by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment begins with our view on speculation that OpenAI may delay its IPO. We then turn to rising tensions over tolls in the Strait of Hormuz. Next, we briefly discuss Italy’s push to overhaul its electoral system and the US government’s decision to restrict the use of another AI tool. As always, we include a review of recent domestic and international economic data.

IPO Doubts: While robust earnings continue to buoy tech stocks, lingering valuation concerns are casting a shadow over the sector. On Thursday, The New York Times reported that OpenAI is considering a delay to its initial public offering, following advice that current sector volatility could dampen investor sentiment. The report is likely to intensify fresh worries that the sector has become frothy, underscoring a growing unease among investors regarding tech valuations and highlighting a shifting appetite toward other market sectors.

- The reported delay of OpenAI’s IPO appears tied in part to the recent performance of SpaceX. After an initial surge, shares in the Elon Musk–led company have fallen over 20% from their post-IPO high, declining from around $202 to roughly $153 as early enthusiasm faded. The pullback has raised concerns about the durability of demand for high-profile IPOs, particularly in segments where valuations are already stretched.

- Concerns are also mounting over the availability of liquidity to absorb new IPOs. Given the scale of the SpaceX offering — the largest on record — there is growing unease that retail investors may have limited capacity to support additional deals, particularly with Alphabet also planning its own equity issuance. The fear is that another large offering could prove too much for investors, who have already grown more risk-averse in recent months.

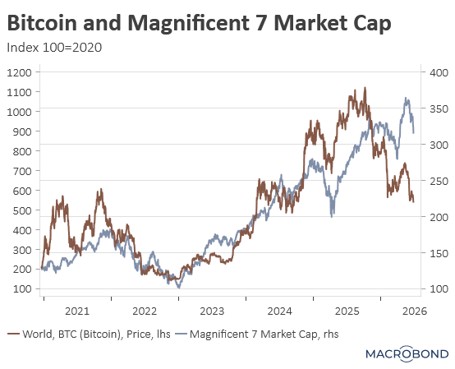

- Bitcoin, which is heavily influenced by retail sentiment, offers a useful barometer for shifts in risk appetite. During the post-pandemic period, bitcoin and the Magnificent 7 stocks largely moved in tandem. However, that correlation began to break down in late 2025, when bitcoin peaked and subsequently failed to recover. The Magnificent 7, by contrast, have also lost some momentum but have since managed to hit new highs.

- The decoupling of bitcoin and the Magnificent 7 likely underscores the primacy of earnings in today’s market. Mega‑cap tech companies have proven that, even with stretched valuations, underlying product demand remains resilient. This dynamic suggests that the AI‑led rally still has room to run in the near term, even if appetite for IPOs has begun to fade. That said, rising volatility across the space strengthens the case for adding exposure to sectors outside of tech as a way to diversify risk.

Strait of Hormuz: The reopening of maritime transit has come under strain as the United States and Iran continue to negotiate the terms governing passage through the strait. On Thursday, Iran reportedly intercepted vessels and forced them to turn back, insisting that ships not transit the waterway without prior authorization. The resulting uncertainty is likely to heighten concerns about the durability of the ceasefire, particularly as Washington and Tehran remain at odds over whether transit fees or tolls will be imposed.

- The dispute centers on Oman, a key US partner that also works with Iran on securing navigation in the Strait of Hormuz. On Thursday, Oman reportedly allowed internationally coordinated vessels to use a coastal corridor to facilitate passage, which Iran appears to view as violating its requirement that ships obtain prior authorization from its Persian Gulf maritime authority before entering the waterway.

- The episode underscores how much of the ceasefire framework over the strait relies on strategic ambiguity. Earlier in the day, Secretary of State Rubio reiterated that the United States will not accept Iranian tolls for navigating the waterway under any circumstances, a stance that appears to have prompted Tehran to adopt a more assertive posture in projecting control over the strait.

- While the recent conflict has introduced uncertainty, conditions in the strait are beginning to stabilize following the US-Iran ceasefire agreement. Earlier this week, oil prices retracted to pre-conflict levels, while transit volumes through the strait have recovered to roughly 25% of pre-war levels. This improvement suggests that, although the waterway remains contested, access has meaningfully improved relative to conditions just a few weeks ago.

- Rising geopolitical tensions over the strait are poised to drive further volatility in energy prices, as the probability of direct conflict between the two sides remains elevated. Although attacks on commercial shipping have reduced vessel traffic through the chokepoint, the ceasefire appears to be holding for now. This is largely attributed to the US reluctance to escalate militarily while the two sides negotiate a long-term agreement. That said, markets are expected to remain on edge until a final deal is formally secured.

Italy Vote Overhaul: Italian PM Giorgia Meloni is facing criticism over plans to overhaul Italy’s electoral system in ways that could favor her party in future elections. The proposal would grant a minority coalition additional seats if it secures at least 42% of the vote. Supporters argue that the change would enhance political stability by reducing fragmentation, while critics contend it is primarily designed to help Meloni consolidate power. The proposal reflects a wider pattern of incumbent governments tweaking voting rules to shore up their positions.

AI Tools Restriction: Security concerns are driving tighter limits on advanced AI systems. The White House has asked OpenAI to restrict its latest model, GPT‑5.6, to a small group of government agencies because of security risks. If implemented, this would be the first time a government has constrained release of a major technology before launch. The request follows earlier efforts to limit foreign access to Anthropic’s Fable 5 and Mythos 5 models, signaling a firmer government grip on frontier AI.