by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT] | PDF

Good morning and happy CPI day! We cover the data below, but the quick read is that prices rose less than expected, lifting equity futures, which were leaning higher before the report. Tropical Storm Nicholas has hit the Texas coast, dumping prodigious amounts of rain. The storm track is taking it toward Louisiana. Our coverage begins with the New York Fed’s inflation survey, followed by an update on the uranium market and Facebook (FB, USD, 376.51). Our regular coverage begins with China news. Bond market jitters continue. The international roundup is next; the center-left wins in Norway. We close with pandemic coverage.

NY Fed and Inflation: The New York FRB conducts a survey of consumer behavior and outlooks, and its recent polling on inflation expectations is sobering. The overall inflation expectation for one year out is 5.2%; the three-year rate is 4.0%. Older Americans (over 60) are most concerned, forecasting a 6.0% rate over the next 12 months. But even the under 40 bracket is looking for 4.5%. Check out the above link for the breakdown by education, age, and region. The bottom line for the Fed is that inflation expectations are rising, and the central bank’s only real tool to address it is to weaken aggregate demand, which we doubt it will do.

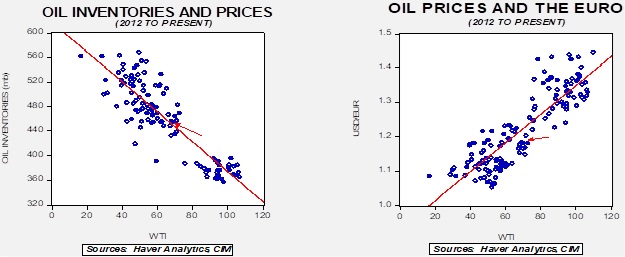

Uranium on a tear: We have been friendly to uranium on the idea that, eventually, it will become obvious that you can’t achieve a carbon-free energy sector without nuclear power. That doesn’t mean nuclear power isn’t without its externalities, but so does every other power source. The uranium market isn’t huge. Much of the production and consumption is tied to long-term contracts, meaning the spot market is even smaller than it looks. In such situations, a small amount of buying can lead to price spikes. Investor interest appears to be high, and that has sent prices up sharply. We don’t know how long it will last, but over the long run, we suspect prices will remain higher than seen in recent years.

Facebook (FB, USD, 376.51): In the spirit of Animal Farm, it turns out that all animals are equal, but some are more equal than others. A WSJ report reveals that the social media company does not screen all Facebook users the same.

China: Evergrande (EGRNF, USD, 0.46) remains in the news.

- The steady drip of bad news from the property developer Evergrande is now starting to become a broader problem. Until around 2015, China essentially prevented defaults. Investors tended to assume they wouldn’t occur and, thus, take excessive risk. But the Xi regime has changed the rules of the market, and the Evergrande situation could prove to be a serious test. We are seeing evidence of protests against the company, with investors demanding their money back, employees demanding their pay, and homeowners demanding their homes get built. The company is cautiously starting to outline a restructuring plan. It is offering investors some mix of cash, payables, and property. The CPC has shown limited tolerance for protests and civil unrest. Beijing will likely press for some sort of resolution, but it looks like there are not enough assets to make all creditors and shareholders whole. In one sense, allowing bankruptcy and restructuring will inject an element of hazard to investors, which isn’t a bad thing. However, the fallout could be difficult to manage.

- Blackstone (BX, USD, 129.21) dropped its plans to purchase Soho China (410, HKD, 2.20) due to concerns over a lengthy regulatory review. It may be a polite way of saying China was never going to approve the transaction. The owners of Soho China are under scrutiny regarding concerns they are dumping their properties in China to flee the country. In the current political environment in China, this is a problem. Shares in Soho China plunged on the news.

- The former head of the PBOC, Zhou Xiaochuan, criticized the venture capital industry for creating a “winner take all” environment in the digital economy. These comments dovetail with Beijing’s recent criticism of the “disorderly expansion of capital.” Zhou is an establishment figure in China, and his position is further evidence that the investment practice of funding firms with strong network effects may be under pressure in China. He also suggested that curbing tech monopolies would “ensure growth,”

- In related news, regulators have warned against tech giants blocking links to rival companies.

- Alibaba (BABA, USD, 165.41) has offered details on how it will spend its CNY 100 billion (USD 16 billion) “common prosperity fund.”

- Although it is being dubbed an “anti-fraud” app, a new app also appears to be designed to track Chinese users’ access to foreign financial news sites. If so, it would suggest that China continues to use the “great firewall” to control the news narrative.

- The SEC’s Gensler indicates Chinese firms listed in the U.S. will need to be audited. We suspect that won’t happen under General Secretary Xi.

International roundup: Labor wins in Norway, the Peronists don’t win in Argentina, and Lebanon gets aid.

- Norway’s Labor party and its allies look poised to take control of the government. Labor itself won 48 seats out of 169, over half needed to gain control of the legislature. The Center and the Socialist Left won 28 and 13 seats, respectively, giving it a majority of 89 seats. Most important for Norway’s oil and gas industry, the current coalition does not need the Greens to form a government. The Greens wanted to end exploration which, would have led to eventual declines in production.

- Meanwhile, the opposition won handily in primary elections in Argentina. Given recent polling, this outcome was not unexpected.

- Lebanon, which is near economic collapse, has received $1.135 billion in SDRs from the IMF. Although this won’t fix the country’s problems, it will likely buy the new government some time.

- Although the Nord Stream 2 pipeline is complete, it will be several weeks before gas will flow. The line still needs some final work, testing, and regulatory approval.

- Spain, dealing with rapidly rising electricity prices, has implemented a windfall profits tax.

- The leaders of the Quad—the U.S., Australia, Japan, and India—will meet in Washington on September 24th. This meeting will be the first one in person for this group. China views this arrangement as an alliance to contain China. We agree with Beijing on this one.

COVID-19: The number of reported cases is 225,359,152, with 4,641,746 fatalities. In the U.S., there are 41,223,105 confirmed cases with 662,252 deaths. For illustration purposes, the FT has created an interactive chart that allows one to compare cases across nations using similar scaling metrics. The FT has also issued an economic tracker that looks across countries with high-frequency data on various factors. The CDC reports that 456,755,755 doses of the vaccine have been distributed, with 380,831,725 doses injected. The number receiving at least one dose is 209,701,005, while the number receiving second doses, which would grant the highest level of immunity, is 178,982,950. For the population older than 18, 65.0% of the population has been vaccinated. The FT has a page on global vaccine distribution.

- The debate of booster shots is heating up. The Lancet’s most recent research suggests boosters are not needed at this time. However, the White House is pushing for boosters after promising them and is accusing the FDA and CDC of withholding data. To us, this looks like a classic case of a collision between politics and science. Science is a form of inquiry, and “settled science” means that the preponderance of opinion supports a certain point. Since science is inductive, the truths it unearths are always tentative. Politics, on the other hand, is about making decisions with available data. Conflicts are inevitable.

- There are inquiries about data procedures at the National Institutes of Health after genetic samples of COVID-19 were destroyed at the request of Chinese researchers. Even if this event is innocent, the action does not look good.

- There are new outbreaks of COVID-19 cases in China.