by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment will first explore the divisions among Fed officials regarding the path of monetary policy. We will then examine other critical market developments, including China’s clampdown on purchases of Nvidia chips, the obstacles to a Russia-Ukraine agreement, and progress on EU-US trade talks. We will conclude with an overview of additional global and domestic factors shaping the financial landscape.

Fed Divided: Policymakers were deeply divided on the path of monetary policy due to concerns surrounding tariffs. Some Fed officials expressed concern that the tariffs would lead to increased inflation. Others, however, argued that more action was needed to support the economy, citing signs of a deteriorating labor market. A third group remained undecided on whether inflation or the labor market presented a greater risk to the economy. Despite the disagreement, the majority of officials ultimately concluded that inflation posed the more significant threat.

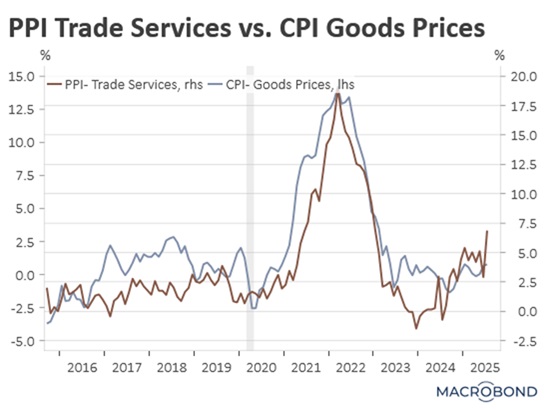

- The disagreement among policymakers comes at a critical time, as both aspects of the central bank’s dual mandate — maximum employment and price stability — appear to be at risk. Recent revisions to job payroll data have shown significantly slower job growth than initially reported. Concurrently, a higher-than-expected monthly rise in the Producer Price Index (PPI) has fueled concerns that input prices may soon translate into higher consumer prices.

- This monetary policy uncertainty is compounded by growing concerns over the central bank’s independence, following intense presidential pressure to lower interest rates. The situation escalated on Wednesday when President Trump called for Lisa Cook to resign over allegations that she falsified loan documents. This follows the president’s previous attempt to force Fed Chair Powell to step down amid accusations of misleading Congress about renovations to the Federal Reserve building.

- We maintain our expectation for the Fed to cut rates this year, with a September move appearing increasingly probable. The upcoming jobs report will be crucial as any confirmation of slowing job growth could tilt the committee toward a cut. Conversely, further signs of labor market strength would likely cause the Fed to keep rates on hold.

China and Nvidia: Chinese officials are seeking to curb domestic companies’ reliance on NVIDIA AI chips, following controversial remarks by US Commerce Secretary Howard Lutnick. Last month, Lutnick stated that US chipmakers were withholding their highest-quality chips from China, with the goal of making the country “addicted” to American semiconductors.

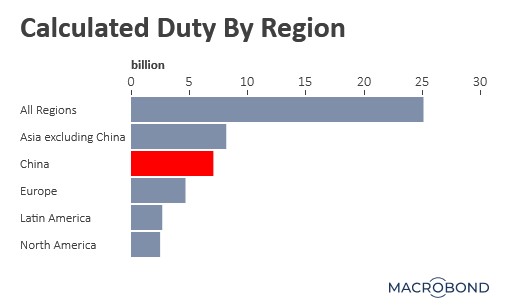

- In response, Chinese regulators have begun intensifying their scrutiny of domestic firms’ US chip purchases, aiming to encourage domestic alternatives. This action is a response to ongoing US efforts to secure concessions from trading partners through tariffs and restrictions. Earlier this week, the US Treasury secretary noted that China paid the most in tariff revenue. Furthermore, the US is reportedly negotiating a deal that would force chipmakers to pay a percentage of their revenue from their China sales to the US government.

- The ongoing US-China conflict is not merely an economic competition but also a clash of narratives. Beijing seeks to avoid any perception of submission to the US, an objective that runs counter to the Trump administration’s desire to demonstrate American dominance in its trade relationships. Although this dynamic will likely result in contentious discussions, it is unlikely to derail the possibility of a comprehensive agreement.

Eurozone Surprise Growth: Economic activity in the eurozone picked up in August, according to the latest PMI data. The key business sentiment indicator registered 51.1, exceeding expectations of 50. A reading above 50 indicates economic expansion, while a reading below 50 suggests contraction. This better-than-expected growth suggests the broader eurozone economy is on firmer footing, making it likely that the ECB will refrain from lowering interest rates at its next meeting.

Russia-Ukraine: US Vice President JD Vance hinted that a potential deal to end the war in Ukraine faces two major obstacles: providing security guarantees for Ukraine and resolving Russia’s claim over Ukrainian territory it does not currently control. Russia has rejected the initial proposal, demanding to be included in any security arrangement. Meanwhile, Ukrainian President Zelensky remains opposed to ceding any territory. As diplomatic talks continue, the US has hinted at future air support for Ukraine, even as Russia intensifies its offensive.

EU-US Trade Deal: The White House and the European Union have formally moved to implement a preliminary trade agreement, as outlined in a newly released joint statement. The agreement, which follows weeks of negotiation, links relief from US sectoral tariffs (on autos, pharmaceuticals, and semiconductors) to the EU’s meeting of specific benchmarks. A key component is a framework to address long-standing US objections to the EU’s digital services regulations. The agreement is likely to provide support to US and European stock markets.

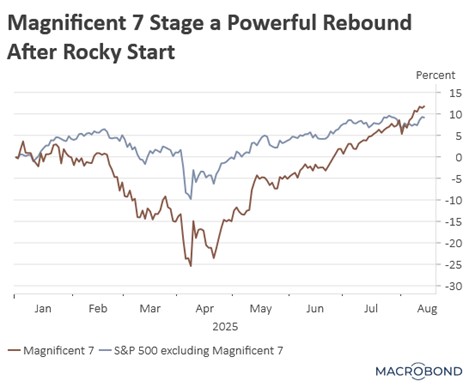

AI Spook: Meta has reportedly paused hiring in its AI division. While the freeze has been attributed to changes in the company’s organizational planning, it follows reports that its AI initiatives have failed to deliver solid revenue and productivity gains. Investors had already expressed concern that tech firms were prioritizing capital expenditure (CAPEX) at the expense of shareholder value. This tension is particularly acute given its elevated valuation, a situation that may fuel broader skepticism toward high-spending tech firms.

Walmart Confidence: Walmart, the largest US retailer, has raised its financial guidance, signaling strong confidence in the resilience of the American consumer. This optimistic forecast comes as the company reports success in mitigating price pressures from higher tariffs. While Walmart has absorbed some of these costs and passed others on to consumers, it has cautioned that price increases may become more noticeable as it replenishes inventory. Nevertheless, Walmart’s confidence is a positive indicator for the broader economy.