but also carries the potential for unforeseen risks.

German Economy: The German economy contracted by 0.3% in the second quarter, a sharper decline than the initially reported 0.1%. This downward revision follows a strong first quarter, where robust export growth had pushed expansion to 0.3%, suggesting the recent contraction may represent a partial normalization. Nevertheless, persistent weaknesses in manufacturing and investment spending remain a concern, which will likely increase pressure on the government to introduce further stimulus measures.

H20 Chips: Nvidia, the world’s largest chipmaker, has reportedly paused production of its H20 AI chip. This move follows increased scrutiny from Chinese officials on companies buying the chips, sparking concerns about weak demand. Nvidia’s performance has been a key indicator for the broader AI boom, and its consistent ability to beat expectations has driven market sentiment. As the company prepares to report earnings next Wednesday, any perceived weakness could fuel market uncertainty. Despite this, the broader tech sector still appears to have momentum.

US Transshipments: In a bid to circumvent China’s 10% levy on US goods, American metal dealers are reportedly rerouting China-bound shipments through intermediaries like Vietnam, Mexico, and Canada. This strategy has emerged as a direct response to the tariffs, leading to a notable decline in the volume of metal exports shipped directly from the United States to China. While the full extent of this activity remains unclear, it highlights an important and evolving tactic in the ongoing trade dispute.

Global Postal Service: Postal services worldwide are halting certain international shipments to comply with a deadline for ending a key tax exemption. This follows the president’s elimination of the de minimis rule, which previously allowed low-value packages to enter the country without import tariffs. While the long-term impact is still unfolding, this change is likely to cause short-term complications and delivery delays as foreign shippers scramble to adapt to the new compliance requirements.

South-North Korea: South Korean President Lee Jae-myung is set to meet with President Trump to discuss a recent trade deal and security agreement. During the meeting, President Lee plans to urge President Trump to reopen diplomatic dialogue with North Korea. This push for renewed talks comes amidst ongoing efforts to address security concerns on the Korean Peninsula.

Chipmakers Safe: The Trump administration has decided against requiring companies that receive CHIPS Act funding to surrender equity in exchange. This decision follows the separate case of the administration offering direct aid to Intel in return for a stake. By removing this requirement, the administration is reducing a key deterrent for foreign companies considering major investments in the US, thereby strengthening the program’s economic impact.