Author: Amanda Ahne

Bi-Weekly Geopolitical Report – Mid-Year Geopolitical Outlook: Uncertainty Reigns (June 17, 2024)

by Patrick Fearon-Hernandez, CFA, Thomas Wash, Daniel Ortwerth, CFA, and Bill O-Grady | PDF

As the first half draws to a close, we typically update our geopolitical outlook for the remainder of the year. This report is less a series of predictions as it is a list of potential geopolitical issues that we believe will dominate the international landscape for the rest of the year. The report is not designed to be exhaustive. Rather, it focuses on the “big picture” conditions that we think will affect policy and markets going forward. We have subtitled this report “Uncertainty Reigns” to reflect the fact that chaos and unpredictability have become entrenched as the post-Cold War era of globalization gives way to a new period of Great Power competition. Our issues are listed in order of importance.

Issue #1: China – South China Sea

Issue #2: Russia-Ukraine-NATO

Issue #3: Israel-Hamas-Iran

Issue #4: The US Elections

Issue #5: US Defense Rebuilding

Issue #6: Global Monetary Policy

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Asset Allocation Bi-Weekly – #120 “Copper, Gold, Treasurys, and the New World” (Posted 6/10/24)

Asset Allocation Bi-Weekly – Copper, Gold, Treasurys, and the New World (June 10, 2024)

by the Asset Allocation Committee | PDF

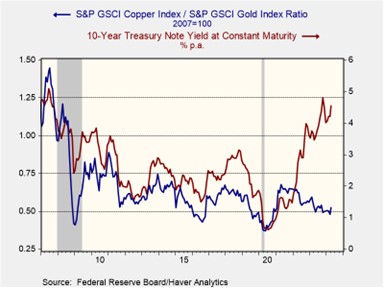

Early 2023 served as a stark reminder that correlations can break down when least expected. Last year, a decline in the copper/gold ratio led many investors to anticipate a fall in longer-term yields, particularly for the 10-year Treasury note. However, these expectations were shattered as yields not only increased but surged to multi-decade highs by October. This episode underscores the challenge of relying too heavily on old assumptions. In this report, we’ll delve into the dynamics between the copper/gold ratio and 10-year yields and explore whether this historical connection has been permanently severed.

The copper-to-gold ratio is a closely watched indicator of investor risk sentiment. This ratio compares the price of copper, an industrial metal heavily used in construction and manufacturing, to the price of gold, a traditional safe-haven asset. A rising ratio generally signals investor optimism about economic growth. As economic activity picks up, demand for copper rises and pushes its price higher relative to gold. Conversely, a declining ratio suggests investor pessimism and a potential economic slowdown. This could be due to fears of recession or other economic troubles, leading investors to seek the perceived safety of gold.

As shown in the chart below, a rising copper-to-gold ratio has historically coincided with increasing long-term Treasury yields. This reflects investor expectations of accelerating economic growth, which can lead to inflation. To compensate for the potential erosion in bond values, investors demand higher yields on longer-term bonds. The relationship also works in the opposite direction. Investor fears of geopolitical risks or recession trigger a decline in both the copper/gold ratio and bond yields as investors seek safety in gold and US government bonds.

The once strong correlation between the copper/gold ratio and interest rates seems to be unraveling in the post-pandemic recovery. While the ratio initially surged with the global reopening, China’s economic slowdown has caused it to fall over the last couple of years. In contrast, the 10-year Treasury yield has climbed as stubbornly high inflation has prompted central banks to tighten monetary policy, leading to further interest rate increases. This disconnect between the traditional indicators suggests a potential shift in market dynamics.

Prior to the pandemic, investors largely operated under the assumption of a stable, low-inflation world. This fostered an environment where long-term investments were attractive, and there was minimal fear that duration risk would erode their value. Consequently, investors primarily focused on the long end of the yield curve only during periods of economic concern or during major events that might prompt the Fed to cut rates and stimulate growth. This preference for bonds during economic downturns mirrored that of gold — a safe-haven asset. As a result, both bond yields and the copper-to-gold ratio had previously moved counter-cyclically.

However, these market relationships started to change as government efforts to prevent a recession through the creation of massive deficits led to higher long-term interest rates. The issuance of new Treasurys pushed up interest rates as the market struggled to absorb the new bonds. A further contributing factor to this dynamic is the Federal Reserve’s hawkish monetary policy. The Fed’s tapering of its bond holdings has reduced a key source of demand. Additionally, recent interest rate hikes have discouraged investors from holding long-term bonds as short-term bonds offer more attractive yields.

The metals market has also seen a transformation. So far this year, China’s modest industrial rebound has lifted copper prices from their 2023 lows, while the collective central bank buying of gold, spearheaded by China, has sent bullion prices skyrocketing. This unusual gold surge has offset the rise in copper prices, which explains why the ratio has been relatively subdued this year. While this trend may seem fleeting, evidence suggests emerging economies are accumulating gold as a potential hedge against the US government’s frequent use of sanctions tied to the dollar. As a result, it is possible that the copper/gold ratio could continue to move in the opposite direction of 10-year Treasury yields.

The breakdown in the relationship between the copper/gold ratio and 10-year Treasury yields likely stems from a new global economic reality. Higher deficits and inflation expectations have driven up long-term yields, while China’s slowdown and central bank gold purchases have suppressed the copper/gold ratio. A return to the prior correlation could occur if investors become confident in a return of price stability and if the accumulation of gold by foreign central banks proves temporary. However, we are doubtful of a near-term return, given persistent labor shortages, inflation pressures, and rising geopolitical tensions, particularly between the US and China.

Bi-Weekly Geopolitical Podcast – #48 “The Philippines, China & Escalation in the South China Sea” (Posted 6/3/24)

Bi-Weekly Geopolitical Report – The Philippines, China & Escalation in the South China Sea (June 3, 2024)

by Daniel Ortwerth, CFA | PDF

On the short list of seemingly constant topics in the news today is the rising tension between the United States and the People’s Republic of China. Across the spectrum of issues, disagreement between these two great powers seems increasingly unavoidable. Geopolitical developments in every corner of the globe often find a way to become another point of US-Chinese friction. When conditions become stormy like this, the question arises as to whether this tension will escalate into greater conflict, possibly even outright war. If it does, what will be the flashpoint? Where will the spark occur?

A storm is currently brewing in the South China Sea (SCS) that might make this body of water the area of greatest risk. Like so many conflicts in history, this one does not involve a direct conflict between the opposing great powers, but rather a local dispute involving a small but significant country, the Philippines, and China. This dispute holds the potential to stir up a storm that engulfs the region or that even spills into the world beyond it.

This report explains how the current Philippine-Chinese dispute developed and how it could further escalate. After providing a recent history of key developments in the SCS, we explain in detail the dispute at hand. Next, we show the strands that connect the tiny outcropping of land at the heart of the dispute to the broader world. As usual, we conclude with a review of implications for investors.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Business Cycle Report (May 30, 2024)

by Thomas Wash | PDF

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. The intention of this report is to keep our readers apprised of the potential for recession, updated on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

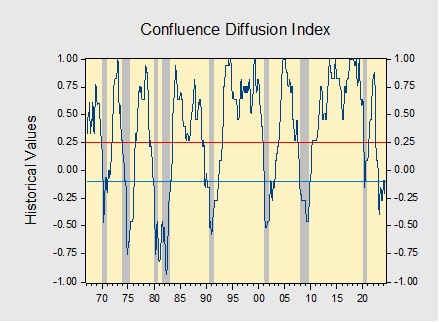

The Confluence Diffusion Index fell deeper into contraction, in a sign that the expansion is struggling to gain traction. The April report showed that seven out of 11 benchmarks are in contraction territory. Last month, the diffusion index slipped from -0.1515 to -0.2121, below the recovery signal of -0.1000.

- Financial conditions loosened as Fed officials kept rate cuts on the table for 2024.

- Goods-producing activity tapered as households grow more pessimistic about the economy.

- Employment gains slowed in a sign that the labor market is starting to cool.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is in recovery. The diffusion index currently provides about six months of lead time for a contraction and five months of lead time for recovery. Continue reading for an in-depth understanding of how the indicators are performing. At the end of the report, the Glossary of Charts describes each chart and its measures. In addition, a chart title listed in red indicates that the index is signaling recession.

Asset Allocation Bi-Weekly – #119 “The Importance of the Federal Reserve’s Inflation Target” (Posted 5/28/24)

Asset Allocation Bi-Weekly – The Importance of the Federal Reserve’s Inflation Target (May 28, 2024)

by the Asset Allocation Committee | PDF

Money has three characteristics: medium of exchange, store of value, and unit of account. When money is taught in undergraduate economics classes, these three functions are treated as self-evident, but careful observation suggests that that the first two characteristics are contradictory. If a monetary authority emphasizes the medium of exchange function, then it will tend to oversupply specie to the economy. If the store of value function is favored, then currency is restricted, which tends to support the value of money at the expense of consumption.

In practice, monetary authorities must balance these goals. However, these authorities don’t exercise policy in a vacuum. Instead, the dominating factor usually reflects the power structure of a nation. A society dominated by creditors and asset owners tends to favor the store of value function, whereas one dominated by debtors and consumers favors medium of exchange. Throughout history, monetary authorities have usually either adopted a gold standard, which tends to favor the store of value function, or a fiat standard, which means the currency’s value is set by the central bank’s control of the money supply. Throughout history, a fiat standard tends to favor the medium of exchange function.

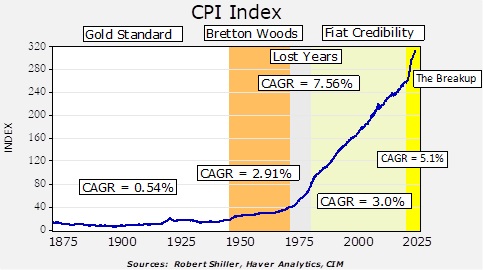

Price levels should reflect which factor the policymakers favor. This chart details the CPI index relative to historical monetary regimes.

Our data series begins in 1871. From the founding of the republic until 1944, the US was on a gold standard for the majority of the time. During wars, the gold standard was usually suspended, but the government tended to return to it once the conflict ended. The gold standard did come under pressure during the Great Depression as the dollar was devalued against gold and US private monetary gold holdings were declared illegal. Despite the erosion, the compound annual growth rate of CPI during this period was 0.54%, clearly low. The gold standard mostly favors capital owners and creditors; a key reason that political support for the gold standard began to erode in the 1920s was due to expanded suffrage. Debtors and the unpropertied that fought during WWI demanded a voice in government after the war ended. What made the gold standard work is that these classes bore the cost of austerity, but once they acquired political power, they were disinclined to accept the austerity demanded by the gold standard.

As WWII was winding down, the allies created a hybrid of the gold standard at Bretton Woods. Currencies were pegged to the dollar and the dollar was pegged to gold. As the chart above shows, it was not as effective as the gold standard in containing inflation, but it worked reasonably well. However, by the early 1970s, a precipitous drain of US gold reserves led President Nixon to suspend gold redemptions in 1971, leading to the “lost years” period on the above chart. Inflation soared.

To contain inflation and restore confidence in currencies under a fiat standard, Western central bankers gradually established two key rules: central bank independence and a clear inflation target. Over time, central banks were freed from their finance ministries, which gave them the power to conduct an independent monetary policy. Since the early 1980s, the central banks of industrialized nations have steadily been granted their independence from fiscal authorities.

The most widely adopted inflation target was 2%; this target was initially established by the Reserve Bank of New Zealand on an offhand comment to a television reporter rather than through careful study. Other central banks soon adopted the standard. Although the Federal Reserve didn’t officially adopt the standard until 2012, it was considered the de facto standard as early as 1996. As the chart above shows, the compound annual growth rate of US CPI over this period exceeded 2%. The general consensus, though, is that an inflation rate between 2% to 3% is low enough to where economic actors don’t factor inflation into consumption and investment decisions. And so, the combination of central bank independence and a clear inflation target has mostly been successful in supporting confidence in fiat currencies. International trade expanded under fiat credibility which suggests that there was general confidence in the dollar as the reserve currency and US Treasurys as the reserve asset.

On the above chart, we have added a fifth regime — The Breakup. Since the pandemic, the pace of inflation has clearly accelerated. Although central bank officials argued that the inflation issue was “transitory,” it has instead proven to be persistent. Central banks have raised interest rates but clearly not to the point where inflation has returned to the Fed’s target level.

There are two factors that we think are undermining the Fiat Credibility regime. First, there is a sentiment among some notable policymakers that the 2% target is too low. The fact that in the last decade central banks in some parts of the world lowered their policy rates below 0% and the FOMC engaged in zero interest rates plus balance sheet expansion is prima fascia evidence that the inflation target is too low. The basic idea is that a higher inflation target would give policymakers greater leeway to stimulate the economy without resorting to unorthodox monetary policy actions.

The second threat may be more formidable. Across the industrialized world, there are rising pressures on fiscal budgets. Aging populations are straining government retirement programs, and rising geopolitical tensions are leading to higher defense spending. In the US, the Congressional Budget Office is projecting high deficits for the rest of the decade.

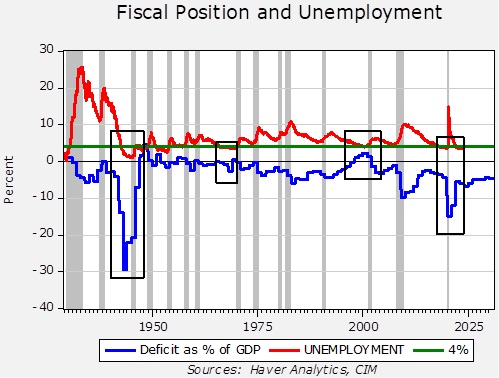

This chart shows the deficit as a percentage of GDP and the unemployment rate. We have inserted boxes around periods where the unemployment rate was at or below 4%. Note that in two periods when the unemployment was at this low level (the late 1960s and late 1990s), deficits tended to be low or, in the case of the latter event, the government ran a surplus. During the other two events (WWII and after the pandemic), the deficit widened while unemployment was low. Usually, a strong economy narrows the deficit as tax receipts rise and spending on welfare support programs declines.

What is concerning about the current situation is that despite low unemployment, the Congressional Budget Office is projecting that rather elevated deficits will be continuing. There is much criticism of this spending in the financial media, with some calling it “the largest deficit in peacetime.” We quibble with this comment, and we disagree about this being “peacetime.” In fact, if this is wartime, the deficits will likely be higher in the future. Defense spending coupled with social spending for retirees will strain budgets. In general, tax increases are politically difficult. At the same time, this cold war we are facing is already fracturing global trade, which will tend to increase structural inflation.

In the face of rising deficits, central bank independence is under threat. These deficits will need to be financed. To prevent sharp increases in interest rates, central banks may be forced to expand their balance sheets to absorb this debt in order to keep interest rates at manageable levels. Obviously, something has to give. We suspect what will “give” will be price levels. The unknown is how households and firms will react to what is essentially an increase in the inflation target. If inflation fears rise enough, economic actors will separate the medium of exchange function of money from the store of value function. If that occurs, some financial and real assets could replace the store of value function for economic actors. Our task, as asset managers, is to determine which assets will gain that function and invest accordingly.