by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with the latest chapter in President Trump’s tariff war with other countries, including big new tariffs on major trading partners including Japan and South Korea. We next review several other international and US developments with the potential to affect the financial markets today, including a decision by Trump to resume arms exports to Ukraine and a new executive order that will further weigh on the US green energy industry.

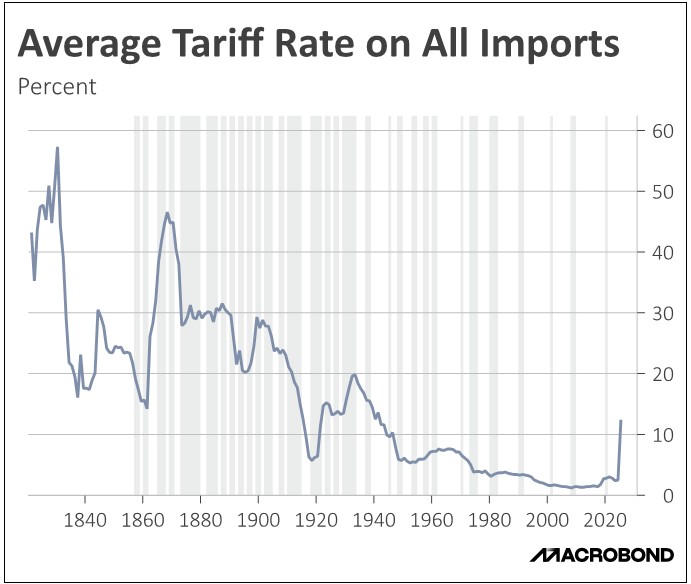

US Tariff Policy: As he promised, President Trump announced major tariff hikes yesterday for multiple countries that have failed to strike trade deals with the US during the 90-day pause that runs out tomorrow. The threatened new tariffs, which will take effect on August 1, include levies of 25% for Japan and South Korea, 30% for South Africa, and 40% for Laos and Myanmar. The high rates reignited concerns about trade wars and economic disruptions, driving risk asset values sharply lower yesterday.

United States-Ukraine-Russia: President Trump yesterday said the US will resume sending weapons to Ukraine to help it defend against Russian attacks. The turnaround follows public and private complaints by Trump that the Kremlin refuses to give up its maximalist territorial and political demands against Ukraine. In Trump’s words, “I’m disappointed, frankly, that President Putin hasn’t stopped.”

- As we and other observers have noted previously, it’s been unclear why Trump has long been so deferential to Putin and supportive of Russia, despite the country’s authoritarian political system and threats to US interests. Trump’s new statements suggest he may be reassessing the nature of Putin’s Russia and could potentially adopt a more mainstream view of the regime.

- As we noted in our Comment yesterday, Trump’s experience with trade negotiations since Inauguration Day also appears to have been a learning experience for him, highlighting the limits of US economic leverage and his own negotiating skill. Going forward, such learnings in geopolitics and economics could subtly shift Trump’s foreign policy toward something more akin to traditional US approaches, even if his rhetoric remains just as aggressive.

North Atlantic Treaty Organization: The Financial Times yesterday carried an article showing how the Dutch port of Rotterdam and the Belgian port of Antwerp are preparing for a potential war with Russia. The efforts are focused on identifying and reserving the port facilities that would be needed to move large amounts of military cargo from the US, the UK, and Canada onto the Continent in wartime. The planning is further evidence that Europe has gotten serious about rebuilding its defenses in the face of Russian aggression and uncertain US support.

Germany: The Ministry of Defense is reportedly mulling a massive 25-billion EUR ($29.3 billion) program to buy thousands of new armored vehicles and tanks to help outfit seven new combat brigades that Berlin has promised to add to the North Atlantic Treaty Organization’s defense capability over the coming decade. The plan would include up to 2,500 GTK Boxer infantry fighting vehicles and as many as 1,000 Leopard 2 main battle tanks, all of which would boost sales by top German defense industry firms, such as Rheinmetall.

United Kingdom: Prime Minister Starmer’s office yesterday declined to rule out tax increases on the rich to help fill the hole in public finances after parliamentary backbenchers in Starmer’s center-left Labour Party last week forced him to retreat on his planned welfare cuts. Analysts are now increasingly expecting Chancellor of the Exchequer Reeves to announce such tax hikes in her autumn budget statement. Expectations of higher taxes on the wealthy could further exacerbate the recent modest retreat in British stock values.

Japan-Philippines: New reports say Tokyo is mulling the transfer of one or more of its six Abukuma-class naval destroyers to the Philippines. If a deal is struck, it would mark Japan’s first transfer of a complete weapon system in decades. Pacifist legal restrictions had barred such transfers for many years, but the contemplated new deal shows how Tokyo is gradually dropping those limits as it tries to bolster its allies’ ability to help defend against Chinese aggression.

China: Little noticed amid the global news of war and trade disputes recently, General Secretary Xi and other top officials have launched a broad campaign against what they call “involution,” meaning excessive price competition arising from excess capacity and production. Excess supply, weak domestic demand, and now greater export barriers have put the country’s producer price inflation in negative territory since late 2022, putting many firms out of business and creating the risk of social disruption.

Australia: The Reserve Bank of Australia today voted 6-3 to keep its benchmark short-term interest rate steady at 3.85%, dashing expectations for a 25-basis point cut to 3.60%. In its policy statement, the RBA said conditions are sufficiently stable and that it can take more time to assess whether consumer price inflation remains on track to fall to the central bank’s 2.5% target. In response, the Australian dollar has appreciated 0.8% so far today, reaching $0.6544.

US Clean Energy Industry: After his “big, beautiful” tax-and-spending bill signed into law last week curtailed the Biden tax credits for green energy projects, President Trump yesterday signed an executive order tightening the standards that wind and solar farms must meet to be eligible for the remaining credits. While the law said facilities had to be “under construction” within the next 12 months to be eligible, the order says a “substantial portion” of the facility must be completed by the deadline. In response to the news, green energy stocks are trading lower today.

US Air Travel Industry: In a move that is sure to spark calls for a national day of celebration, the Transportation Security Administration is reportedly planning to end the rule that most airline passengers take their shoes off for screening before boarding a flight. The requirement is apparently the top complaint that travelers have with TSA. Passengers above the age of 75 and 12 or under are already exempt, as are those in TSA’s PreCheck program.