by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EDT] | PDF

Our Comment opens with an update on the Russia-Ukraine war, including news that Russian President Putin has launched a major purge and reorganization of his top military command amid ongoing shortcomings in the war effort. We next review other international and U.S. developments with the potential to affect the financial markets today, including wide-ranging fallout from the war and signs of further labor union actions. We close with the latest news on the coronavirus pandemic.

Note: Because COVID-19 has become more endemic and in most countries isn’t disrupting the economy or politics as much as it did previously, we will drop our dedicated COVID-19 section beginning July 1. We will continue to cover pandemic news as needed within our main text.

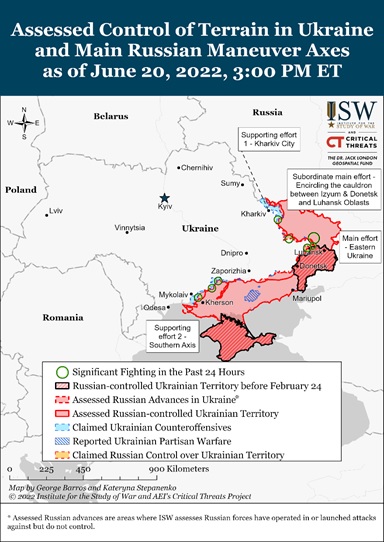

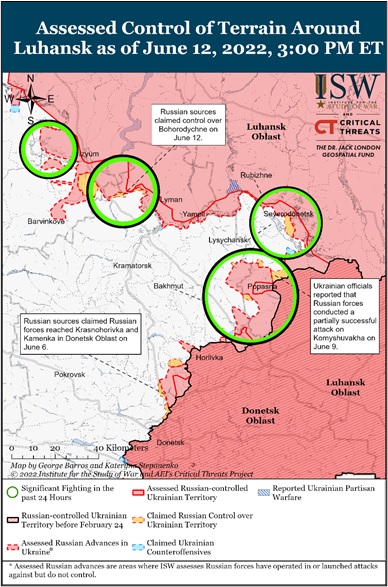

Russia-Ukraine: Even as Russian forces continue to make slow, plodding progress in seizing Ukraine’s northeastern Donbas region, new intelligence reports indicate President Putin has fired Army General Alexander Dvornikov from his role as the commander of Russia’s Southern Military District (SMD), which also entailed leading the invasion of Ukraine. Putin has instead named Army General Sergey Surovikin as head of the SMD and, separately, Colonel-General Gennady Zhidko, the head of the Military-Political Directorate of the Russian Armed Forces, as commander of the invasion. Notably, the Military-Political Directorate is focused on maintaining morale and ideological control over the military, just as it did in the Red Army during the Cold War. These personnel moves, along with others, suggest Putin is carrying out a broad purge of underperformers, which in itself is additional evidence that the Russian forces are still struggling with massive shortcomings in the face of strong resistance from the Ukrainians.

- In other war news, a major Russian oil and gas refinery close to the Ukrainian border was set ablaze today after a drone allegedly controlled by Kyiv’s forces crashed into it. Video on social media showed two drones crashing into the facility and setting off the fire, and local authorities claim they have recovered the remains of both drones. If the drones prove to be “kamikaze” weapons recently provided by the West, the attack on Russian soil would further inflame President Putin and tempt him to escalate the conflict.

- Indeed, Russian military forces have been staging mock missile attacks on NATO member Estonia as part of their planned exercises close to the Estonian border. Reports indicate a Russian military helicopter also crossed into Estonian airspace with its transponders off, prompting Tallinn to call in the Russian ambassador to complain.

- As Russia continues crimping its natural gas deliveries to Western European countries in retaliation for their sanctions and other support to Ukraine, International Energy Agency chief Fatih Birol warned the Europeans must prepare immediately for the complete severance of Russian gas exports this winter.

- According to Birol, “The nearer we are coming to winter, the more we understand Russia’s intentions. I believe the [gas] cuts are geared towards avoiding Europe filling storage, and increasing Russia’s leverage in the winter months.”

- To help cushion the blow, Birol urged Western European governments to take further measures to cut demand, temporarily fire up old coal-fired electricity plants, and keep ageing nuclear power stations open.

- He also suggested that any additional CO₂ emissions from burning coal would be offset by an acceleration in Europe’s plans to cut its reliance on imported fossil fuels and build up renewable generation capacity.

- Industry executives say the Indian government has encouraged its state-owned energy companies to scoop up cheap Russian crude that otherwise wouldn’t have a market because of Western sanctions. The Indian purchases, which include new long-term contracts, will take the sting out of the sanctions and essentially help provide funding for Russia’s invasion of Ukraine.

Italy: The anti-establishment Five Star Movement, the largest party in Prime Minister Draghi’s national unity government, is splitting up amid internal disputes over the war in Ukraine.

- Foreign Minister Luigi Di Maio, one of the party’s most prominent members and a strong supporter of Italy’s backing of Ukraine, said he would form a new, pro-government party that will remain in the governing coalition. He will take about 60 of the party’s 227 lawmakers with him.

- That could eventually prompt Former Prime Minister Conte to pull his more radical followers out of the coalition and potentially bring down the government.

Georgia: After the European Commission recommended against giving the country EU candidate status last week, tens of thousands of Georgians have been protesting in the streets of Tbilisi and casting blame on the government. The protests against the pro-Kremlin leadership are another example of how Putin’s invasion of Ukraine has backfired by further isolating Russia and its supporters.

United Kingdom: As a strike by railway workers has already shut down much of the U.K.’s transportation system, the country’s main teacher unions are threatening to walk off the job this autumn if the government doesn’t agree to a 12% pay hike for their members. The news illustrates how labor has come to feel more empowered in major developed countries, threatening further strikes and other measures to bring down wealth and income inequality. If successful, the labor actions could lead to higher business costs, more inflation, narrower profit margins, and potentially lower equity valuations going forward.

Global Travel Chaos: With the end of pandemic restrictions leaving people desperate to travel but airlines stuck with insufficient workers, airports across the globe are struggling with flight delays, cancellations, long lines, and lost baggage. Some airport officials are bracing for the disruptions to last into the fall, forecasting that pent-up demand for travel won’t let up.

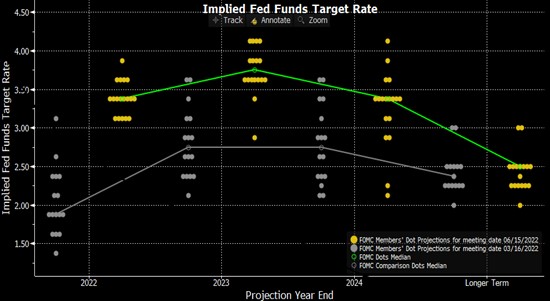

U.S. Monetary Policy: Treasury Secretary Yellen, a former Federal Reserve governor, yesterday argued that the Fed’s current interest-rate hikes could bring down inflation without pushing the economy into recession. According to Yellen, today’s unusually low labor force participation rate means there are plenty of workers on the sidelines who could start looking for work because of rising wages.

- In Yellen’s view, increased labor supply coupled with rising interest rates would help bring down inflation before economic growth slows too much.

- We would note, however, that the labor force participation rate hasn’t shown signs of improving much, even after many months of high and rapidly rising wage rates.

- We also may get Fed Chair Powell’s view on the matter today, when he begins two days of testimony before Congress on the central bank’s monetary policy plans. Powell and other current Fed policymakers are clearly panicked about inflation and seem willing to risk an economic slowdown by tightening policy aggressively, even if they aren’t willing to say so publicly. Concern over what Powell might say in that regard is probably a key reason global risk markets are weaker so far today.

U.S. Fiscal Policy: President Biden today will propose a three-month suspension of the federal gasoline tax of 18.4 cents per gallon. As we noted in our Comment yesterday, the federal tax only amounts to about 3.7% of today’s average retail price, illustrating how Biden is stuck with few good ways to address soaring energy prices in the near term. On top of that, lawmakers in Congress look unlikely to approve the plan.

U.S. Regulatory Policy: The Biden administration yesterday indicated it plans to issue a rule eliminating virtually all nicotine from cigarettes to make them less addictive and help people quit smoking. Under the plan, the FDA will formally propose the rule on May 23, although it probably wouldn’t take effect until years after that date.

U.S. Labor Market: While the major economic data series are starting to hint at a slowdown in the economy, more granular private data and anecdotes are doing the same. According to the Wall Street Journal, more companies in multiple industries have been rescinding job offers in recent weeks. Many major firms have also announced reduced hiring plans, hiring freezes, and even layoffs. We expect labor demand to cool further in response to factors such as rising interest rates, high inflation, slowing economic growth in China, and uncertainty regarding the Ukraine war.

COVID-19: Official data show confirmed cases have risen to 540,643,457 worldwide, with 6,322,412 deaths. The countries currently reporting the highest rates of new infections include the U.S., Taiwan, Germany, and Brazil. (For an interactive chart that allows you to compare cases and deaths among countries, scaled by population, click here.) In the U.S., confirmed cases have risen to 86,456,273, with 1,014,040 deaths. In data on the U.S. vaccination program, the number of people considered fully vaccinated now totals 221,924,152, equal to 66.8% of the total population.

- In the U.S., the latest wave of infections appears to be topping out, but hospitalizations are still accelerating with their usual lag. The seven-day average of newly reported cases stands at 96,218, down 15% from two weeks ago. The seven-day average of people hospitalized with confirmed or suspected COVID-19 came in at 29,934 yesterday, up 2% from two weeks earlier. New COVID-19 deaths are now averaging 289 per day, down 11% from two weeks earlier.

- Moderna (MRNA, $129.99) released clinical trial results showing its two-strain vaccine booster increases immunity against the fast-spreading Omicron subvariants. In a request that regulators approve the use of the vaccine, the company argued that the higher level of protection compared with the company’s existing vaccine justified switching to the new booster, which could help prevent “a large rise in cases” in early autumn.