Author: Amanda Ahne

Asset Allocation Bi-Weekly – The UAE’s Exit From OPEC (June 1, 2026)

by Bill O’Grady | PDF

On May 1, the United Arab Emirates (UAE) formally exited both the Organization of the Petroleum Exporting Countries (OPEC) and the broader OPEC+ grouping of major oil producers. Such exits are not unheard of. For example, Indonesia suspended its membership in OPEC in 2015. However, Indonesia left the cartel not because it wanted to produce more oil, but because it had become a net oil importer. Qatar left the cartel in 2019, but there were several factors that led to its exit, including the fact that it had become more of a natural gas producer and Saudi Arabia and the UAE had isolated the country over its fostering of the news organization Al Jazeera.

Unlike Indonesia, the UAE has excess oil production capacity that represented about 25% of the cartel’s total. Like Qatar, tensions between Saudi Arabia and the UAE are elevated. The two countries have supported opposing sides in Yemen, for example.

In the immediate term, the UAE’s decision won’t affect the oil markets significantly. That’s because the Strait of Hormuz remains mostly closed. Although the UAE does have a pipeline to the Gulf of Oman, bypassing the strait, it is currently already fully utilized. Thus, the UAE can’t increase its oil output or exports until the US-Israeli war against Iran comes to some sort of resolution. But once that occurs, there will likely be a market impact.

Just what sort and how much of an impact is the focus of this report. To understand why the UAE’s action is important, it’s worth examining the role of cartels in the oil market. Oil supply has a tendency to be “lumpy.” On occasion, large oil fields are discovered and developed. Once these fields begin producing, supply usually increases dramatically. Oil demand is price inelastic, which means that in the short run demand doesn’t immediately react to the increase in supply. A glut of oil occurs, which brings sharply lower prices. Usually, suppliers react to the drop in price by reducing output. However, oil fields have limited flexibility in boosting or cutting output as oftentimes it can be very costly to reopen a well once it has been shut in. Oil is also unique compared to other commodities in that there is an incentive to continue producing once a well is operational because, if a producer were to stop, there would be nothing to prevent other drillers from pulling oil from the same field.[1]

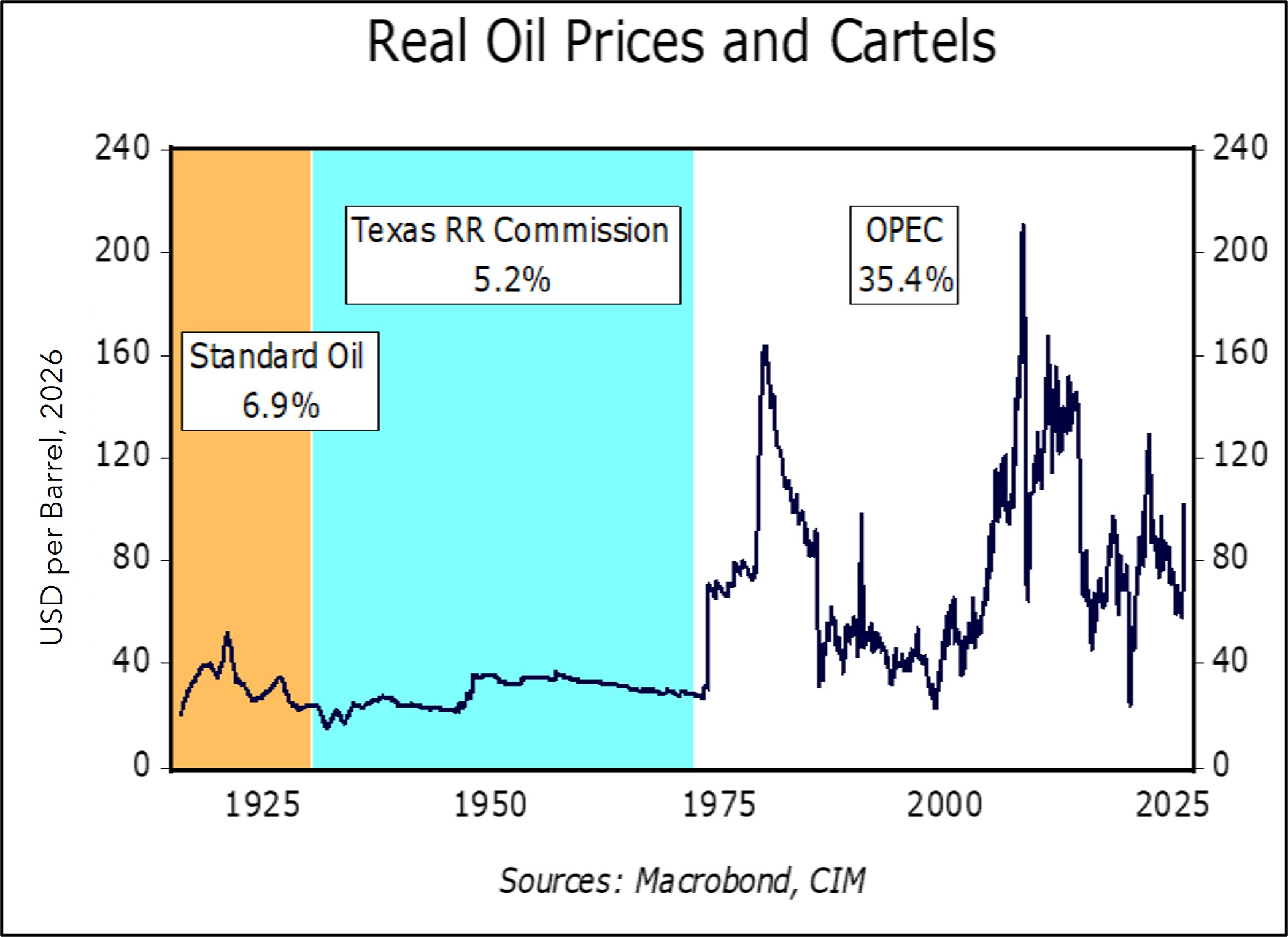

This situation can lead to collapsing prices. When the East Texas Oil Field was discovered during the Great Depression, production soared and caused prices to fall from $1.10 per barrel to $0.15 per barrel. Not only can such a glut be ruinous for producers, but the rush to generate cash flow can lead to overproduction and damaged reservoirs. In this example, the Texas Railroad Commission, which had authority to regulate oil production in the state, used the state militia to enforce production shares. The commission became the de facto cartel manager of the oil market, holding production off the market to keep the price higher than a free market would have generated, while also helping to stabilize prices. The Texas Railroad Commission held this role until 1972, when US consumption matched the state’s production capacity. From this point forward, OPEC became the cartel that manages the oil price.

The chart above shows the inflation-adjusted price of West Texas Intermediate oil, deflated by the US consumer price index. Although Standard Oil was formally broken up in 1911, its successor companies mostly managed production. From 1915 until 1930, the standard deviation of oil prices was 6.9%. The Texas Railroad Commission era shows a standard deviation of 5.2%. Clearly, OPEC has been the least successful cartel in terms of price management, with a standard deviation of 35.4%. But, as the chart shows, it has been successful at managing prices at times. For example, from 1986 through 1999, the standard deviation was 10.0%, even during the Gulf War.

Nevertheless, OPEC has struggled to manage prices in this century, with a standard deviation of 24.2%. First, it was unable to contain prices during China’s emergence after joining the WTO in 2001. It also struggled to manage the market following the advent of US shale oil.

The decision by the UAE to leave the cartel will likely further complicate price management. As we noted above, the decision doesn’t matter much while the Strait of Hormuz is blocked. However, once it reopens and supply chains are restored, the UAE’s production will be a bearish factor for oil prices. We expect Saudi Arabia will attempt to maintain price stability for a time, given the country’s history of cutting its output to preserve higher prices. But, as we saw in 1985 and again in 1999, the kingdom eventually decided that it was tired of providing support for “free riders” and punished overproduction by flooding the market with oil, and we would anticipate a similar outcome here. We don’t know when this moment will occur, but traders will have to factor this possibility into prices.

Complicating matters further is the closure of the Strait of Hormuz. Oil consumers now know that this region of the world is an unreliable supplier and will undoubtedly take steps to diversify energy sources moving forward. China’s ability to manage through an “all of the above” strategy will likely support alternative energy sources, such as coal, wind, solar, nuclear, et al. The uncertainty of oil supplies tends to depress demand over time. Therefore, even before the UAE’s decision, oil prices would have eventually had to decline enough to offset the uncertainty surrounding future supply. A smaller OPEC cartel will increase the likelihood of lower prices…eventually.

[1] As highlighted in the “milkshake” scene in the movie There Will Be Blood (1:34).

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Business Cycle Report (May 29, 2026)

by Thomas Wash | PDF

Note: This report was delayed due to severe data lags caused by the government shutdown. Although data for the missing months will not be released, the report is written as if no disruption occurred.

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. The intention of this report is to keep our readers apprised of the potential for recession, updated on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

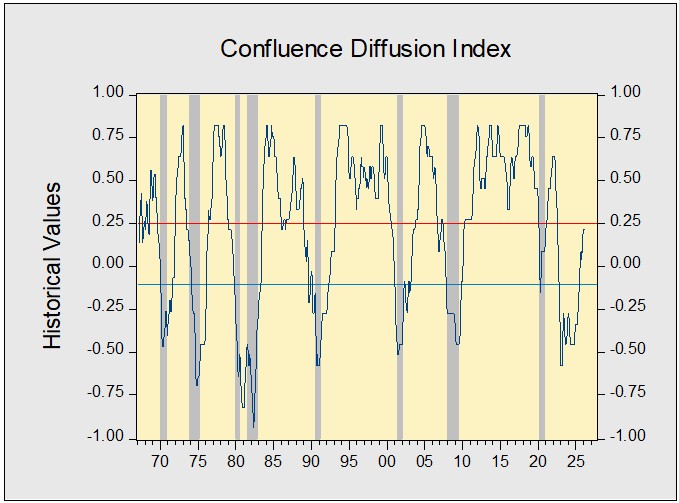

The US economy continued to expand in April, with overall conditions improving. Our proprietary Confluence Diffusion Index remained in expansionary territory for the fifteenth consecutive month, with no indicators entering or exiting contraction, leaving three of 11 signals in warning territory. That said, several areas warrant closer monitoring. Financial conditions point to ample liquidity — particularly within the technology sector — while signals from the real economy remain mixed. Business investment is holding up, but households and firms are increasingly concerned about higher inflation. Meanwhile, labor market momentum has strengthened.

Financial Markets

AI continues to support equities, with related stocks benefiting from sustained capital expenditure by large technology firms. Much of the improved sentiment since April has been driven by strong corporate earnings and expectations of de-escalation in the US-Iran conflict. This rebound in risk appetite comes roughly a year after the “Liberation Day” shock, with markets increasingly confident in their ability to look through geopolitical disruptions. At the same time, rising debt levels and renewed inflation concerns have pushed up both long-term yields and short-term rates, even as fiscal support continues to flow into the economy.

Goods Production & Sentiment

April’s economic data presented a mixed picture, as the war-driven energy shock weighed on both households and firms. Residential construction edged lower but remained resilient, with homebuilders navigating higher energy costs and borrowing rates. New orders strengthened as firms built inventories to get ahead of the potential supply chain disruptions tied to the conflict in Iran. Consumer confidence was the weakest component, easing from the prior month as households increasingly began to anticipate higher inflation for the months ahead.

Labor Market

The US labor market showed further signs of improvement, with hiring picking up modestly. Nonfarm payroll growth has resumed at a moderate pace, led by continued strength in healthcare, while transportation and warehousing are also gaining momentum. The unemployment rate edged higher and remains above levels seen two years ago. However, layoffs are still relatively contained, with initial jobless claims only slightly higher than the previous month.

Outlook & Risks

The economy remains on solid footing, supported by strong underlying fundamentals that were in place before the conflict in Iran escalated. We continue to expect the AI investment boom to support both growth and asset prices, as sustained capital spending underpins economic activity. However, we are increasingly concerned about the direction of monetary policy. The Federal Reserve has turned more hawkish in recent weeks, raising the risk of tighter credit conditions. This shift could become a headwind, particularly as firms and households grow more reliant on credit to finance investment and consumption. Still, the near-term outlook remains firm, while the medium- to longer-term trajectory is more cautiously optimistic.

The Confluence Diffusion Index for May, which provides a composite view of the economy based on 11 benchmarks, remains in expansionary territory according to April data. The index’s value was unchanged at +0.2121, well above the recovery signal threshold of -0.1000. The index shows that while the overall economic outlook is solid, we have not seen the full impact from the conflict in Iran. This is further evidenced by the fact that only three of the 11 benchmarks are in contraction, unchanged from last month.

- Rising inflation fears have led to a steeper yield curve.

- Consumer sentiment is being weighed down by inflation concerns.

- The labor market appears to be gaining momentum.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is in recovery. The diffusion index currently provides about six months of lead time for a contraction and five months of lead time for recovery. Continue reading for an in-depth understanding of how the indicators are performing. At the end of the report, the Glossary of Charts describes each chart and its measures. In addition, a chart title listed in red indicates that the index is signaling recession.

Daily Comment (May 29, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with our take on the latest progress in US-Iran negotiations. We then turn to AI, focusing on rising compute costs and what they mean for the pace of adoption. Next, we briefly discuss the EU’s push for greater control over critical supply chains and France’s unexpected economic contraction. We also include, as always, a review of recent domestic and international economic data.

New Deal? The United States and Iran have agreed to extend their ceasefire by 60 days, following Treasury Secretary Scott Bessent’s announcement that both sides have reached a preliminary framework for a deal that could reopen the Strait of Hormuz. While the agreement still requires approval from President Trump, it represents the clearest signal to date that the two parties are nearing a broader resolution. Markets have responded quickly to the development, with oil prices easing and Treasury yields falling.

- The White House appears increasingly confident that a deal is close. While details remain limited, Bessent has emphasized that any agreement must meet three core conditions: the reopening of the Strait of Hormuz, Iran relinquishing its enriched uranium, and a full cessation of its nuclear program. In addition, the US is insisting that all transit through the strait remain free of tolls.

- Iran has thus far negotiated in good faith, pressing for the release of approximately $24 billion in frozen assets as part of any agreement. It is also seeking an end to Israeli strikes in Lebanon and some degree of influence over maritime traffic through the strait. On the nuclear front, Iran would prefer to retain its enrichment program but has signaled a willingness to transfer enriched material to China or Russia as a potential compromise.

- The interim deal now awaits President Trump’s final approval, with reports suggesting he intends to take several days to review the terms despite markets already largely pricing in a green light. Following Bessent’s announcement, WTI crude fell below $90 per barrel for the first time in over a month, while the 10-year Treasury yield declined nearly 10 basis points to 4.43%. These moves reflect growing market confidence that a resolution to the conflict could alleviate the supply chain disruptions triggered by the escalation.

- While markets appear confident that a deal will be reached, we remain more cautious. Although the president typically welcomes market reassurance, he has also shown a preference for securing a clear, tangible win — something this framework may not fully deliver. We are cautiously optimistic that cooler heads will prevail. However, a rejection of the deal would likely trigger a sharp market reaction and could raise the risk of renewed escalation.

AI Costs: More firms are beginning to rein in AI spending as usage costs increasingly pressure budgets. On Thursday, Amazon announced plans to dismantle its internal AI leadership board in an effort to discourage the use of AI for its own sake rather than for clear productivity gains. The move follows internal findings that some employees were deploying AI for low-value or unnecessary tasks — a trend increasingly referred to as “tokenmaxxing.” This shift toward tighter controls suggests that the pace of AI adoption may be slowing as firms look to rein in costs.

- As AI adoption has accelerated, providers have periodically struggled to keep up with demand given finite computing capacity, leading to the use of quotas and rate limits to manage usage. Anthropic, for example, initially tightened Claude Code limits in response to “unprecedented demand,” but more recently has been able to raise those limits significantly after securing additional compute capacity through a new partnership with SpaceX and other cloud providers.

- Another sign that AI costs are mounting is the trend of companies moving toward public markets. This shift will likely force these firms to prioritize profitability over aggressive market share expansion. Anticipated IPOs from industry leaders like OpenAI, Anthropic, and SpaceX could provide a necessary capital influx; however, these moves will also subject the companies to intense public scrutiny regarding revenue targets and fiscal discipline.

- Despite the hype around AI, questions remain about its ability to generate robust returns on investment. A widely cited MIT study released in August 2025 found that more than 95% of surveyed firms had yet to demonstrate a positive ROI from their AI initiatives. A follow‑up report from PwC in January indicated that 56% of CEOs saw neither higher revenues nor lower costs from AI over the prior 12 months, and only about 12% reported achieving both outcomes.

- AI still appears poised to be a positive force for the economy and markets over time, but we are increasingly focused on the buildup of related risks. Rising implementation and infrastructure costs, in particular, could slow future adoption and make it harder for AI providers to deliver on today’s lofty expectations. In this environment, it remains sensible to maintain broader tech exposure, while continuing to monitor concentration and valuation risks.

EU Chip Takeover: The EU is weighing emergency powers that would allow it to compel chipmakers to override existing contracts in times of crisis. The proposal is intended to reduce the bloc’s vulnerability to economic coercion from the US and China, given Europe’s heavy reliance on imported semiconductors. It also follows the Dutch government’s controversial intervention involving chipmaker Nexperia and underscores how, in a less globalized world, governments are likely to take a more active role in strategic sectors of the economy.

France Contraction: The French economy unexpectedly contracted in the first quarter. According to the national statistics office Insee, GDP fell 0.1% quarter‑on‑quarter, weighed down by weaker exports and soft domestic demand. While some observers view the decline as a one‑off that could be reversed in the second quarter, concerns persist that France’s rising debt burden, new US trade restrictions, and the energy shock linked to the conflict in Iran could pose additional headwinds to growth.

Daily Comment (May 28, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with our thoughts on a potential AI tax. We then turn to Federal Reserve policy and the possibility of a rate hike. Next, we provide brief updates on the US-Iran conflict and the rise in semiconductor stocks. As always, we include a review of recent domestic and international economic data.

Taxing AI: In a recent Time op-ed, Senator Elizabeth Warren (D‑MA) called for changes to the tax code that would channel a portion of AI‑related gains into federal revenue and ensure the benefits are shared more broadly with everyday Americans. Her proposal comes as lawmakers search for ways to make rapid advances in AI more politically and socially acceptable to voters. It also lands at a moment when AI is playing a growing role in the economy while facing mounting public backlash over its pace of adoption, perceived equity implications, and the extent to which its expansion is seen as being facilitated by government support.

- Most of her tax proposals are familiar, including a wealth tax and higher capital gains taxes, and do not target AI specifically. However, she is also floating a more novel idea: an excise tax on data centers’ energy usage, which has received limited mainstream attention so far. In her view, such a levy would help large tech firms compensate local communities for higher utility costs tied to surging data‑center demand, and support the competitiveness of US companies in the global AI race.

- The idea of taxing data centers is not new as there has also been a recent push to tax computer processing. The key distinction between taxing energy and taxing computation is that an energy tax applies to the electricity consumed, while a compute tax applies to the volume of computational work itself. An electricity tax mainly nudges firms toward cheaper or cleaner power sources, whereas a compute‑based tax would more directly incentivize reducing or optimizing workloads.

- The renewed push to tax AI comes as major tech companies sharply increase capital spending to keep up with surging demand for the technology. In 2025, Nvidia CEO Jensen Huang argued that computing capacity will need to scale by orders of magnitude — potentially up to 1,000x — to support more advanced, agentic forms of AI. If AI capacity growth continues on this trajectory, an AI‑linked tax on energy use or consumption could become a meaningful revenue source for governments over time.

- While the idea of an AI tax remains purely speculative for now, it could gain momentum heading into the 2028 election. If enacted, such a tax would likely create a headwind for tech companies that rely heavily on data centers, as it would increase their operating costs. However, if AI continues to grow as fast as projected, the tax could also help raise government revenue and reduce the national debt, which might ultimately bring down longer-term bond yields.

Hikes Possible? Nearly a month after the last FOMC meeting, Fed officials appear to be shifting away from an easing bias toward a more tightening-oriented stance. Following Governor Christopher Waller’s call to abandon the easing bias, several policymakers have begun signaling openness to a rate hike later this year. This shift in sentiment will likely place upward pressure on bond yields, as markets begin to reprice the policy path to reflect a higher probability of further tightening.

- On Wednesday, Fed Governor Lisa Cook highlighted a range of risks to the Fed’s price stability mandate, including artificial intelligence related disruptions, tariffs, and escalating tensions with Iran. She indicated a willingness to raise interest rates if inflation remains elevated. In contrast, Fed Governor Philip Jefferson struck a more optimistic tone suggesting that current policy remains well positioned, noting that inflation appears to be cooling, while emphasizing that upside risks to inflation persist.

- Inflation risks are rising as the Federal Reserve confronts a series of overlapping supply shocks. The AI build-out is lifting household utility costs and memory chip prices, while tariffs are increasing import prices. At the same time, the war in Iran is pushing up energy and food costs. These pressures are already feeding into goods prices — historically the more responsive component — but may increasingly spill over into services, where disinflation has proven far more persistent.

- The recent shift in risk sentiment has started to push the 10‑year Treasury yield higher. Market pricing indicates that the 10‑year yield remains highly sensitive to year‑end fed funds expectations. That tight relationship reflects the fact that long‑term yields are largely driven by the expected path of short‑term rates plus the term premium investors demand for bearing inflation, and bond supply risk over time. However, we think geopolitical risks may also be impacting term premia.

- The Fed’s pivot marks the start of a new regime during which the central bank must navigate recurring, supply‑driven geopolitical shocks — something it has not faced at this scale before. This backdrop is likely to complicate monetary‑policy calibration over the next several years, particularly as the global economy continues to deglobalize. In our view, that combination argues for elevated volatility in long‑term rates as the Fed adapts its reaction function to an evolving geopolitical landscape.

Iran Setback: The US on Thursday carried out multiple strikes on Iranian targets in the Strait of Hormuz, underscoring its commitment to keeping the waterway open. Ahead of the strikes, the US president vowed not to allow any actor to control the strait and warned Oman, a US ally, against supporting any Iranian effort to impose a toll in the region. Although the current truce still appears to be holding, developments on the ground suggest the ceasefire remains fragile.

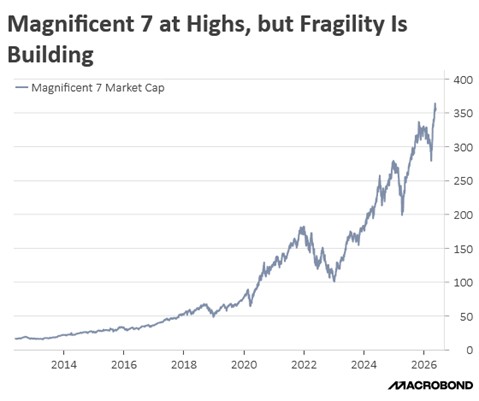

Chipmakers Rise: AI enthusiasm has propelled chipmakers to their strongest run since the dot‑com era. The PHLX Semiconductor Index is up roughly 75% year‑to‑date, marking its best start to a year since 1999. The move has been driven largely by surging AI‑related capex and earnings expectations, even as macro and geopolitical uncertainty remain elevated. While we see scope for further upside in the near term, we continue to advocate adding value exposure as a way to mitigate concentration risk in AI‑heavy growth names.

Daily Comment (May 27, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with our takeaways from the pope’s first encyclical letter. We then turn to the war in Ukraine and its broader implications for modern conflict. Next, we briefly review the strong performance of chipmakers, the Texas primary, and the latest consumer confidence data. As always, we conclude with a summary of recent domestic and international economic developments.

Pope’s AI Warning: Although artificial intelligence is becoming more ubiquitous, there are growing calls for stronger guardrails. Over the weekend, Pope Leo XIV compared the rush to develop AI to the Tower of Babel in Genesis, using the analogy to underscore rising unease about both the pace of innovation and growing overconfidence in its ultimate impact. His remarks come amid broader concerns that the market’s enthusiasm for AI could prove vulnerable to a reversal if expectations run ahead of reality.

- In Genesis 11, the Tower of Babel serves as a cautionary account of human ambition outpacing restraint. The story describes a unified effort to build a city and a tower reaching the heavens — an expression of collective confidence and self-sufficiency. In response, God disrupts the project by confounding their language and dispersing the population, effectively halting progress. The episode is often interpreted as a warning about the risks of unchecked ambition and the limits of human control.

- The pope’s appeal comes at a moment when the rapid rollout of AI is generating significant disruption but, so far, only modest and uneven gains. A recent research paper from the Federal Reserve Bank of San Francisco finds that AI’s impact on productivity has been mixed, with benefits concentrated in a few sectors and slow diffusion elsewhere. Reflecting similar concerns from the private sector, Uber’s COO has acknowledged that the company’s substantial AI investments have yet to deliver consistently strong returns.

- AI remains the dominant market theme, but the related stocks have been highly volatile. They sold off in fall 2024 on worries about frothy valuations after Nvidia’s earnings underwhelmed sky‑high expectations. The group weakened again in early 2025 after DeepSeek’s launch, which investors saw as a competitive threat to leading US AI firms. Another downturn in fall 2025 followed renewed concerns that circular revenue models in the AI ecosystem were undermining the durability of underlying business momentum.

- AI still has strong momentum, but we think the rally is vulnerable to a sudden shock that could reset expectations, even if no such trigger is currently visible. We therefore recommend maintaining some exposure to value stocks as a buffer in periods of uncertainty, given their tendency to outperform during past episodes of market stress. While this diversification can mean some relative underperformance in powerful growth-led rallies, it also supports better capital preservation over time.

The Forgotten War: While there are tentative discussions about ending the US-Iran standoff, the war between Russia and Ukraine appears to be entering a new phase. On Tuesday, Moscow warned civilians and diplomats to leave Kyiv as it announced plans to target “decision‑making centers” in Ukraine’s capital. The escalation comes as Russia seeks to regain momentum after recent setbacks. The ongoing conflict in Ukraine also helps explain why the United States and Iran are struggling to find a clear off‑ramp as markets push for de-escalation.

- Moscow’s decision to escalate the conflict comes as momentum on the battlefield has shifted against it. In recent months, Ukrainian forces have regained some territory, though it remains unclear whether they can decisively tilt the war in their favor. A key concern for the Kremlin is that domestic support for the campaign may be eroding, and authorities have reportedly tightened control over Telegram, a popular social media platform, in an effort to shape and contain the narrative.

- Moscow is contending with setbacks, but Ukraine is also facing mounting challenges. A report on Monday indicated that roughly half of the countries participating in the Czech-led ammunition initiative for Ukraine have pulled out, potentially constraining supplies of badly needed shells and other munitions. Although the specific states that withdrew were not identified, Germany and several Nordic countries are reported to be continuing their military support for Ukraine.

- Ukraine and Iran’s abilities to prolong conflict reflects how cheaper weapons, particularly drones, have made it easier and less costly for states to defend their territory. These capabilities mean that, even if they cannot decisively defeat a stronger adversary, smaller countries can continue fighting and inflicting damage despite losses of key military systems. In this environment, they have little incentive to accept unconditional surrender.

- Similar to the US-Iran conflict, the lack of a clear victory has made it difficult for the two sides to reach an agreement, largely due to concerns about political backlash from the costs incurred. Russia is in a particularly difficult position, as it needs something to show for its massive casualties and the likely continued isolation resulting from the invasion. These prolonged conflicts are likely to become more common, as cheaper weapons make it easier for smaller nations to fight larger ones.

Chip Demand: AI chipmakers Micron and SK Hynix have both crossed the $1 trillion mark as demand for processors that power cloud-based AI services continues to outstrip supply. Memory chip producers, in particular, underscore the centrality of hardware to AI build‑outs and have been among the largest beneficiaries of big tech’s infrastructure push. Yet, while these companies are thriving today, it is important to remember that the chip industry has historically been highly cyclical, with frequent booms and busts driven by shifts in supply and demand.

Texas Primary: Texas Attorney General Ken Paxton defeated Senator John Cornyn in the Republican Senate primary. His victory has created an opening for Democrats, as James Talarico is currently viewed as having a slight edge in early polling. A Democratic pickup of this seat would significantly increase the odds that Republicans lose their Senate majority. Reflecting this shift, the Cook Political Report moved the race from “likely Republican” to “lean Republican.”

Consumer Confidence: The Conference Board reported a modest easing in consumer sentiment in May. The decline reflects persistent inflation concerns, which continue to weigh on household expectations for future prices of goods and services. Compared with the University of Michigan survey, the Conference Board’s measure — typically more sensitive to labor market conditions than inflation — has shown a more moderate deterioration. Even so, the data indicates that household economic expectations remain notably less optimistic than prevailing market sentiment.

Confluence Mailbag – #10 “The End of Hegemony, the Iran Stalemate, and the AI Bubble” (Posted 5/26/26)

Daily Comment (May 26, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with an update on the Iran war, where the optimism over a potential new peace deal late last week has started to give way in the face of new US attacks on Iran’s military over the last 24 hours. We next review several other international and US developments that could affect the financial markets today, including new data showing that rising prices are starting to push down consumer purchasing power around the world and new research indicating that deregulation has opened up huge new lending opportunities for US banks.

United States-Israel-Iran: Despite statements late last week by President Trump and other US and Iranian officials indicating a 60-day ceasefire extension was in the works, the president, starting on Saturday, suggested the deal could still take several days to be finalized. Of course, the hints of a new deal could be mostly political posturing as in the past. It would not be a surprise if no deal materializes this week. The US yesterday also launched attacks on Iranian missile sites and mine-laying boats, further undermining hopes for a more permanent end to the fighting.

- In any case, the key point is probably that even if a peace deal is struck, normalizing global energy and commodity flows in the Middle East would likely take a year or more. That suggests global energy and commodity prices are likely still at risk of further increases, which would potentially weigh on economic growth around the world, drive government bond yields even higher, and cause important political implications.

- Separately, Israeli Prime Minister Netanyahu ordered his military to step up its attacks on the Islamist militant group Hezbollah in southern Lebanon. The move came after far-right members of Netanyahu’s cabinet demanded a full-scale resumption of Israel’s offensive there in defiance of the US administration’s preference that they stand down to support the current US-Iranian ceasefire.

- While global oil prices had fallen sharply into the weekend on hopes for a peace deal, the new US strikes on Iran and Iranian threats to retaliate have given a boost to oil prices this morning. Near futures prices for Brent crude are up some 2.9% so far today to about $96.20 per barrel.

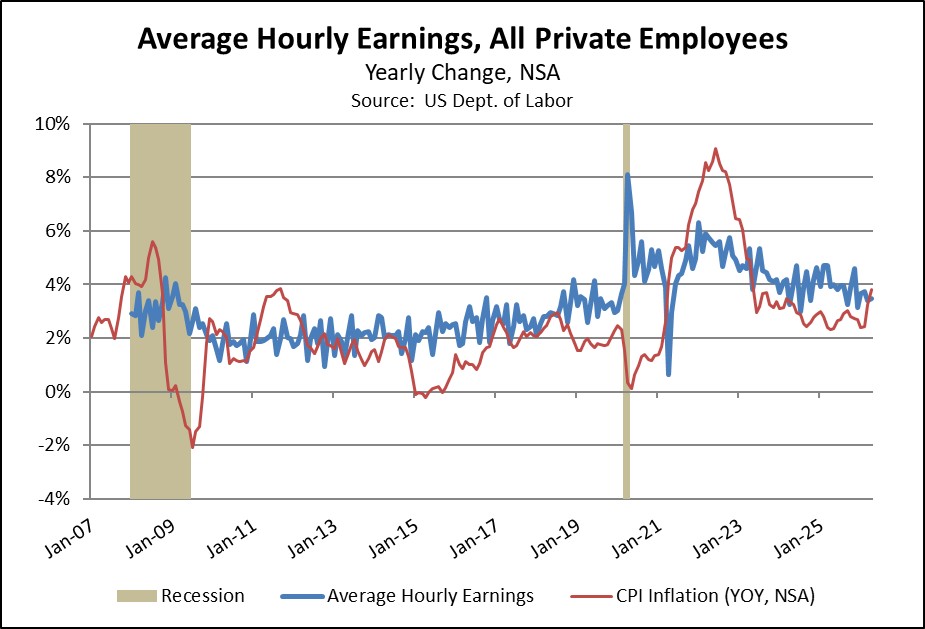

Global Labor Market: An article in the Financial Times today notes that spiking prices for energy and other commodities are threatening to cut the total purchasing power of workers around the world. In the US, for example, we have noted that the consumer price index in April was up 3.8% from the same month one year earlier, while average hourly earnings were only up 3.5%. The FT article notes that the trend is moving in the same direction in economies such as the UK and the eurozone, which will likely weigh on growth and asset values.

European Union-China: Five key EU countries have signed a paper calling for the bloc to respond more aggressively to “systemic and structural industrial overcapacity,” a phrase that is often taken as shorthand for China. The paper by the Netherlands, France, Spain, Italy, and Lithuania illustrates how the EU is increasingly riven by disagreements over whether to engage more closely with Beijing to offset a fraying US relationship or erect strong trade barriers to protect domestic industries.

- The issue will be discussed at an EU summit on Friday.

- For investors, the risk is that if trade and investment flows between the EU and China remain relatively unfettered, EU companies could gradually be weakened, even if they preserve some economic opportunities in the short term. However, tougher trade and investment barriers could lead to a trade war that results in immediate disruptions.

United States-Japan: The US has reportedly warned Japan that its purchase of 400 Tomahawk cruise missiles will be severely delayed as Washington works to rebuild its depleted arsenal after the Iran war. Japan’s Tomahawk purchase was meant to give it advanced strike capabilities and help it defend itself against China while it worked to develop its own missiles. The delay will likely spur Japan to redouble its missile development efforts, potentially giving further impetus to its expanding defense industry and creating new investment opportunities.

United Kingdom: New data yesterday said bank lending to non-financial companies fell to 59% of the UK’s GDP in the third quarter of 2025, marking the lowest level in almost 30 years. The figures were especially weak for lending to small- and medium-sized firms. The reduced bank lending reflects both weak economic growth and tougher bank regulation.

Indonesia: In a little noticed announcement last week, President Prabowo said the government will take control of the country’s major commodity exports. The first two commodities brought into the plan will be coal and palm oil. By taking the control of foreign commodity sales away from legions of middlemen, Prabowo’s goal is to curb tax evasion and improve efficiency. However, few details have been released, leaving producers and current middlemen unsure of how to proceed.

US and UK Banking Industries: New research by consultancy Alvarez & Marsal has found that deregulation allowed major banks in the US and UK to expand their balance sheets by a cumulative $1.3 trillion over just the last two quarters, giving them a significant leg up on their more constrained rivals in the eurozone and Switzerland. The figure illustrates the under-appreciated impact of recent reforms in the US and UK, which should be supportive of those countries’ bank stocks.

Daily Comment (May 22, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with our perspective on why lawmakers are struggling to regulate AI. We then examine the latest developments in the US-Iran conflict. We also briefly address the spread of the Ebola outbreak to additional countries, the US’s decision to delay certain weapons sales to Taiwan, and early indications that governments are moving to reassure bond investors. As always, we conclude with a comprehensive roundup of the latest international and domestic economic indicators.

Rising AI Pushback: Lawmakers are still struggling to balance the push to promote AI with the need to protect their communities. On Thursday, the president chose to delay the signing of an executive order that would have imposed stricter oversight on the development of AI tools. He is far from the only official wrestling with how best to regulate the technology, yet his hesitation underscores how optimistic government officials remain about AI’s potential benefits. Even so, growing unease among voters is starting to pressure lawmakers to act.

- One factor behind the postponement appears to be divisions within the White House itself. Treasury Secretary Scott Bessent has taken a leading role in advocating for rules to govern AI in the wake of Mythos, which has demonstrated an ability to expose vulnerabilities in the nation’s core infrastructure and financial system. He has been pressing the national security team to move more quickly to put these guidelines into place.

- On the other hand, there are also concerns that imposing too many rules could leave the United States at a competitive disadvantage to China in the AI race. This camp, reportedly led by National Cyber Director Sean Cairncross, has sought to slow the process, arguing against new regulations without a clearer sense of the potential costs. To bridge the divide, officials have pushed for more feedback from outside the White House on how prospective rules might affect both the private and public sectors.

- Public debate over AI regulation is intensifying just as public sentiment toward the technology begins to deteriorate. Opposition to new data centers has been particularly strong in parts of Texas, which now hosts the largest facility of its kind globally. Concerns range from noise and environmental impact to significant energy consumption, with surveys indicating that these projects rank among the least popular local developments.

- While AI continues to exhibit strong momentum, it is likely to encounter increasing political and regulatory headwinds. We suspect such resistance could moderate the pace of earnings growth these firms have recently delivered and potentially weigh on investor sentiment toward the sector. In this context, we continue to advocate maintaining some exposure to value as a potential buffer against a shift in market momentum.

Iran Deal Close? There are growing signs that the US and Iran are moving closer to a potential agreement that could lead to the reopening of the Strait of Hormuz. Iranian officials have signaled that the latest US proposal has helped bridge key gaps between the two sides as indirect negotiations continue. Remaining points of contention appear to center on Iran’s right to uranium enrichment and the authority to impose transit tolls. While talks are still ongoing, the prospect of a deal has begun to ease market tensions as participants await further clarity.

- Signs of progress come as Iran approaches the US deadline for potential strikes within the next few days. Earlier this week, the president warned that an attack was under consideration but extended the timeline following pushback from Middle Eastern countries concerned that they could become targets in the event of a strike on Iran. However, Trump indicated that military action could begin as early as this weekend.

- On Friday night, a UAE power plant was targeted in a drone attack launched from Iraq, forcing the facility to rely on backup generation to avoid broader disruptions. Although Iran did not claim responsibility, the incident is widely viewed as a signal of the potential escalation risks should the US resume military action.

- The prolonged duration of the conflict is beginning to exert a more pronounced drag on the economy. The latest ISM report shows a sharp rise in inventory accumulation, suggesting that demand pressures are broadening. As firms compete more aggressively for limited inputs, this dynamic could contribute to more persistent inflationary pressures and further weigh on global economic growth.

- While signs of progress in the conflict are encouraging, a resolution does not appear imminent, as neither side appears willing to make meaningful concessions. Meanwhile, rising inflationary pressures are likely to weigh on bond prices, prompting investors to reduce duration exposure. In this environment, private credit and business development companies could benefit from their floating-rate structures, particularly as default rates and spreads remain relatively contained.

Ebola Outbreak: Concerns are growing that the Ebola outbreak could spread across Africa. While currently confined to the Democratic Republic of the Congo and Uganda, experts fear the virus may reach three additional countries on the continent. The situation remains critical, with over 500 confirmed cases and 150 fatalities reported to date. Although there is no evidence that the outbreak has reached other continents, international medical response is active; notably, one American citizen is currently receiving treatment for the virus in Germany.

Taiwan Sales on Ice: The Pentagon has informed Taiwan that it will delay certain weapons sales amid the conflict in Iran. While officials maintain that US stockpiles are sufficient, the move reflects a desire to preserve readiness ahead of potential escalation. It may also signal an effort to avoid straining ties with China as Washington seeks Beijing’s support in easing Middle East tensions. That said, the decision could encourage Asian nations to further diversify their defense supply chains.

Bond Yields Ease: Japanese and UK bond yields have eased amid signs that policymakers may act to address supply-demand imbalances. In Japan, the Ministry of Finance has signaled a reduction in long-duration issuance. In the UK, potential Labour challenger Andy Burnham has indicated he would maintain existing fiscal targets if he were to replace Prime Minister Keir Starmer. We expect continued bond market pressure to push governments toward policies aimed at containing further increases in yields.

Note: Due to the holiday, the Comment will not be published on Monday.