Author: Amanda Ahne

Bi-Weekly Geopolitical Report – Goodbye Prigozhin (September 18, 2023)

Bill O’Grady | PDF

On August 23, an executive jet carrying seven passengers and three crew members crashed near Moscow on a flight to St. Petersburg. Yevgeny Prigozhin, the head of the Wagner Group, a private Russian military company, was reportedly one of the passengers. Prigozhin was having an eventful summer. He had led an apparent mutiny in June, but called off his march on Moscow despite making significant progress toward the capitol after seeming to make a deal with Russian President Putin, and thereafter was seen conducting Wagner business again.

In this report, we will examine four issues. First, is he really dead? Second, if he is dead, who did it and how did they do it? Third, we will discuss the benefits and costs of the Wagner Group to the Russian state. And fourth, we will analyze the potential benefits and costs of his apparent assassination. As always, we will conclude with market ramifications.

Don’t miss our other accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify | Google

Weekly Energy Update (September 14, 2023)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA | PDF

Oil prices have continued their rise, with WTI trending towards $90 per barrel.

(Source: Barchart.com)

(Source: Barchart.com)

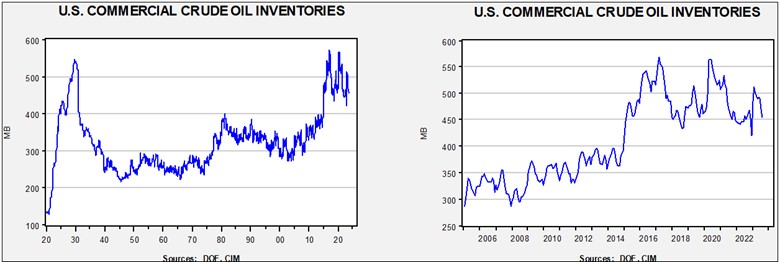

Commercial crude oil inventories rose 4.0 mb, compared to forecasts of a 2.0 mb draw. The SPR rose 0.3 mb which puts the net build at 4.2 mb (the discrepancy is due to rounding).

In the details, U.S. crude oil production rose 0.1 mbpd to 12.9 mbpd. Exports declined 1.8 mbpd, while imports rose 0.8 mbpd. Refining activity rose 0.6% to 93.7% of capacity.

(Sources: DOE, CIM)

(Sources: DOE, CIM)

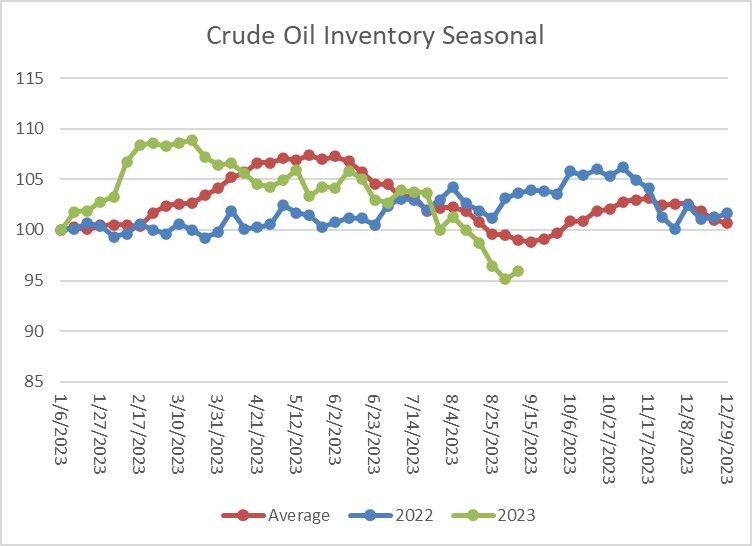

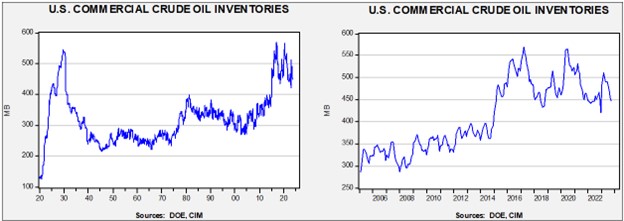

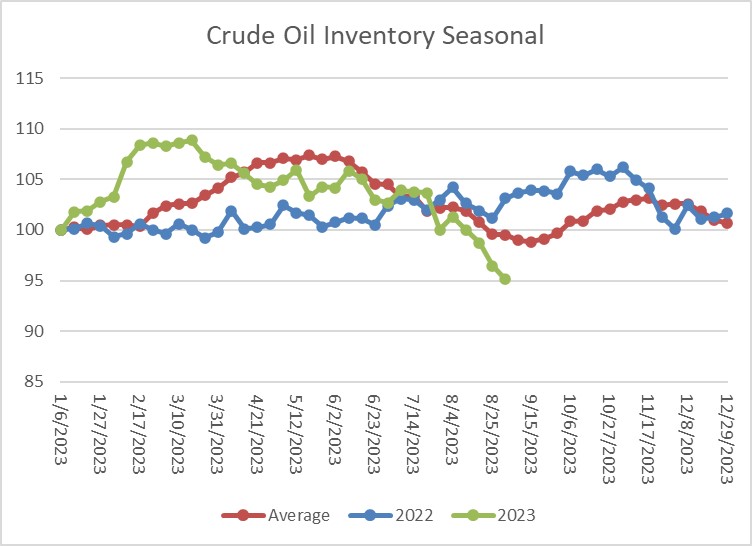

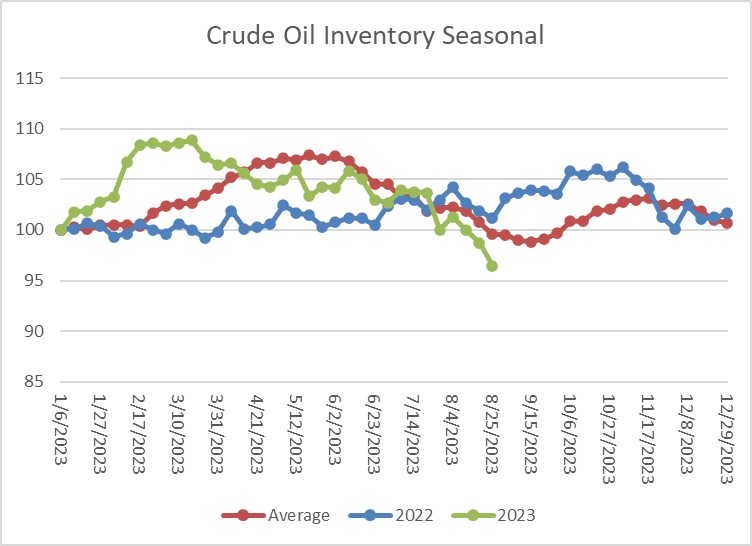

The above chart shows the seasonal pattern for crude oil inventories. Last week’s rise is mostly consistent with expected seasonal increases in crude oil stockpiles. However, the sharp drop in exports is a bit of a puzzle and if reversed next week, inventories could remain tight.

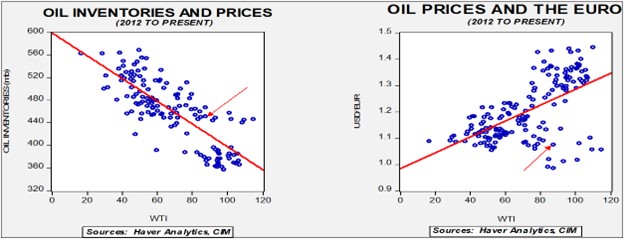

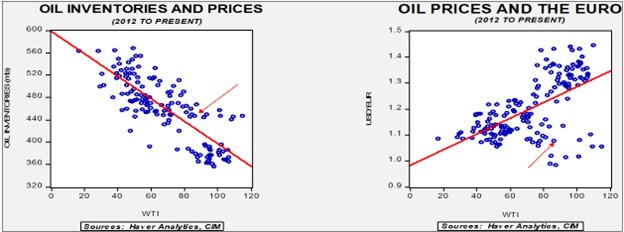

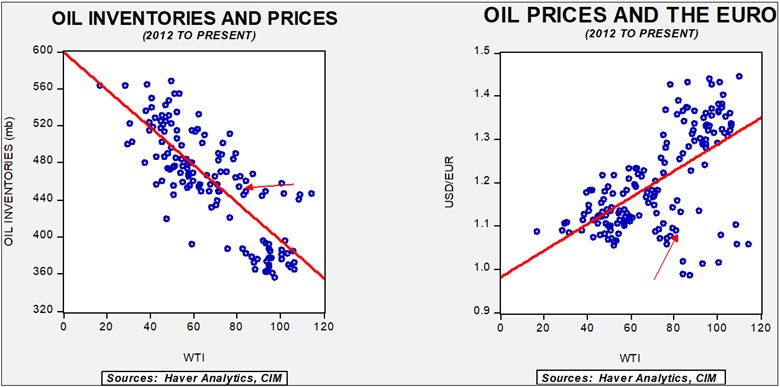

Fair value, using commercial inventories and the EUR for independent variables, yields a price of $73.30. Commercial inventory levels are a bearish factor for oil prices, but with the unprecedented withdrawal of SPR oil, we think that the total-stocks number is more relevant.

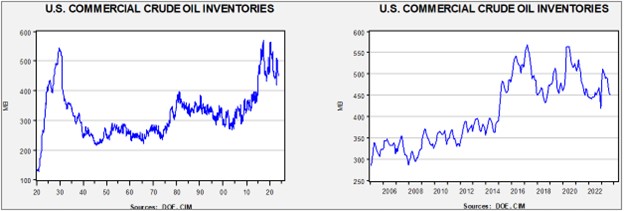

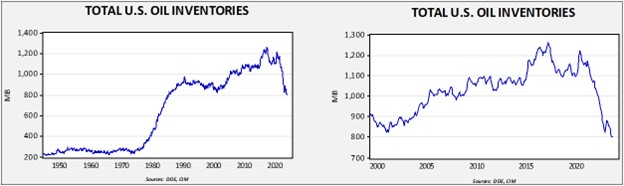

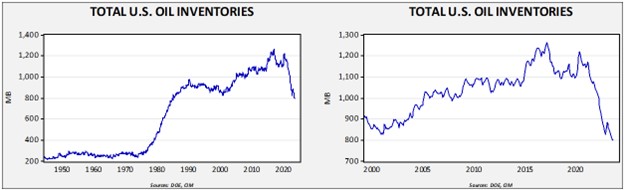

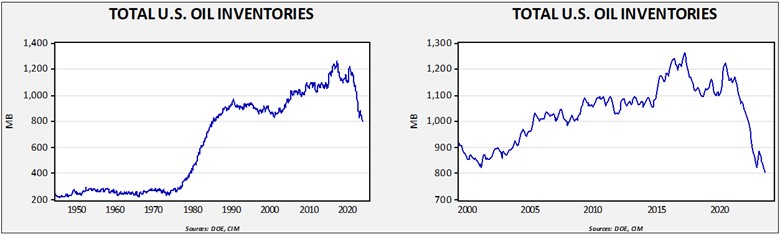

Since the SPR is being used, to some extent, as a buffer stock, we have constructed oil inventory charts incorporating both the SPR and commercial inventories.

Total stockpiles peaked in 2017 and are now at levels last seen in late 1985. Using total stocks since 2015, fair value is $94.95.

Market News:

- The executive director of the IEA issued an editorial in the Financial Times where he forecast peak oil and natural gas demand would occur by the end of the decade. The increase in EVs and renewables is expected to supplant fossil fuels. Obviously, we won’t know for sure if he is correct for a few years, but this position does affect behavior. Oil and gas firms have already shifted their focus from growth to providing return to shareholders and owners. After all, how does one justify expanding production that may simply be stranded? On the other hand, if he is wrong, and demand continues to grow, the behavior of firms increases the likelihood of much higher oil prices.

- Russian refineries are planning seasonal maintenance that will allow for more oil exports but will also curtail product exports. It will be interesting to see if Russia maintains its promise to restrict oil supplies in light of this seasonal situation.

- Although the Kingdom of Saudi Arabia’s (KSA) production restrictions have supported oil prices recently, it will almost certainly weaken the economy. That’s in part due to increasing Iranian exports and rising Guyana production that will reduce the KSA’s market share. We don’t expect a change in Saudi production this year, but we wouldn’t be surprised to see an attempt to regain market share next year.

- U.S. shale producers are trying to impress investors with their improved efficiency. In the past, it was all about production, but now there is a focus on profitability. One measure of efficiency is the length of drilling laterals; in other words, getting more oil from each wellhead.

- As the odds of an Australian LNG strike loom, Chevron (CVX, $165.59) is likely to deploy a legal strategy to avert a work stoppage. Workers have already went on strike to signal their resolve. There is an element of Australian law that suggests that if two sides in a labor dispute are hopelessly deadlocked, one side can petition for arbitration and work continues. It is apparently untested, and we would be surprised if the courts give Chevron an out.

- EU natural gas prices jumped on strike news.

Geopolitical News:

- As we have noted recently, the U.S. and Iran are taking steps to improve relations. For example, frozen Iranian financial accounts held in South Korea have been allowed to be sent to Tehran in exchange for prisoners. The prisoner swap has been officially approved this week. However, that isn’t keeping U.S. officials from seizing Iranian oil that violates American sanctions. We note that the owner of a ship holding Iranian oil has admitted he broke sanctions in court.

- If Saudi/Iranian relations continue to improve, is there a chance that the KSA will soften its stance on Hezbollah? And will that affect the potential for an Israeli/KSA normalization?

- There is a political cost to this deal. Iran is generally unpopular and doing anything that smacks of appeasement raises concerns.

- Despite reports that Iran is slowing down its nuclear enrichment activities, the IAEA continues to report that Iran has expanded its stock of near-weapons grade uranium.

- One sign that the markets believe there will be a thaw with Venezuela is that it’s long moribund bond market is rallying.

- There are Iranian Kurdish groups opposed to the government in Iran that have taken refuge in Iraq. A recent agreement between Tehran and Baghdad calls for Iraqi officials to disarm these groups. It is unclear if Iraq will actually follow through on this promise, as it might trigger an armed response from Iraqi Kurds. Although the Kurds are themselves divided, being attacked by an outside force might just unify the Kurds in the face of a common enemy.

- Although Russian oil sales to Europe have been curtailed, they are not eliminated. Small EU nations tend to be buyers still. The Czech Republic is increasing its purchases of Russian oil, for example.

Alternative Energy/Policy News:

- MIT has announced a new carbon capture technology using an electro-chemical process that uses less energy. Current methods tend to require high levels of energy and if this energy comes from fossil fuels, the gains are mostly cosmetic.

- Amazon (AMZN, $141.58) is making a major investment in direct carbon capture. We are seeing a trend in large companies backing this technology.

- Geothermal energy is poised for aggressive development. This form of energy is clean and mostly non-controversial. The problem has always been that there are limited areas where such energy can be economically exploited. However, new methods of extracting this power are being developed which, if successful, will lower costs and make the power more widely available.

- The U.S. and the KSA are in talks to secure and develop EV metals in Africa. This unusual partnership is being fostered by fears that China will extend its dominance over these metals.

- Malaysia is set to ban the exports of rare earths, demanding that firms build processing facilities in country for the finished product.

- Not only are cars going electric, but large trucks are too, although progress has been much slower due to the weight of batteries. Elon Musk is looking at building out a massive recharging network for such vehicles but wants public sector support.

- China’s dominance in photovoltaic (PV) is leading to lower prices for solar panels, essentially undercutting producers in the U.S. and Europe. EU producers are warning that they will be facing bankruptcy without state support, either from tariffs or subsidies.

- In the U.S., support for the PV industry as part of the Inflation Reduction Act hasn’t yet translated into manufacturing, but it is expected to expand solar power in the U.S.

- The annual U.K. wind auction failed to gather any winning bids this week. Rising costs for building facilities is said to be the culprit.

- The EU is just a couple of weeks away from implementing its carbon border taxes. Companies in Europe are scrambling to adjust to higher priced imports.

- As China exports low cost EVs to Europe, the EU announced it will investigate the role of Chinese government subsidies in this surge. Such studies are usually a precursor to dumping tariffs.

Asset Allocation Bi-Weekly – #105 “Fiscal Tightening Looms” (Posted 9/11/23)

Asset Allocation Bi-Weekly – Fiscal Tightening Looms (September 11, 2023)

by the Asset Allocation Committee | PDF

To understand the state of the U.S. economy and gauge near-term financial prospects, investors over the last couple of years have focused on issues like the Federal Reserve’s monetary policy, consumer price inflation, labor market indicators, and retail sales. They seemed to pay much less attention to fiscal policy, except perhaps amid this spring’s Congressional standoff over the federal debt limit. Our recent work suggests fiscal policy could become a much more important focus in the coming months. In part, that’s because of the potential for a stalemate in Congress over the budget for the new fiscal year starting October 1. More generally, it’s also because of the fast-growing budget deficit and looming changes in the government’s income and outlays.

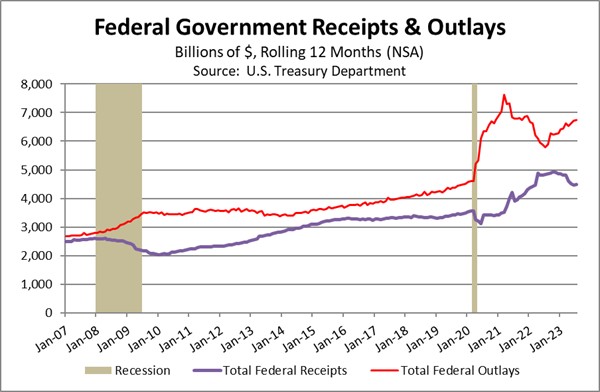

To start out, let’s look at the broad contours of today’s federal budget situation. In the 12 months ended in July, federal receipts totaled $4.480 trillion, but outlays rose to $6.743 trillion. The deficit stood at $2.263 trillion. That shortfall was nowhere near the enormous deficits at the height of the coronavirus pandemic, but it was still much worse than in the prior 12 months. As shown in the chart below, the expansion in the deficit over the last year reflected both declining receipts and rising outlays.

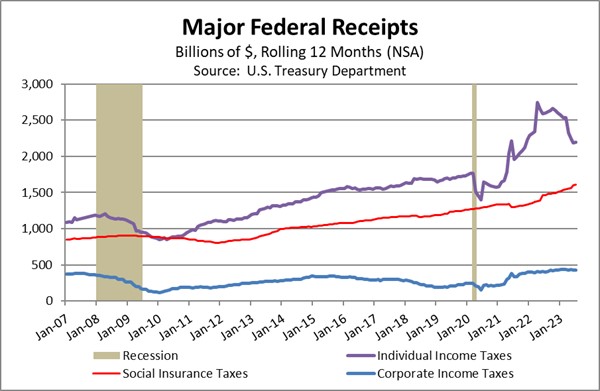

To understand what’s going on here, let’s first dive deeper into federal revenues. During the year ended in July 2023, they were down $352.4 billion from the year ended in July 2022, for a decline of 7.3%. Our analysis shows the decline can be explained entirely by a $408.3-billion drop in individual income taxes, most likely because of lower capital gains taxes after the stock market’s long slide last year, lower wage income as more Baby Boomers and other workers dropped out of the labor force, and an upward adjustment to federal tax brackets because of the price inflation in 2022. The drop in individual income taxes was partially offset by a modest rise in other receipts, such as Social Security taxes, Medicare taxes, corporate income taxes, and customs duties.

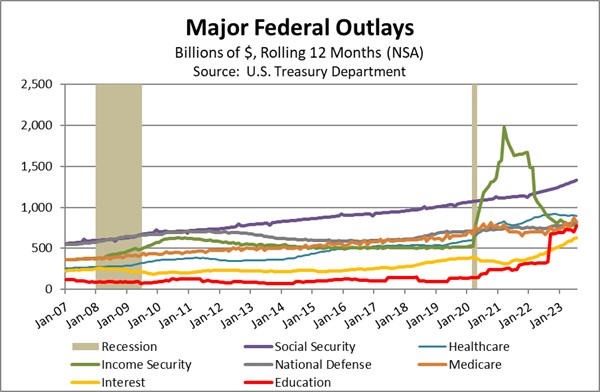

The bigger change came on the spending side of the ledger. In the year ended July, federal outlays were a whopping $951.8 billion more than in the preceding year, for a rise of 16.4%. A couple of major outlays fell. For example, Income Security and Healthcare spending declined modestly. On the other hand, several big spending types grew sharply. Because of population aging, a boom in new retirees, and a big cost-of-living increase in Social Security benefits, outlays for Social Security and Medicare grew by a collective $279.6 billion. In addition, interest outlays were up $182.9 billion from the prior 12 months as outstanding debt grew and interest rates rose. Most dramatic of all, education outlays ballooned by $453.2 billion compared with the previous 12 months, mostly reflecting the pandemic-era moratorium on student loan repayments and interest. That moratorium was declared back in March 2020, but final costs of $449.3 billion were recognized only in September 2022, making it look like there was a sudden, temporary spike in education expenditures during that one month (see chart below).

The spike in recognized education expenditures may drop out of the 12-month rolling average beginning with the Treasury report for September 2023, which could then show a drop in spending. More broadly, as the student loan pause and other big pandemic relief programs come to an end in the coming months, the drop in overall fiscal stimulus could have a noticeable negative impact on demand. Not only will college graduates lose their student loan subsidies and have to start paying principal and interest again, but daycare centers will lose their operating subsidies, prompting some to close and forcing many, mostly women, out of the workforce. Of course, the administration’s big, new programs to subsidize infrastructure rebuilding and factory construction will soon begin to pump more money into the economy, but that probably won’t offset all the expiring pandemic outlays.

Without substantial growth in fiscal stimulus in the coming year, a major pillar that has prevented the economy from entering recession will be removed. Although the tight labor markets from the loss of Baby Boomers and the consequent higher incomes remain as does rising interest income, the drop in fiscal stimulus raises the odds of a downturn in the coming quarters. Thus, investors need to remain vigilant about a recession, even though the current consensus is calling for continued growth.

Weekly Energy Update (September 8, 2023)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA | PDF

Oil prices have clearly broken out of their trading range, with Brent crude oil moving above $90 per barrel. Prices are being supported by the Russian and Saudi extension of production restraint.

(Source: Barchart.com)

(Source: Barchart.com)

Commercial crude oil inventories fell 6.3 mb, much lower than the 1.8 mb draw forecast. The SPR rose 0.8 mb which puts the net draw at 5.5 mb.

In the details, U.S. crude oil production was steady at 12.8 mbpd. Exports rose 0.4 mbpd, while imports rose 0.2 mbpd. Refining activity fell 0.2% to 93.1% of capacity.

(Sources: DOE, CIM)

(Sources: DOE, CIM)

The above chart shows the seasonal pattern for crude oil inventories. Last week, the continued decline in inventories put stocks well below seasonal norms. We are nearing the seasonal trough, and if stockpiles continue to decline, it would be a bullish factor for oil prices.

Fair value, using commercial inventories and the EUR for independent variables, yields a price of $74.53. Commercial inventory levels are a bearish factor for oil prices, but with the unprecedented withdrawal of SPR oil, we think that the total-stocks number is more relevant.

Since the SPR is being used, to some extent, as a buffer stock, we have constructed oil inventory charts incorporating both the SPR and commercial inventories.

Total stockpiles peaked in 2017 and are now at levels last seen in late 1985. Using total stocks since 2015, fair value is $95.32.

Market News:

- The Kingdom of Saudi Arabia (KSA) and Russia announced that they will keep their production restrictions in place until the end of the year. This news boosted oil prices and the restrictions should buoy prices. Falling KSA production is leading to a decline in Saudi oil exports. As these producers constrain output, there is some evidence that Iran is taking market share. The U.S. is likely facilitating Iranian oil flows.

- Rising oil prices are a danger to the global economy. China itself is at risk.

- The Biden administration has rescinded some Alaskan drilling permits issued during the Trump administration. However, the Willow project remains in place. The administration is continually trying to weave a path between supporting the economy through lower oil prices and placating the environmental wing of the Democratic party. For the most part, Biden is managing to disappoint both goals. Although the decision was welcomed by environmentalists and panned by the fossil fuel industry, in reality, the White House is not going full bore toward either side. This decision details the difficulty of being in power. There are costs to engaging in a policy and sometimes those costs make a president unpopular.

- It should be noted that oil companies are were not rushing to expand the projects in Alaska.

- A new DOE report shows the LNG market is broadening. As this market broadens, it’s a supportive factor for U.S. natural gas producers. This broadening is also helping Russian gas producers as well. While EU piped gas imports have plummeted, Europe is importing record volumes of Russian LNG. EU leaders have taken notice of these imports and argue that they should be curtailed.

- Brazil’s oil and gas production hit a new record in July.

- Guyana is currently producing 0.4 mbpd, but by 2028, it is expected to be producing 1.2 mbpd, making the country an increasingly important supplier to the oil market.

- Canada is near completion of its Trans-Mountain pipeline. Once open, it will shift Canadian oil flows to the Pacific, increasing oil exports to the Far East, and reducing Canadian flows into the U.S. We would expect the Canadian/U.S. differentials to narrow compared to their history.

- For reasons that are not exactly clear, the difference in electricity consumption between the weekends and weekdays is steadily falling. Most of the time, electricity consumption during the week had been higher than the weekends. However, in recent years, the difference has been shrinking. The most likely reason is probably coming from the industrial sector. It’s possible that industrial firms are running full out and, thus, don’t slow down on the weekends, or industrial firms have become more energy efficient, narrowing the difference. In any case, if this pattern continues, it will make it easier to manage the grid. Energy firms have to maintain capacity to meet peak demand. If that peak declines (essentially smoothing out demand), utilities should then need lower peak capacity.

Geopolitical News:

- We have documented the U.S. efforts to see the KSA and Israel normalize their relations. Key participants to this goal are the Palestinians. The Palestinians are formulating their demands to support normalization, but what is unclear is just how concerned Riyadh is about meeting those demands. Although such a deal would be a blockbuster, there are numerous impediments to getting a deal done.

- Brett McGurk, a senior administration Middle East advisor, is traveling to Riyadh this week to meet with KSA and Palestinian representatives.

- Beijing and Riyadh are steadily improving relations. The Bank of China (BACHF, $0.35) has opened its first branch in the kingdom providing evidence of deeper financial cooperation. Creating banking relationships will facilitate trade in local currencies.

- Russia is facing internal fuel shortages that appear to be worsening. There is concern that the lack of fuel could adversely affect the grain harvest.

- The U.S Navy has indicated it intends to keep warships around the Strait of Hormuz to address Iranian attacks. The IRGC has seized a ship it claims was carrying smuggled fuel.

- The G-7 is quietly shelving the Russian oil price cap; as prices have increased, there is less incentive to curtail Russian supplies.

- Although Iran has expanded its inventory of near-weapons grade uranium, there are some hints it is slowing its stockpile accumulation, perhaps as a confidence-building At the same time, the U.N. watchdog IAEA is still not able to fully monitor Iran’s nuclear program.

- Iran is holding an EU official from Sweden. Johan Floderus has been in captivity for over a year.

- Swedish oil executives are on trial for war crimes due to their drilling activity in South Sudan. The executives are accused of aiding government and paramilitary groups who engaged in war crimes to secure areas for drilling activities.

Alternative Energy/Policy News:

- The Danish wind energy firm Ørsted (DNNGY, $21.17) warned that supply chain issues and complications surrounding tax credits hurt earnings. Shares of the company fell sharply on the news. Wind energy has been hitting some snags recently for a myriad of reasons.

- Four metals are critical to the energy transition: lithium, nickel, copper, and cobalt. Chile dominates copper and lithium reserves, the Congo holds the majority of cobalt reserves, and nickel resides in Australia and Indonesia.

- The KSA is investing heavily in the U.S. lithium battery industry.

- Due to the probable lack of supplies of these metals to meet anticipated demand, the importance of recycling is increasing.

- Although controversial, nuclear power remains the most stable carbon-free electricity source. China, with 21 reactors under construction, is moving to dominate this industry.

- As EV production grows in the U.S., much of the build-out is occurring in the rural South, offering both opportunities and disruption to local communities.

- China’s EV industry is rapidly expanding and is increasingly becoming a growth engine for the economy. China’s EV industry is threatening European and U.S. automakers. We suspect that the EU producers will accommodate China, whereas the U.S. will protect American automakers.

- China’s aggressive expansion of battery production is raising fears it is creating a supply glut that could depress prices.

- Chinese EV battery producers are focusing on Hungary for battery production in Europe. The government is considered more friendly to Beijing and has offered subsidies.

- Range is one of the most important issues for the transition from internal combustion engines to EVs. Since batteries take longer to charge and charging stations are not as readily available as gasoline stations, drivers deciding on which to buy are concerned about this issue. Car makers are working to develop solid state batteries that could charge much faster, but perhaps more importantly, could have ranges of up to 1000 miles.

- China has a dominant position in solar panels, but since the Chinese economy is driven more by government goals rather than profitability, the industry continues to invest even in the face of weaker prices.

- Russia continues to benefit by exporting nuclear fuel to the world’s nuclear power industry. Weaning off of Russian supplies will take years, although as we noted in recent reports, the U.S. is starting the process.

- Geoengineering is a controversial method of addressing carbon reduction and temperature control. The oceans remove carbon from the atmosphere, and there are efforts underway to enhance the ocean’s capacity to absorb carbon. There are numerous other carbon capture projects underway as well. Corporate America seems to be getting behind these efforts.

- Governments are expanding their investment into fusion power.

Weekly Energy Update (August 31, 2023)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA | PDF

Oil prices were mostly rangebound this week, holding near recent highs. We are watching Hurricane Idalia as it travels through the Gulf of Mexico. Its current track suggests it will miss the most sensitive areas of oil and gas production, but it could disrupt oil and gas shipping for a few days.

(Source: Barchart.com)

(Source: Barchart.com)

Commercial crude oil inventories fell 10.6 mb, much lower than the 2.2 mb draw forecast. The SPR rose 0.6 mb which puts the net draw at 10.0 mb.

In the details, U.S. crude oil production was steady at 12.8 mbpd. Exports rose 2.2 mbpd, while imports rose 0.5 mbpd. Refining activity fell 1.2% to 93.3% of capacity.

(Sources: DOE, CIM)

(Sources: DOE, CIM)

The above chart shows the seasonal pattern for crude oil inventories. Last week, the sharp drop in inventories put stocks well below seasonal norms. We would expect inventories to continue to decline into mid-September and then start their seasonal rise into November.

Fair value, using commercial inventories and the EUR for independent variables, yields a price of $71.86. Commercial inventory levels are a bearish factor for oil prices, but with the unprecedented withdrawal of SPR oil, we think that the total-stocks number is more relevant.

Since the SPR is being used, to some extent, as a buffer stock, we have constructed oil inventory charts incorporating both the SPR and commercial inventories.

Total stockpiles peaked in 2017 and are now at levels last seen in late 1985. Using total stocks since 2015, fair value is $95.49.

Market News:

- Although it is commonly held that oil demand will peak sometime over the next 20 years, there are skeptics who argue that this is unlikely. One reason is that developing economies will likely see more intensive energy consumption which will keep oil demand growing. The problem with the more commonly held view is that it affects investment. As we noted last week, for the first time ever, U.S. oil firms returned more cash to shareholders than they spent on exploration. This sort of activity makes sense if the future of oil and natural gas is bleak; however, if that is not the case, we could be dangerously underproducing oil which would lead to higher prices.

- Low water levels in the Panama Canal are forcing delays and light loadings of vessels. The problem could constrain LNG shipping to Europe.

- The Kingdom of Saudi Arabia (KSA) is expected to roll over its current cuts into October.

- During the pandemic, oil prices briefly “went negative.” Essentially, there was a lack of storage space for crude oil and those trying to sell it were forced to pay traders to take it. One of the contributing factors to the situation was selling from the oil ETFs. As investors moved to sell the ETFs, the managers of the funds, which held nearby oil futures contracts, were also forced to “dump” contracts. The forced selling created the downdraft in prices, leading to the unprecedented negative oil price. In response, the largest ETF from the United States Oil Fund (USO, $72.78) changed its investing pattern. Instead of holding the nearby futures, it spread its holdings among numerous contract months. Although this action dampened the impact on the front month, it also made the ETF less sensitive to nearby prices. Thus, investors wanting exposure to nearby oil prices found the product less attractive. We note that the fund manager has decided to return to holding the nearby futures again. Although this decision will make the product more attractive, it also will recreate the problem that led to the May 2020 price collapse.

- Although it is rarely discussed in polite company, there is an undercurrent of assigning costs of regulation. This is the reason lobbying exists. It is well known that the global shipping industry is “dirty,” as it has historically used bunker fuel, the dirtiest but cheapest cut of the crude oil barrel, but because of its international situation, it tends to be hard to regulate. As new global regulations are put into place, there is a battle on how (or better yet, to whom) the costs of regulation will be allocated.

- We have noted recently that U.S. oil production is rising. Interestingly enough, so is Canada’s.

- Although U.S. oil production is rising, drilling activity in the Permian Basin is declining rapidly. However, we may see this trend reverse in the coming months.

- The U.S.’s third largest oil refinery has been shut down due to a storage tank fire. The news lifted diesel fuel prices.

- Another area seeing expanding oil production is in Suriname.

Geopolitical News:

- We have not commented in detail on the Robert Malley situation. To recap, Malley was a special envoy to Iran who was recently relieved of his security clearance (and put on unpaid leave). Officially, the concern is his handling of sensitive documents, but the real issue is that he may have been an Iranian mole in the State Department. Although the mainstream U.S. media has mostly ignored the issue, it has been examined in great detail by John Schindler on Substack. Interestingly enough, the Iranian media is reporting on the topic and has disclosed internal State Department documents. It is unlikely that this situation will directly affect the oil and gas markets; however, it may disrupt administration negotiations with Iran and thus could lead to a drop in Iranian oil supplies.

- There was an apparent coup in Gabon, which is a member of OPEC+. President Bongo had just won a third term, but apparently elements of the military opposed his continued rule. Gabon is a relatively small producer (0.2 mbpd), so we don’t expect this event to have much impact on oil prices.

- Turkey and Iraq are in a dispute over who will pay the $1.5 billion fine incurred by the Kurdish Regional Government. Until the fine is paid, Turkey is blocking Iraqi oil exports from Northern Iraq.

- Iran has lived under some element of U.S. sanctions since 1979. The goal of sanctions is to change the sanctioned nation’s behavior. With Iran, for the most part, it seems this really hasn’t worked. It is clear sanctions have hurt Iran’s economy and its people, but Iran continues to act contrary to U.S. goals and persists despite the sanctions. A new paper suggests that a major reason for this is that Iranian elites actually benefit from sanctions. Essentially, Iranian elites shift the burden of sanctions onto ordinary Iranians and thus are willing to accept the sanctions regime.

- As the U.S. increases pressure on Russia, Washington is easing sanctions on Venezuela. The Biden administration doesn’t want high oil prices; it just wants to undermine Moscow.

- Although Iraq has ample natural gas reserves, it lacks processing capacity. Raw natural gas often contains liquids (which are quite valuable) and impurities that need to be refined for use in power plants, chemical processes, etc. Because Iraq lacks processing capacity, it has been forced to import “dry” natural gas from abroad. Turkmenistan and Iraq have announced a new trade deal for natural gas to feed Iraq’s electricity production.

- The KSA wants to build nuclear power stations. By doing so, it can free up more oil and natural gas for export. The U.S. and China are competing to provide the reactors, but Washington faces an impediment. The U.S. wants to build reactors that won’t create materials that could be used in nuclear weapons, while Beijing does not have similar requirements. Thus, the U.S. could find itself in a situation where it either doesn’t enforce its non-proliferation standards to get the business (which would probably be done by South Korea) or hold to the standards and see China build the reactors. In either case, the program could give Saudi Arabia the materials needed to build a nuclear weapon. We also note that Riyadh is using the nuclear issue as part of the U.S. goal of normalizing relations between Israel and the KSA.

- Saudi foreign reserves fell last month despite high oil prices. This drop reflects production cuts. Generally speaking, higher oil prices have tended to lift reserves, so the cuts are having an impact.

Alternative Energy/Policy News:

- Fossil fuels receive subsidies. It is common in emerging market economies for governments to subsidize fuels to households, for example. The IMF calculates these subsidies exceeded $7.0 trillion last year.

- As we have been noting on a regular basis, China is dominating the EV battery market. Not only is China becoming the low-cost producer, but it is also developing new battery technologies that could extend range and use cheaper, more abundant materials. For the West, the continued dilemma is whether to simply accept Chinese dominance to accelerate the energy transition or exclude China and pay higher costs.

- There is growing concern that China may be creating a glut of batteries, which will make excluding them even more difficult.

- There are increasing experiments using dense materials, such as sand, to hold heat which could then be used as batteries. Although not necessarily efficient, the material is cheap enough that, for some applications, it works quite well.

- In electrolysis, which splits hydrogen from oxygen in water and frees up the former for energy use, the process typically uses platinum as a catalyst. New studies suggest that gold and nickel might be more effective as a catalyst.

- One factor that is often overlooked in the energy transition is the role of efficiency. By using less fuel in transportation, HVAC, etc., less carbon will be emitted. Promoting efficiency through regulation tends to be less effective than through price, which is why economists always press for carbon taxes as the fastest way to promote the energy transition.

- As Europe warms, nations are finding that their housing stock is ill-equipped for higher temperatures.

- Australian researchers report progress on an air/zinc battery.

- For the first time, the U.S. auctioned wind energy leases in the Gulf of Mexico. The bidding was rather tepid.

- Germany is promoting geothermal energy to replace fossil fuels.

Asset Allocation Bi-Weekly – Examining the Rise in T-Note Yields (August 28, 2023)

by the Asset Allocation Committee | PDF

Perhaps the most interesting market event this month has been the rapid jump in 10-year Treasury note yields. At the end of May, the 10-year Treasury was yielding 3.64%, but recently the yield hit 4.36%. What’s behind this jump? Here are a few reasons behind the rise:

- Treasury borrowing is expected to increase with more supply coming into long-duration paper.

- The Bank of Japan is slowing giving up on yield curve control which will mean higher rates for Japan’s government bonds.

- Expectations of a recession in the U.S have dissipated; in fact, the recent GDPNow estimate from the Atlanta Federal Reserve Bank for this quarter’s real GDP is a whopping 5.8%.

All these reasons are valid. Our position has been that the 10-year Treasury yield has been too low for some time with the primary reason being that the market has been expecting the policy rate to decline faster than was likely.

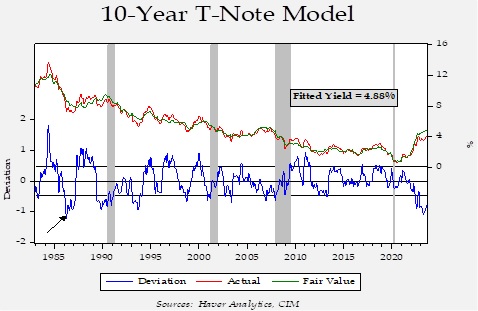

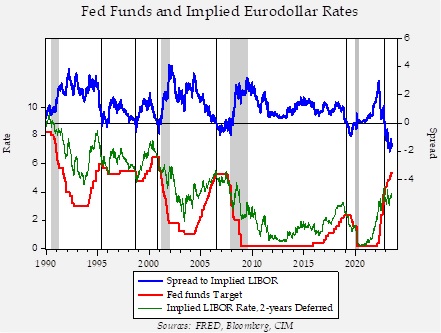

This chart shows our 10-year T-note yield model; its components include fed funds, the 15-year average of CPI,[1] the five-year standard deviation of inflation, German and Japanese 10-year yields, oil prices, the yen/dollar exchange rate, the fiscal deficit/GDP, and a binary variable for unified government. When the deviation is negative, it suggests the current yield is below fair value. As the chart shows, the current fair value is a yield of 4.88%.

Our analysis suggests the 10-year yield, even with its recent rise, is discounting a fed funds target of 3.40%. Such a rate is certainly possible but, barring either a financial accident or a rapid decline in economic growth, the FOMC has been signaling it will keep policy steady for an extended period of time. In other words, it may take a long time before the policy rate falls to this level. Despite these comments from policymakers, financial markets are still expecting the FOMC to cut rates.

This chart compares the fed funds target to the implied LIBOR rate, two-years deferred. With the demise of LIBOR, we have grafted the SOFR futures implied rate to the LIBOR rate. The upper line shows that the fed funds rate remains well above what the market is forecasting for short-term interest rates over the next two years. The market’s positioning isn’t unreasonable, as a recession will occur at some point. Although the onset has been delayed, with reasons discussed in our Q3 2023 Asset Allocation Rebalance Video, a downturn is still possible in the coming year. In the meantime, given how “rich” current 10-year T-note yields are relative to our model, we believe it is hard to make a case for extending duration.

On the 10-year T-note model chart, we have placed an arrow that shows the last time yields were this expensive. That period was 1986, and long-duration yields had plummeted due to a collapse in oil prices. As oil prices recovered, long-duration yields jumped. Although that period isn’t a perfect analog to the present, it does suggest that in the absence of recession, there is ample room for long-duration yields to rise further. Generally speaking, the longer the next recession is pushed into the future, the greater the odds that long-duration yields will rise further. Based off this analysis, we expect to favor shorter-duration fixed income until conditions change.

[1] We use this as a proxy for inflation expectations.

There will be no podcast for this week’s report.

Business Cycle Report (August 24, 2023)

by Thomas Wash | PDF

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. The intention of this report is to keep our readers apprised of the potential for recession, updated on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

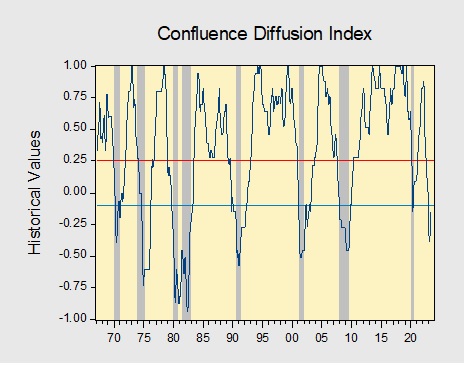

The Confluence Diffusion Index stagnated in a sign that the economy is still not in the clear. The July report showed that seven out of 11 benchmarks are in contraction territory. Last month, the diffusion index was unchanged at -0.1515, slightly below the recovery signal of -0.1000.

- Renewed optimism about the economy boosted stock prices.

- Higher interest rates led to a slowdown in homebuilding.

- The labor market is tight, but there are signs that hiring is starting to cool off.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is in recovery. The diffusion index currently provides about six months of lead time for a contraction and five months of lead time for recovery. Continue reading for an in-depth understanding of how the indicators are performing. At the end of the report, the Glossary of Charts describes each chart and its measures. In addition, a chart title listed in red indicates that the index is signaling recession.