Author: Amanda Ahne

Asset Allocation Bi-Weekly – Let’s Talk About Tariffs! (November 11, 2024)

by the Asset Allocation Committee | PDF

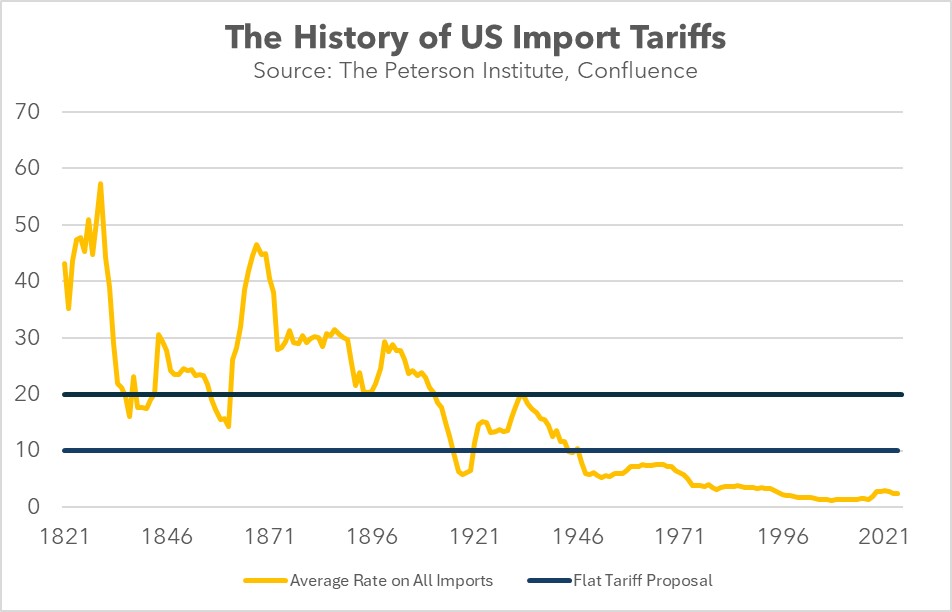

In recent years, tariffs have made a surprising comeback. Once widely condemned as a relic of the protectionist past, tariffs reemerged in 2016 as a policy tool against China and are now being considered for implementation on goods from all other countries. Populists tend to believe that these tariffs can be used to address a range of domestic economic issues, including persistent trade and fiscal deficits. They also generally believe that by leveling the playing field for domestic industries, tariffs can ultimately boost living standards for American households.

Under the new proposal, the US would impose a blanket tariff of 10% to 20% on all imports, with additional tariffs of 60% to 100% on goods from China. This would significantly increase the US’s average tariff rate to its highest level in nearly eight decades. The primary goal would be to protect US manufacturers and incentivize foreign companies to shift factory operations to the US, thereby creating domestic jobs. Furthermore, proponents believe that the increased tariff revenue could help reduce the US federal budget deficit. This proposed strategy has resonated with a substantial portion of the American electorate.

Despite its popularity with certain segments of the population, the proposal has faced significant opposition as it contradicts conventional economic wisdom. A tariff is a tax imposed on imported goods. Typically, it is levied as an ad valorem tax, which means it is calculated as a percentage of a good’s value. For instance, if the tariff rate were 10%, then importing a car valued at $10,000 would require paying a tariff of $1,000.

The potential increase in import costs has raised concerns about the proposal’s impact on price inflation. While businesses initially bear the cost of import tariffs, they can often pass a significant portion of this cost onto consumers in the form of higher prices. This economic phenomenon, known as tariff pass-through, is particularly prevalent for goods where businesses have significant pricing power. However, the extent to which tariffs can contribute to inflation and impact the overall economy varies.

When US consumers and businesses purchase foreign goods by paying in dollars, the foreign seller typically will exchange the greenbacks received for their own currency in the foreign exchange market. Therefore, increased US demand for foreign goods should lead to increased demand for foreign currencies, which in turn could weaken the US dollar. However, foreign countries often recycle their dollar holdings back into the US economy, in which case the foreign inflow can paradoxically buoy the dollar and widen the US trade deficit, or at least limit the dollar depreciation and the narrowing of the deficit.

For a flat tariff to successfully reduce trade and fiscal deficits without exacerbating inflation, the US would need to transition from a consumption-driven economy to an export-oriented one. US consumers would need to scale back their demand for tariff-laden imports and/or US producers would need to increase their exports. This shift would require the US to reduce its reliance on borrowing and become a net lender to the global economy. By increasing exports, the US could offset the negative impacts of tariffs and strengthen its economic position. Countries, like China, have achieved this transformation by implementing policies that encourage saving and discourage consumption, often at the expense of social safety nets.

The US dollar’s dominance as the global reserve currency could hinder an export-led growth strategy. Historically, large US trade deficits have supported the dollar’s role as other countries have relied on it for international transactions. To shift this dynamic, the US might need to diminish the dollar’s appeal. This could involve implementing capital controls, as many developing countries do, in order to restrict cross-border capital flows. Alternatively, the US could sacrifice monetary policy autonomy, either by pegging the dollar to another currency or by joining a currency union with other nations.

Because we don’t expect the US to make all the necessary adjustments to become more export-oriented, we believe that potential tariffs could induce foreign countries to devalue their currencies to offset the impact of the tax levy. Accommodative monetary policy could make this possible. This scenario would benefit US companies with limited foreign revenue, such as small and mid-cap companies, as their revenues would likely remain unaffected by currency depreciation. However, this could negatively impact US exporters that rely on foreign sales as the price of their goods could become less competitive.

Bi-Weekly Geopolitical Podcast – #56 “Rising US & Global Debt: A Perspective Check” (Posted 11/4/24)

Bi-Weekly Geopolitical Report – Rising US & Global Debt: A Perspective Check (November 4, 2024)

by Daniel Ortwerth, CFA | PDF

Concern has been rising across American society and throughout much of the world about the level of United States government debt. An increasing number of voices are sounding the alarm that the debt level is unsustainable, and crisis is on the way. Debates rage about how such a crisis will begin and when it will happen, but according to the alarmist view, the country will inevitably face financial catastrophe, with grave consequences for the security of the nation and the welfare of its citizens. Is this true? Are we really on a critical path, and is a catastrophic outcome inevitable? It is time to gather the facts and apply sound analysis to give ourselves a well-founded perspective.

This report uses standardized, internationally recognized data for 43 of the largest countries, from the beginning of the century to the present, to analyze US and global debt levels according to broadly accepted methods. It assesses the progression of debt levels across the period, between countries and country groups (i.e., developed and emerging) and between sectors of society (i.e., government and private). Our goal is to provide a fact-based sense of the situation and its trends. The report pays particular attention to the comparison between US and Chinese debt levels, since this plays a role in the geopolitical competition that has emerged. As always, we finish with implications for investors.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Business Cycle Report (October 31, 2024)

by Thomas Wash | PDF

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. The intention of this report is to keep our readers apprised of the potential for recession, updated on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

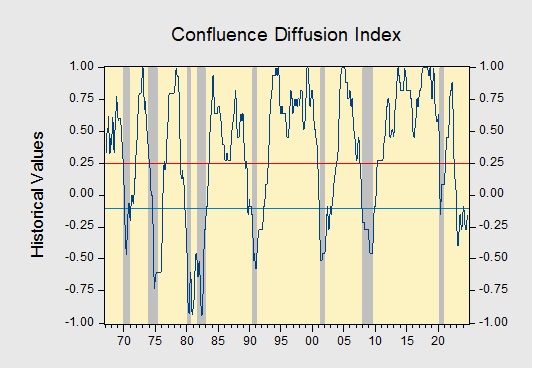

The Confluence Diffusion Index remained in contraction. The September report showed that six out of 11 benchmarks are in contraction territory. Last month, the diffusion index improved slightly from -0.2152 to -0.1515 but is still below the recovery signal of -0.1000.

- A drop in interest rate expectations helped to loosen financial conditions.

- The Goods-Producing sector is improving, but overall activity remains weak.

- The labor market continues to show resilience.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is in recovery. The diffusion index currently provides about six months of lead time for a contraction and five months of lead time for recovery. Continue reading for an in-depth understanding of how the indicators are performing. At the end of the report, the Glossary of Charts describes each chart and its measures. In addition, a chart title listed in red indicates that the index is signaling recession.

Asset Allocation Bi-Weekly – #128 “The Inflation Adjustment for Social Security Benefits in 2025” (Posted 10/28/24)

Asset Allocation Bi-Weekly – The Inflation Adjustment for Social Security Benefits in 2025 (October 28, 2024)

by the Asset Allocation Committee | PDF

Even for dedicated, successful investors who have built up a substantial nest egg, Social Security retirement and disability investments can be an important part of their financial security. For many Americans, Social Security benefits may be the only significant source of income in advanced age. On average, Social Security benefits account for approximately 30% of elderly people’s income and more than 5% of all personal income in the US. There is one aspect of Social Security that is especially important in the current period of higher price inflation: By law, Social Security benefits are adjusted annually to account for changes in the cost of living. In this report, we discuss the Social Security cost-of-living adjustment (COLA) for 2025 and what it implies for the economy.

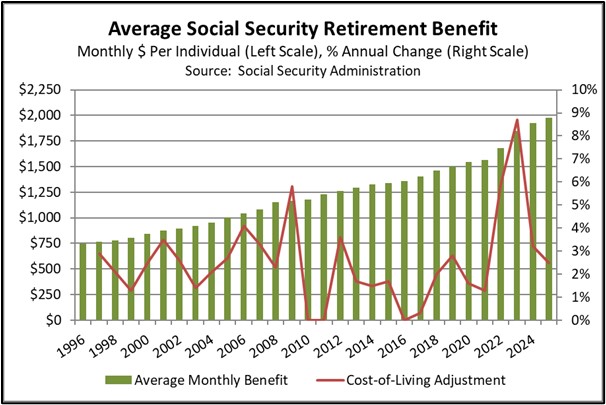

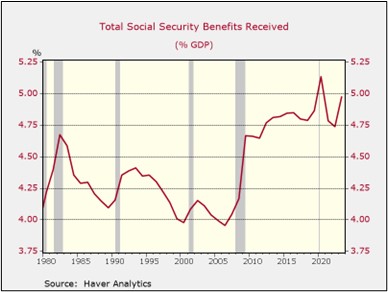

In mid-October, the Social Security Administration announced that Social Security retirement and disability benefits will increase 2.5% in 2025, bringing the average retirement benefit to an estimated $1,976 per month (see chart below). The increase, much smaller than those during the last couple years of high inflation, will bump up the average recipient’s monthly benefit by approximately $49. The benefit increase was right in line with expectations, given that it is computed from a special version of the Consumer Price Index (CPI) that is widely available. The COLA process also affected some other aspects of Social Security, although not necessarily by the same 2.5% rate. For example, the maximum amount of earnings subject to the Social Security tax was raised to $176,100, up 4.4% from the maximum of $168,600 in 2024.

Media commentators often fret that the Social Security COLA could be “eaten up” by rising prices in the following year, or that the benefit boost could provide a windfall if price increases decelerate. In truth, COLA merely aims to compensate beneficiaries for price increases over the past year. It is designed to maintain the purchasing power of a recipient’s benefits given past price changes with price changes in the coming year being reflected in next year’s COLA.

For the overall economy, the inflation-adjusted nature of Social Security benefits is particularly important. Since so many members of the huge baby boomer generation have now retired, and since more and more people are drawing disability benefits than in the past, Social Security income has become a bigger part of the economy (see chart below). In 2023, Social Security retirement and disability benefits accounted for 4.9% of the US gross domestic product (GDP). Having such a large part of the economy subject to automatic cost-of-living adjustments helps ensure that a big part of demand is insulated from the ravages of inflation, albeit with some lag. In contrast, if Social Security income were fixed, a large part of the population would be seeing its purchasing power drop sharply, which might not only reduce demand, but could also spark political instability. Of course, the additional benefits in 2025 will help buoy demand and keep inflation somewhat higher than it otherwise would be.

Finally, it’s important to remember that an individual’s own Social Security retirement benefit isn’t just determined by inflation. The formula for computing an individual’s starting benefit is driven in part by a person’s wage and salary history. Higher compensation will boost a retiree’s initial retirement benefit, which will then be adjusted via the COLA process over time. As average worker productivity increases, average wages and salaries have tended to grow faster than inflation, and as a result, the average Social Security benefit has grown much faster than the CPI. Over the last two decades, the average Social Security retirement benefit has grown at an average annual rate of 3.5%, while the CPI has risen at an average rate of just 2.6%. In sum, Social Security benefits provide an important source of growing purchasing power that helps buoy demand and corporate profits in the economy.

On the bottom line in our view, this year’s COLA announcement will prove to be market neutral. Although recipients may experience initial disappointment with this adjustment relative to those of recent years, the adjustment is actually more in line with those that came before the recent period of heightened inflation.

Asset Allocation Quarterly (Fourth Quarter 2024)

by the Asset Allocation Committee | PDF

- Our three-year forecast includes balanced economic growth, albeit at a slower pace than recent experience, and inflation settling above the Fed’s target rate.

- The Fed is expected to continue easing at a measured pace over the next year.

- We initiated a position in long-duration, zero-coupon Treasurys as a stabilizer amid potential global policy uncertainty and default risks.

- We continue to favor small and mid-cap domestic equities which offer appealing valuations and growth prospects relative to large caps.

- International developed equities remain in the portfolios, but we avoid emerging markets due to heightened risks.

- We preserve an allocation to gold as a hedge against geopolitical risks, with an allocation to silver where risk appropriate.

ECONOMIC VIEWPOINTS

Recent economic growth has been bolstered by a strong labor market, fiscal stimulus, and resilient personal consumption. We expect fiscal spending and continued strong labor markets to sustain growth during the beginning of the forecast period, both of which would support the consumer. While the overall business spending and personal consumption sentiment has been generally optimistic, momentum is slowing at the margin. The latest GDP report highlights that a part of the recent expansion stems from drivers that may be short-term in nature, such as inventory build-up ahead of a potential port strike. As we look ahead, we expect the labor market and consumption to be supported by easing monetary policy and lower inflation. The heightened uncertainty surrounding immigration policy could lead to a scenario where labor markets remain tight, which would continue to bolster household incomes. However, toward the end of the forecast period, consumption could moderate and potentially lead to increased uncertainty in the labor markets.

This first chart shows that while civilian unemployment, shown in red, has remained subdued at 4.1%, we are seeing some weakness with part-time work for economic reasons, shown in blue, ticking higher. Wage growth momentum has moderated but remains elevated compared to the pre-pandemic decade. It is worth noting that job openings have fallen as companies anticipate slower expansion, and a notable increase occurred in the long-term unemployed (27 weeks or more), which we anticipate will also be a drag on the labor markets.

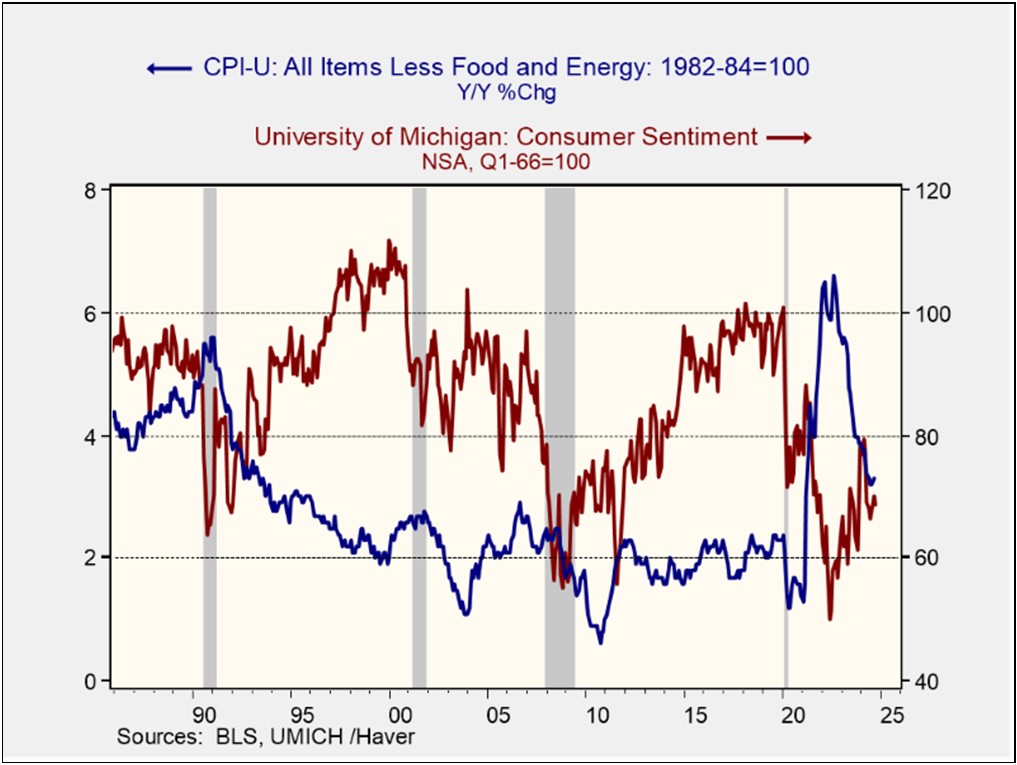

While the Fed’s 50 bps rate cut and expectations for further easing support the expansion, high prices and relatively low rates of savings have made consumers more frugal. Such economic uncertainty has the potential to lead firms to delay investment and households to postpone buying big-ticket items, actions which we have already seen to a degree. Consumer sentiment, shown in red on the second chart, has improved since inflation, in blue, receded from its cyclical peak in 2022. We expect consumption to moderate as households have depleted their stimulus-driven savings and have grown more concerned about future job prospects.

Additionally, the favorable tax treatments for individuals in the Tax Cuts and Jobs Act of 2017 are due to sunset at the end of 2025. While each of the presidential candidates has shown support for extending at least some part of the tax act for individuals, tax policy cannot be unilaterally controlled by the president. To extend these tax cuts, both houses of Congress must pass legislation. While individual tax breaks are set to expire, most of the favorable corporate tax treatments, including the reduction of corporate tax rates from 35% to 21%, do not sunset.

The US presidential election will take place this quarter, and while highly publicized, these elections generally have a limited long-term impact on financial markets. However, given the current political climate, we are taking precautionary measures. We maintain a position in gold as a hedge and have increased our exposure to long-dated Treasurys to mitigate potential risks. Either candidate is expected to govern alongside a divided Congress, which reduces the likelihood of abrupt policy changes.

STOCK MARKET OUTLOOK

We expect corporate profit margins to remain healthy during the forecast period but we’re closely monitoring earnings quality for signs of potential weakness. With moderate economic growth and stable margins, we are maintaining an even-weight position in equity risk. The record level of cash on the sidelines continues to support valuations as we’ve seen these funds flow into risk assets during market pullbacks. This suggests that investors remain generally comfortable with equity exposure but are mindful of valuation levels. Furthermore, as the Fed continues to ease, lower money market rates may drive more capital into equities.

We are even-weight on the growth versus value style bias. While we recognize the concentration risk in a few prominent growth stocks, we believe current economic conditions will support equities across the board. We’re overweight mid-cap equities due to attractive valuations. While small cap stocks also offer appealing valuations, many small caps face higher sensitivity to debt refinancing. To manage risk and focus on earnings quality, we hold a small cap quality factor position, screening for profitability, leverage, and free cash flow.

We also maintain an overweight in the Energy sector and uranium miners, driven by Middle Eastern geopolitical tensions and the global energy transition. Our exposure to military hardware and cyber-defense remains a strategic portfolio component.

International developed equities remain attractive due to valuation discounts. Many global market leaders in the developed world ETFs are trading at lower valuations compared to US large caps. However, due to concerns about European economic growth, we have reduced developed market exposure in some portfolios. We maintain targeted exposure to Japan, where ongoing shareholder-friendly reforms and continued capital inflows may drive multiple expansion. We continue to exclude emerging market equities despite steep valuation discounts as we believe the risks surrounding Chinese growth outweigh the potential returns.

BOND MARKET OUTLOOK

Expectations for fixed income markets largely depend on inflation trends. While we expect volatility of inflation to remain elevated, the likelihood of a spike to levels experienced in 2022-2023 is slim. Rather, we expect inflation to decline gradually but unevenly from those highs, though we find it unlikely that the Fed will achieve its 2% target level within our three-year forecast period. While this became the target during the period of zero rates of the past decade, we find that a level around 3% is much more likely.

Against the backdrop of inflation expectations, the Fed’s data dependency heralds the prospect for three-month rates to remain relatively elevated compared to two-year rates. This implies that, absent a significant economic shock or a deep recession, the yield curve is more than a year away from returning to a normal, positive slope across all maturities. Accordingly, we find a mix of maturities to be the appropriate exposures in the strategies as the process unwinds. Within sectors, we are underweight investment-grade corporates due to their historical tight spreads. However, we are overweight mortgage-backed securities (MBS), where low refinancing activity has created attractive pricing. Contrasted with investment-grade corporates, speculative grade corporates maintain an attractive spread of nearly +300 basis points. Nevertheless, some caution encourages our preference for the higher BB-rated bonds in this asset class.

Although the majority of the bond exposure in the strategies is in the short to intermediate section of the curve, the combination of heightened geopolitical risk, uncertainty surrounding the US legislative and presidential election outcomes, and resulting potential policy changes leads to the introduction of a modest exposure to long-term, zero-coupon Treasurys in most strategies, the intention of which is to act as a hedge against these risks. A long-duration bond may serve as a ballast against market volatility due to its inverse relationship with interest rates and its role as a stabilizing asset in a diversified portfolio.

OTHER MARKETS

We continue to hold a position in gold across all portfolios. Despite gold spot prices reaching record highs this year, we believe additional Fed interest rate cuts and continued central bank purchases could push gold prices higher. The gold position also offers a strategic layer of protection against volatility, given its historical role as a safe-haven asset during periods of geopolitical instability. In portfolios with higher risk tolerance, silver is retained as a complementary precious metal holding. While REIT valuations have improved and the prospect of lower interest rates should generally benefit the sector, we have ongoing concerns around debt refinancing challenges and property valuations that lead us to avoid this sector this quarter.

Keller Quarterly (October 2024)

Letter to Investors | PDF

“Will it play in Peoria?” That wonderfully alliterative question originated in the show business community. A show that might “knock ‘em dead” in New York might not be so popular in the rest of the country. We live in a big nation. While there is a commonality that binds us together, there are meaningful cultural differences. New York, Philly, Boston, and Miami all have their unique qualities, as do Houston, Denver, San Francisco, and LA. As I travel the country I’ve come to admire and enjoy all these mini cultures.

I’m thinking about Peoria, Illinois, because I’ll be visiting that town soon. I’ve been travelling there regularly for about 25 years because of the many friends and clients I have there. What gave rise to the idea that if a show does well in Peoria it will do well anywhere? Like much of the Midwest, Peoria is a place of easy-going, but hard-working and friendly people; people who don’t mind being characterized by words like calmness, perseverance, and normal. In a country where so many people seem to be lined up on the extremes of anything, Peoria provides a delightful middle. It’s neither too high nor too low. If the Peorians like it, mainstream America will love it!

What’s the point of this paean to a Midwestern disposition? I think it is the ideal temperament for successful long-term investing, and you don’t have to be from the Midwest to develop it. It’s important not to let oneself get too excited about something great or get too depressed about a negative development. I believe keeping one’s emotions in check is the single most important thing an investor can do. Investing should be a rational, thoughtful endeavor.

I’ve written before that the same emotions that make us human can be the enemies of successful investing. Emotional extremes generally lead to irrational decisions. There may be many reasons to get emotional about this year’s election, but, in my opinion, the impact on your portfolio should not be one of them. Neither party seems particularly interested in reducing federal spending or substantially increasing the tax burden on the US economy. Thus, we expect federal deficits to remain large no matter which party controls the purse. Both parties are likely to continue tariffs on a variety of Chinese goods destined for the US. Whatever their differences on non-economic issues, we expect that these economic policies, which we believe are inflationary, will remain in place.

As I discussed at length in my last letter (July 2024), the factors that have made the US an extraordinarily good place to invest are still in place and not likely to be affected by the national election. The recent Confluence Asset Allocation Bi-Weekly from September 30, 2024, exhibited data since 1930 indicating that stock market returns have shown virtually no preference for which party was in power.

I repeat what I wrote last quarter, quoting my letter from October 2020: The stock market is neither Republican nor Democrat but is solely interested in making money. In my opinion, the current environment is well-suited to doing just that, regardless of who wins the election.

As we’ve said for several years, we expect inflation rates to remain above the average of the last decade for the foreseeable future. In our opinion, this should be the investor’s primary concern. Our investment strategies, be they domestic equities, international equities, or asset allocation portfolios, have this expectation in mind: that inflation is likely to remain higher than investors expect. The professionals at Confluence Investment Management have experience investing in rising inflation environments. It’s not unknown to us, like Peoria.

We appreciate your confidence in us.

Gratefully,

Mark A. Keller, CFA

CEO and Chief Investment Officer