Letter to Investors | PDF

About 125 years ago, a reporter spied J.P. Morgan on the streets of New York and ran over to get a prediction and a quote. “What will the stock market do?” the reporter asked the great banker and investor. “It will fluctuate,” was Morgan’s droll reply. The reporter dutifully reported the quotation but was disappointed in its generality. He was hoping to get a scoop! He anticipated getting a prediction from the man who knew the stock market better than almost anyone.

J.P. Morgan’s response has been ridiculed over the years, said to be both true and useless. I disagree. The great man did speak the truth, but he also gave us a most useful observation. The reporter was on a fool’s errand to think that this expert on the stock market could predict the future simply because he was learned. In this folly the reporter has had many followers. Many business reporters in print and television continue to press “experts” for predictions of the future. Morgan was not going to take the bait. He knew that the best thing an investor could do was to recognize that the stock market would fluctuate…and leave it at that.

Then why invest in stocks if all they’re going to do is fluctuate? You invest because you believe that over time the U.S. economy and the great companies within it will grow. Time is the investor’s friend. But investment is not what J.P. Morgan’s reporter and most daily viewers of CNBC are interested in. They want to know what the stock market is going to do tomorrow so they can speculate in stocks. Speculation requires a guess as to what a stock or an index will do in the very near future. Investment requires a calculation of the likely returns a company’s shareholders will receive over time. Speculators worry about stocks fluctuating because they may fluctuate in the wrong direction. Investors don’t worry about short-term fluctuations in prices. In fact, if the fluctuations are large enough, investors may use them as opportunities to either buy or sell.

This was illustrated by Benjamin Graham, the father of our profession, in his wonderful book, The Intelligent Investor. He tells us to imagine that we own an interest in a business, and that we have a partner in that business who is a benign, but insane, man named Mr. Market. Every day, Mr. Market decides to offer a price at which he is willing to buy your stake in the business or, in the alternative, sell you some more. The price he offers changes daily, depending on his mood. Some days he’s feeling greatly optimistic. Some days he is fearful that all will be lost. Thus, the price will bounce all over the place, often in the absence of any information that anything has changed.

Most of the time you can ignore Mr. Market. But a careful study of the business you own with him should lead you to conclude that, occasionally, when his offer price is absurdly high or low, you should take advantage of his offer. Graham concluded that most of the time an investor “will do better if he forgets about the stock market and pays attention to the dividend returns and to the operating results of his companies.”

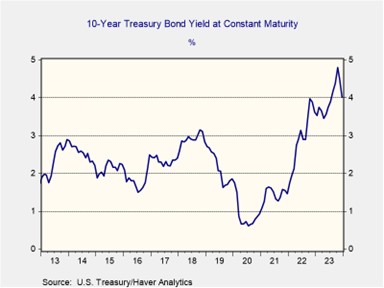

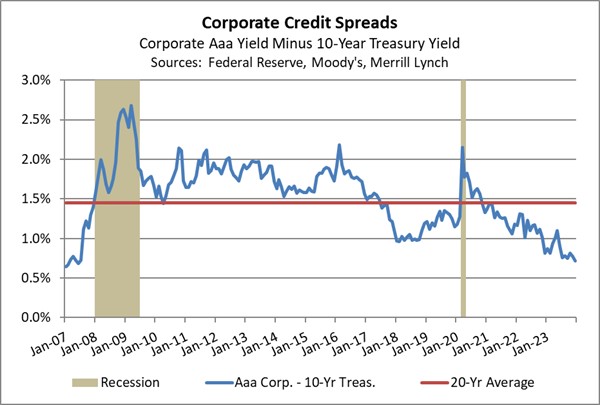

We have often seen the entire stock market behave like Mr. Market, even in recent months. On July 31 of last year, the S&P 500 (one of the broadest indexes of the U.S. stock market) closed at 4589. About three months later, on October 27, it closed at 4117, about 10.3% less, on virtually no change in the economy or business fundamentals. During that time frame, there was no change in the FOMC’s fed funds rate. All that had changed was Mr. Market’s increasing worry that the Fed might raise rates some more and hurt the economy. After October 27, Mr. Market’s worrying began to abate, and he began to be optimistic that the Fed might actually start to cut its fed funds rate. Thus, over the next 2 ½ months to January 17, the S&P 500 rose 15.1% to a close of 4739. Did much of anything change? No. The fed funds rate is the same as it was on July 31 of last year. All that changed was Mr. Market’s mood.

We have sought to build an investment process that is founded on Benjamin Graham’s analysis of J.P. Morgan’s observation: stock prices will fluctuate, but often not for any good reason other than the emotions of the moment. What we constantly remind ourselves is that we are buying and selling businesses, and that the value of those businesses rarely varies as much as Mr. Market’s daily offer price. We seek to buy and hold outstanding businesses, based on our definition of what makes for an outstanding business. Once we identify such a business, we then look for Mr. Market to offer it to us at an attractive price. If we are patient, he usually does just that.

Fundamental to this process is a belief that the price of a stock and its value are not the same thing. Oscar Wilde once famously said that “a cynic is someone who knows the price of everything, and the value of nothing.” I might say the same about many so-called investors. Knowing the price is easy: Mr. Market sets it for you every day. Knowing the value is the hard part: it is only discerned through a process of disciplined analysis. But, in our opinion, this is the only way to use Mr. Market’s unpredictability to one’s advantage.

Happy New Year to you and yours.

We appreciate your confidence in us.

Gratefully,

Mark A. Keller, CFA

CEO and Chief Investment Officer

View PDF

(Source: Heritage Foundation, 2024)

(Source: Heritage Foundation, 2024)