by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with a discussion of how the United States is leveraging AI capabilities to keep key allies within its strategic orbit. We then turn to the Federal Reserve, outlining our views on its next policy direction. Next, we provide briefings on SpaceX’s rising valuation, newly released details of the US-Iran ceasefire agreement, and risks of a potential oil glut next year. As always, we include a review of recent domestic and international economic data.

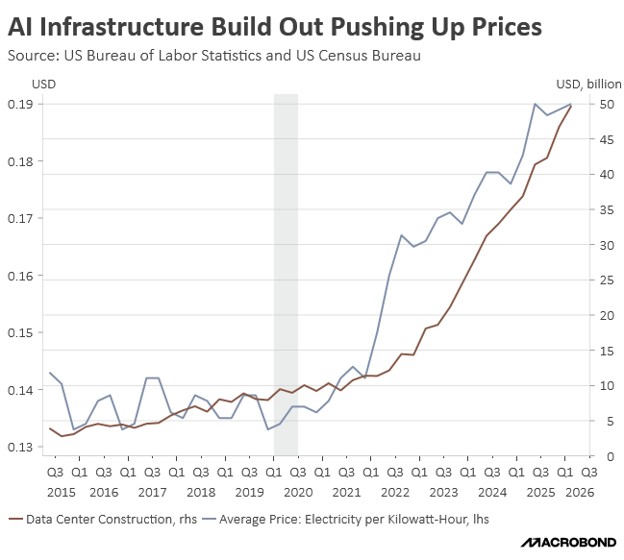

AI Foreign Policy: The United States is increasingly turning to artificial intelligence as a tool to reshape its foreign policy. Just one week after the White House prohibited foreign nationals, including those working within the US, from using the Anthropic tools Mythos and Fable 5, Washington has initiated talks with European partners regarding access to American-made AI tools. These discussions reflect the US’s growing willingness to leverage its technological edge as an instrument of geopolitical influence.

- During the G7 Summit, the United States discussed a “trusted partner” scheme that would grant close allies privileged access to the latest AI models. The scheme could mean that AI providers would be restricted from selling their products to certain countries — or, in some cases, specific companies. A broad agreement may allow participating nations to leverage these advanced technologies in order to assist in the ramping up of their defenses against rivals such as China.

- The decision reflects growing US concern over the capabilities of Anthropic’s latest models. Last week, Commerce Secretary Howard Lutnick warned that the company may require special export licenses to provide certain tools to foreign nationals, citing national security risks. While the White House has not formally explained the directive, it is widely believed to be linked to the discovery of a jailbreak in Fable 5 that could circumvent Anthropic’s safety guardrails.

- The move to restrict AI exports mirrors the semiconductor controls that expanded from 2022 to 2024, which sharply limited advanced chip sales to China and other “countries of concern.” In both domains, Washington aims to guarantee allies’ access to US technology while constraining rivals, underscoring how protective it has become of its technological edge and how it is using that edge to keep key states within its strategic orbit.

- The government push to limit advanced AI-model use by foreign nationals is likely to weigh on the earnings of major technology firms, which are more dependent than most sectors on international revenue. These restrictions also highlight the risk that tech valuations may be elevated relative to rising policy and regulatory headwinds. We continue to advocate sector diversification as a way to hedge against over‑concentration, given the growing dominance of large technology companies within equity indexes.

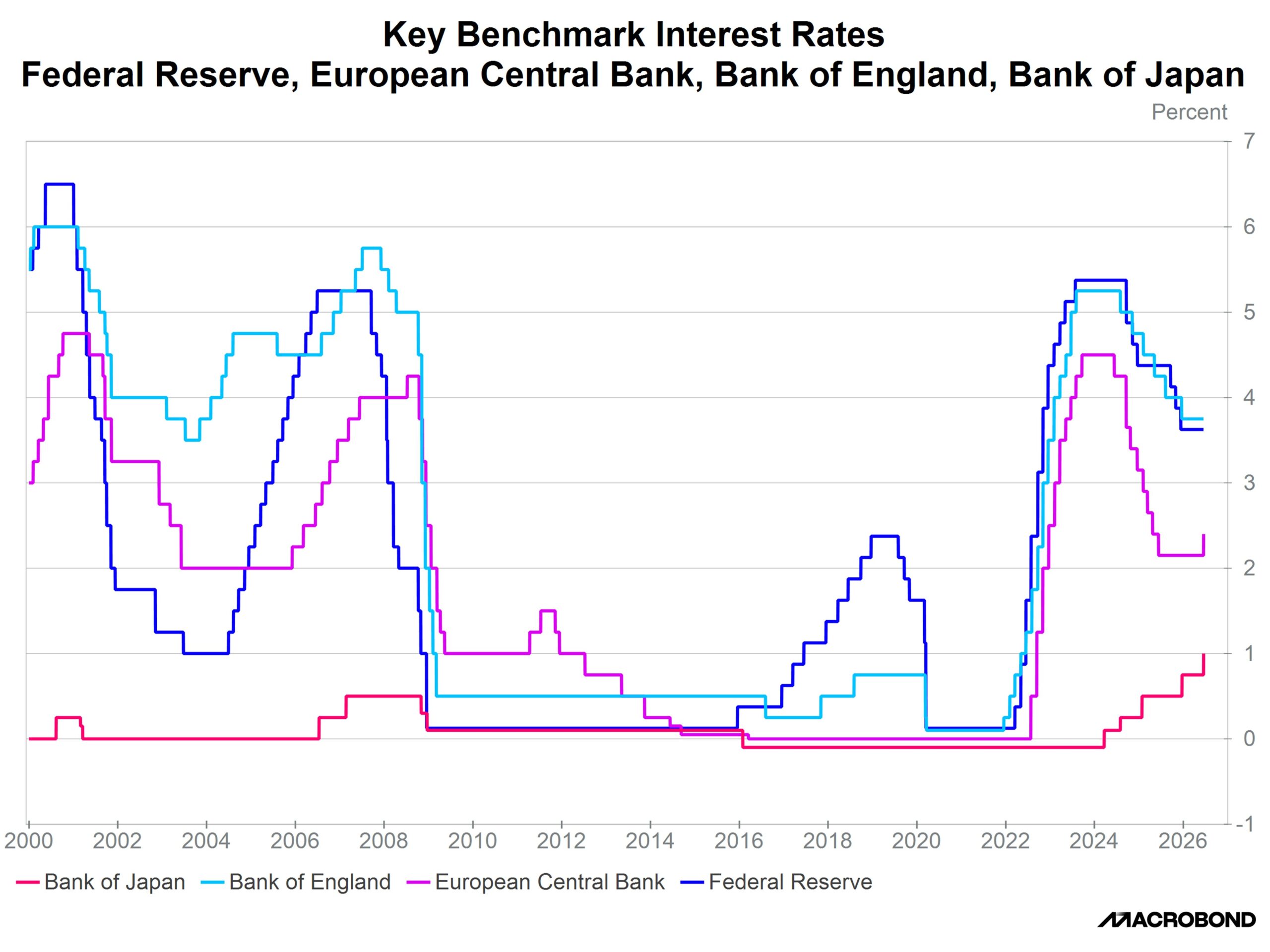

Warsh Takes the Lead: All eyes will be on Fed Chair Kevin Warsh this afternoon as he presides over his first meeting since taking office. Markets will be focused on how the central bank assesses the inflation outlook, particularly in light of recent progress toward de-escalation in Iran. While easing geopolitical tensions should help improve the near-term inflation outlook, uncertainty around the policy path remains elevated amid persistent signs of underlying price pressures.

- Warsh inherits a more hawkish Federal Reserve than his predecessor. Ahead of today’s meeting, several Fed officials have signaled that further rate hikes may be warranted if inflation remains above the 2% target, citing not only pressures from the Iran conflict but also demand strength from the AI boom and a firming labor market. The departure of a noted dove, Governor Stephen Miran, further removes a key counterweight to tightening.

- Further reinforcing the hawkish bias are recent moves by peer central banks. Despite the agreement between Iran and the US to reopen the strait, policymakers elsewhere remain cautious about declaring victory on inflation. The Bank of Japan raised rates on Tuesday, citing ongoing inflation concerns, while ECB Chief Economist Philip Lane signaled that additional tightening remains possible following this month’s hike.

- Markets will be paying very close attention to Warsh as he offers his views on the direction of Fed policy. Over the past several years, the dollar has grown increasingly sensitive to shifts in interest rate differentials, as investors have come to view central banks with relatively dovish stances less favorably against a backdrop of persistently elevated inflation. Against that environment, any hawkish tilt from the Fed could lay the groundwork for another sustained dollar bull market.

- Heading into his first meeting, we expect Warsh to signal that the Fed will stay the course while keeping its options open. Such a stance would leave room for potential rate cuts later this year, which could act as a headwind for the dollar. That said, any shift toward a more hawkish tone could prompt a reassessment of current equity valuations while simultaneously supporting the dollar.

SpaceX’s Rise: The Musk-owned company’s stock is off to a strong start, having just surpassed Amazon’s valuation to become the fifth-largest firm by market capitalization. The sharp move reflects robust post-IPO demand, but much of the recent upside also appears tied to a broader relief rally following progress in Iran-US talks. The rise of SpaceX reflects the growing dominance of tech companies in the S&P 500.

Iran Deal: There remains significant debate surrounding the reported agreement between Iran and the United States to reopen the Strait of Hormuz later this week. While the official framework has been released, subsequent leaks suggested the possibility of a $300 billion investment fund tied to Iran’s compliance with the terms of the deal. The White House has denied any direct US involvement in such a mechanism, but the emergence of these reports underscores the intensifying political pressure and scrutiny surrounding the agreement.

Oil Glut? The International Energy Agency warns that the Middle East agreement could set the stage for oil overproduction during the next few years. Although it does not expect exports to rebound immediately once the conflict ends, it anticipates that as shut‑in capacity and war‑affected facilities gradually return to operation, global output could rise sharply, creating a substantial supply overhang by next year. This prospective increase in production is likely to exert downward pressure on oil prices and related inflation measures in the coming months.