by Thomas Wash | PDF

Newly appointed Federal Reserve Chair Kevin Warsh is pushing for a clear regime shift, starting with a complete overhaul of the central bank’s communications strategy. This month, he appointed a task force led by two former central bank heads — Mervyn King of the Bank of England and Arminio Fraga of the Central Bank of Brazil — alongside Peter Fisher, a former executive vice president of the New York Fed. Their mission is to address a core critique Warsh has held for years: Is the Fed offering markets too much forward guidance?

Central to the issue is Kevin Warsh’s longstanding contention that excessive reliance on forward guidance can erode the Fed’s credibility. He argues that giving markets highly detailed signals about the expected path of policy can constrain the Fed’s flexibility to respond abruptly when conditions change. In his critique, the Fed’s repeated characterization of inflation as “transitory” during the 2021-2022 surge illustrates this problem as it conditioned markets to expect rates to remain lower for longer even as price pressures intensified.

While it is easy to criticize, let’s not forget how we got here today. Forward guidance, as we understand it today, is a relatively recent innovation. Although the Fed has long sought to shape market expectations through its communications, a more explicit and transparent approach did not emerge until the aftermath of the Global Financial Crisis (GFC). Confronted with the most severe economic downturn since the Great Depression, the Fed recognized the urgent need to engage more directly with the public and financial markets.

Under Chair Ben Bernanke, the Fed introduced quarterly post-meeting press conferences — a decisive move toward greater transparency. This new communication channel was intended to help build trust and bolster its authority as the Fed undertook unprecedented changes in its operations, including the adoption of quantitative easing and a zero-interest-rate policy. The evolution continued under Chair Jerome Powell, who expanded press conferences to follow every FOMC meeting as he sought to help return monetary policy to its pre-GFC normal. In doing so, Powell further institutionalized forward guidance as a central policy tool.

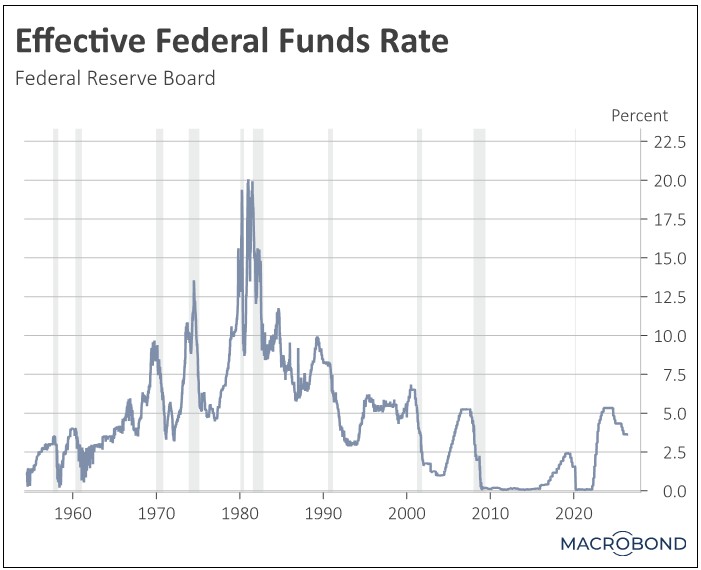

The post-crisis monetary regime appeared to function reasonably well until the pandemic struck in 2020. In the years leading up to COVID-19, the Fed gradually lifted the federal funds rate off the zero lower bound toward a more neutral level, while simultaneously initiating a measured reduction of its balance sheet. This shift moved the system from a crisis-era framework of “abundant” reserves to one of merely “ample” reserves. Episodes of market turbulence (most notably the funding-market strains in 2019) were met with a so-called “mid-cycle” rate adjustment and renewed balance-sheet expansion, yet these responses remained firmly within the boundaries of the existing policy toolkit.

That trajectory was abruptly upended by the first global pandemic in over a century, prompting a nationwide lockdown and a coordinated push by the Fed and the federal government to inject liquidity and avert a prolonged downturn. The Fed rapidly scaled up its crisis‑era tools and leaned more heavily on forward guidance, while rolling out new facilities to stabilize markets and support credit to households and businesses. In doing so, it extended liquidity well beyond the banking system, marking a notable shift from its traditional focus on backstopping distressed banks.

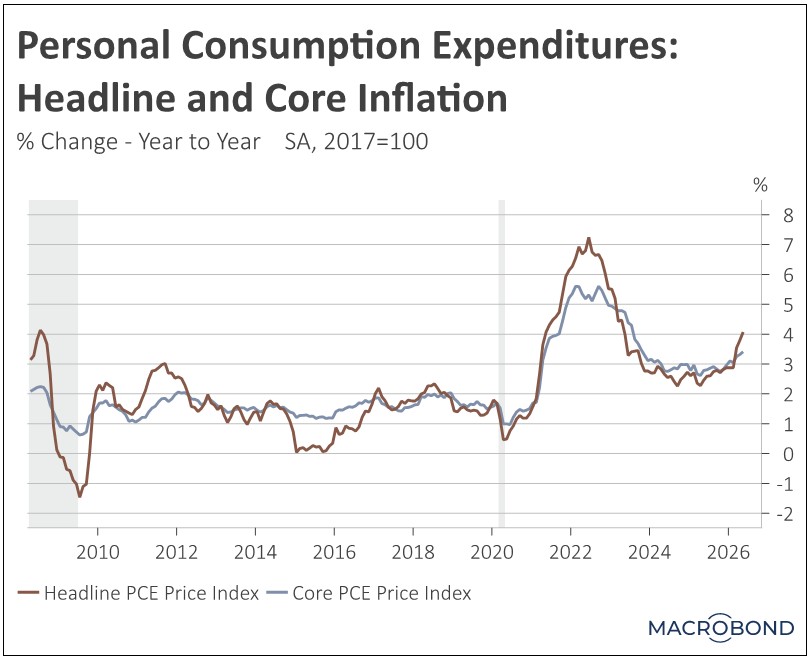

As COVID faded, the Fed confronted a new challenge of resetting policy for an economy emerging from the pandemic. During the early recovery, it effectively emphasized the maximum‑employment side of its mandate over the inflation objective, fearing that the end of lockdowns would still leave many workers struggling to reenter the labor force after prolonged layoffs and amid deep uncertainty about the durability of the rebound. As price pressures began to build, officials judged that much of the increase reflected uneven reopenings and temporary bottlenecks, which they expected to unwind over time, an assessment that led policymakers to famously label inflation as “transitory” and signal that rates would remain lower for longer.

However, as the recovery progressed and labor demand began to outstrip supply, a series of exogenous shocks — from the Suez Canal blockage to major ransomware attacks and, ultimately, Russia’s invasion of Ukraine — amplified the inflationary impulse already fueled by aggressive fiscal and monetary support. With inflation running well above its 2% target, the Fed was forced into an abrupt and politically costly U‑turn, abandoning its lower‑for‑longer stance and launching a rapid tightening cycle.

The decision to tighten created major complications as the Fed was widely perceived to be behind the curve on inflation. This perception contributed to an unprecedented spike in bond volatility. In an effort to regain its credibility, the Fed sought to hike rates more aggressively by moving from 25 basis points per meeting to 50, and then to 75. This rapid escalation only fueled further unease, offering no clear signal as to where the upper limit might be. Such uncertainty triggered a sudden run on regional banks like Silicon Valley Bank, which had mismanaged duration risk by relying too heavily on the Fed’s forward guidance.

As inflation showed signs of easing, the Fed restored some of the credibility that its earlier missteps had called into question, not only regarding its previous decisions but also its ability to provide reliable guidance on the future path of interest rates. However, its decision to lower rates in September was largely viewed as political, despite the Fed having provided hints in the previous meeting that the committee was leaning in that direction, largely because the move came so close to the election.

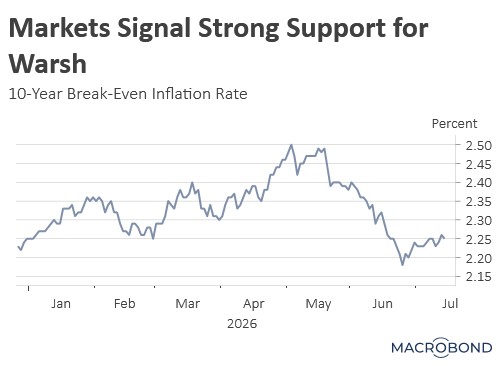

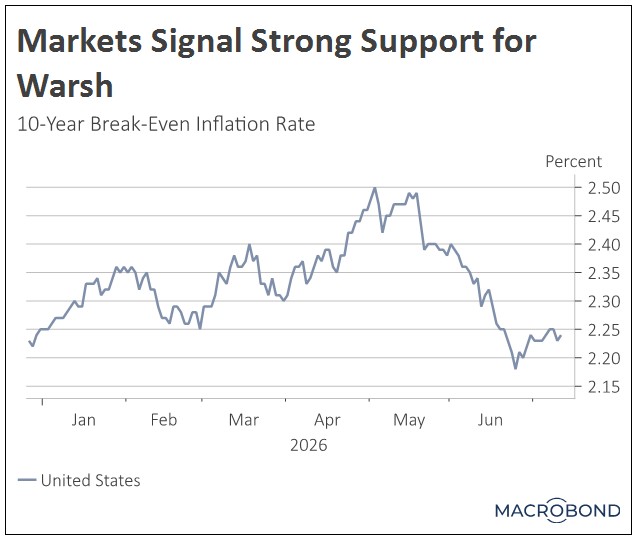

This perception of political bias became a major theme in the lead-up to Warsh taking over as Fed chair, as critics began to view monetary policy decisions as favoring a particular party. While that claim is debatable, it nonetheless became one of the key reasons why Warsh has decided to undertake a major revamp of Fed culture, beginning with its communications strategy. His hope is that reducing the Fed’s transparency, among other changes, could help restore its reputation and bring the Fed back to its pre-GFC stature. So far, markets appear to trust that he is the right person to do it.

In Conclusion

While it is impossible to know what conclusions the task force will ultimately draw regarding the Fed’s current communications strategy, recent experience suggests that a reassessment may be warranted. All things considered, reducing the use of forward guidance could enhance the Fed’s credibility as it works to achieve its dual mandate of price stability and maximum employment. However, the effectiveness of this shift will depend on the degree and the way guidance is scaled back. If the Fed becomes more selective, offering forward guidance only when it has a high degree of confidence in its policy path, it could strengthen its reliability, while still helping anchor expectations and contain bond yields. By contrast, a more aggressive withdrawal, either by eliminating forward guidance entirely or withholding it during periods of heightened uncertainty, could introduce greater volatility in fixed income markets and place upward pressure on yields.