by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with a note on the Russia-Ukraine war, where Kyiv’s forces appear to be on the brink of losing their toehold in the Russian territory of Kursk ahead of planned peace talks. We next review several other international and US developments with the potential to affect the financial markets today, including new details on China’s latest economic stimulus plan and several new Trump administration initiatives in the realms of national security and foreign policy.

Russia-Ukraine War: Continuing their accelerated push over the last week, Russian forces this weekend nearly succeeded in reclaiming the Kursk region that the Ukrainians seized last summer to gain leverage in peace negotiations. It appears that Ukrainian forces could be pushed totally out of the Russian region at any moment. In addition, the Russians are reportedly threatening to surround an unknown number of Ukrainian troops remaining in Kursk, which would put Kyiv at a disadvantage during any talks.

South Korea: Shortly before the end of his term in January, President Biden reportedly put South Korea on a special list of countries that the US deems at risk of acquiring nuclear weapons. The Department of Energy confirmed the designation on Friday, suggesting that the Trump administration has endorsed the move. The news comes one month after South Korean Foreign Minister Cho Tae-yul said that Seoul has not taken nukes “off the table,” but that it has no specific plans to develop them right now.

- As we’ve noted before, rising geopolitical tensions and the US’s growing reluctance to meet its mutual defense promises under various treaties have begun to prompt a range of countries to consider developing their own nuclear weapons.

- In recent polls, some 70% of South Koreans have said they want their own nukes. To block such a move, the Biden Administration in 2023 struck a deal under which Seoul would put any such effort on ice in return for stronger US security guarantees.

- Biden’s designation of South Korea as a proliferation-sensitive state suggests that some political or military leaders in Seoul are still tempted by the possibility, which in turn would likely destabilize the Asia-Pacific region.

China: The State Council today provided a few more details on how the government will implement General Secretary Xi’s vow to “vigorously boost consumption” and “expand domestic demand in all directions.” According to State Council officials, the government will focus on raising incomes, stabilizing the real estate and stock markets, and improving medical and pension services. However, the officials gave few details on the actual planned spending, suggesting the latest stimulus program will again be too modest to truly boost growth.

- Separately, the state statistics agency said retail sales in January and February were up 4.0% from the same period one year earlier, accelerating from the 3.7% increase in the year to December.

- In response to the stimulus program and retail sales data, Hong Kong stocks today have posted a modest rise, while stocks in mainland China declined slightly.

United States-Yemen: The Trump administration on Saturday launched a series of strong airstrikes against the Iran-backed Houthi rebels in Yemen. According to military officials, the strikes are an escalation from those of the Biden administration and are expected to last up to several weeks to degrade the rebels’ ability to attack shipping in the Red Sea. Along with the strikes, President Trump also warned Iran that it must cease providing aid to the rebels.

- The US strikes came after the Houthis last Tuesday said that they would resume attacks on Israeli ships in the Red Sea, the Arabian Sea, the Bab el-Mandeb Strait, and the Gulf of Aden, ending a period of relative calm that began in January with the Gaza ceasefire.

- The strikes also came just days after Iran’s supreme leader, Ayatollah Ali Khamenei, rejected a Trump suggestion of talks aimed at stopping the country’s nuclear program.

US Military: Late last week, Defense Secretary Hegseth directed that the Pentagon’s storied Office of Net Assessments be dismantled. Under the order, military personnel working in ONA will return to their service and be reassigned, civilians will be moved to “mission critical” offices, and ONA contracts will be cancelled. The deputy secretary will then be tasked with developing a plan to rebuild ONA in a manner consistent with Hegseth’s priorities.

- Since being established in 1973, the ONA has operated as a kind of Pentagon think tank to identify and analyze long-term national security trends and lay the groundwork for strategies to respond to them.

- Hegseth’s dismantling of the ONA seems to adopt a “burn it down, then rebuild” approach to reforming the office. While the move is likely to produce near-term cost savings, it is also being panned for potentially creating a period when military planners won’t have an authoritative, deeply researched perspective to rely on.

- Coupled with other recent moves, such as directing large cuts in the defense budget and ordering massive job cuts at the Pentagon and CIA, pulling the plug on the ONA adds to the evidence that fiscal consolidation and bureaucratic reforms are President Trump’s highest priorities — perhaps much higher than even near-to-medium term national security.

US Foreign Policy: Over the weekend, President Trump announced that he has signed an executive order to slash funding and essentially shut down the US Agency for Global Media, which runs the Voice of America, Radio Free Europe/Radio Liberty, and Radio Free Asia. Those Cold War-era organizations were designed to beam uncensored information to closed societies, such as China and Russia, and to promote US values globally.

- According to Trump, the move to close down USAGM was necessary to save US taxpayers from supporting “radical propaganda.”

- In the latest federal fiscal year, USAGM’s budget was about $890 million.

US Trade Policy: The American Chamber of Commerce to the European Union today warned that the Trump administration’s draconian tariffs could hamper up to $9.5 trillion in US-European transactions. According to the Chamber, the developing trade war threatens not only the $1.3 trillion or so in trans-Atlantic goods trade, but also the $750 billion in trans-Atlantic services trade and some $7.5 trillion in sales by US and European cross-border affiliates.

- For example, the Chamber warns that either the US or the Europeans could retaliate for the other side’s goods tariffs by slapping tariffs on the other side’s services.

- Potentially more problematic, US companies with affiliates in Europe could find their European operations hindered by any tariffs on imported US inputs, and vice versa. That could discourage further foreign direct investment by the US firms in Europe or by European firms in the US.

US Visa Policy: The New York Times over the weekend said that the Trump administration is considering a list of 43 countries whose citizens would be barred or restricted from visiting the US. The long list includes countries such as Cuba, North Korea, Afghanistan, Belarus, and Somalia. The extensive list is even broader than the list of countries that Trump used to bar foreigners in his first term.

US Monetary Policy: Tomorrow, the Federal Reserve starts its latest two-day policy meeting, with its decision scheduled to be released on Wednesday at 2:00 PM ET. The policymakers are widely expected to hold their benchmark fed funds interest rate unchanged at its current range of 4.25% to 4.50%. Futures trading suggests that investors are now expecting two or three rate cuts of 25 basis points each this year, but the policymakers may hold their fire until consumer price inflation cools further, economic growth slows sharply, or both.

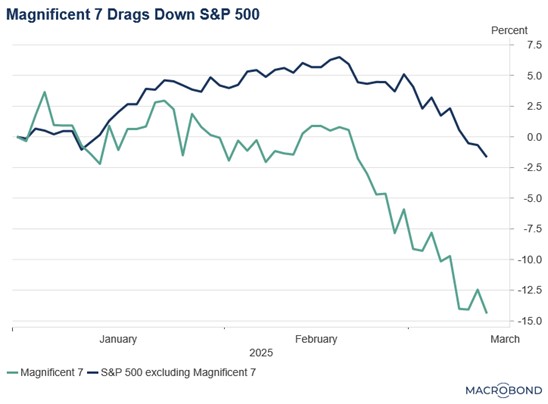

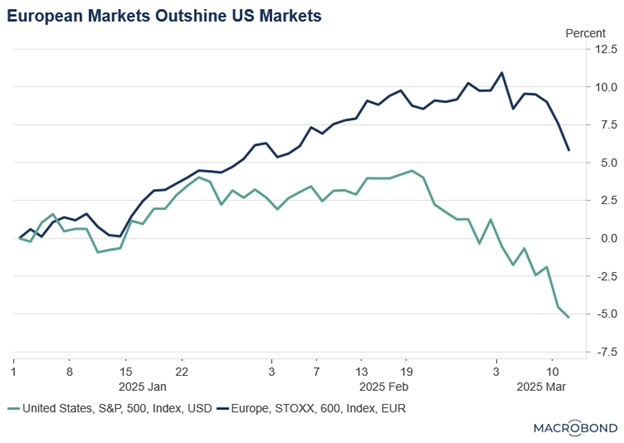

US Stock Market: In an interview yesterday, Treasury Secretary Bessent downplayed the significance of the US stock market slipping into a correction last week, saying simply that, “corrections are healthy . . . They’re normal.” The nonchalant tone of Bessent’s statement adds to the evidence that President Trump isn’t nearly as concerned now about market downturns as he appeared to be in his first term.

- Rather, it increasingly looks like the administration is willing to tolerate even steep declines in stock prices for what it sees as long-term economic benefits.

- Reflecting that realization, stock futures as of this writing are pointing to another day of falling prices.