by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT] | PDF

Good morning, and happy Monday! In the wake of Friday’s rally, U.S. equity futures are mostly steady this morning. Our coverage begins with a look at the G-7 agreement to set a minimum corporate tax. Up next is the president’s trip to Europe. There were three major elections over the weekend; we look at the outcomes. Economics and markets are next, with a look at cryptocurrencies and Treasury Secretary Yellen’s comments about rising interest rates. China news is next. Technology news follows, and we close with pandemic coverage.

The G-7: Corporate taxes are an area of contention in public finance economics. Two broad theoretical problems are in play. First, there is the problem of incidence, which is the economic word for “who pays?” If firms were fully profit maximizers, corporate profits are paid by the firm. However, in real life, firms don’t always maximize profits in a given time frame. They may reduce profits today through research and development spending or by increasing worker training. If firms don’t always maximize profits, then the incidence may fall on consumers (via higher prices) or on workers (through lower wages). In practice, it appears that the corporate tax incidence eventually is paid by others, which has created a vocal group of economists who argue it should be abolished. That leads to the second issue, which is the question of ownership, or put another way, what is a corporation anyway? Legally, we treat a corporation as if it were a person, but that’s a bit silly. A corporation is more of a legal construct that someone owns. Since that owner almost certainly is a person, the earnings that corporation produces eventually go to that owner…who is also taxed as a person. Now, if there were no corporate tax, earnings could be retained indefinitely and no tax would ever be paid by a person, but, as we see with dividends, they are taxed twice in the U.S. In other words, the corporate tax often ends up being a second tax on an individual who is a beneficial owner.

Complicating matters further is the globalization of business. Firms have become remarkably adept at moving earnings to low-tax states and reducing the corporate tax. In the U.S., we see a “race to the bottom” on state and local taxes as these entities try to attract businesses to locate in a certain area. This activity occurs at the international level, too. A solution for state and local governments would be to agree to a minimum level of local and state taxes to remove the incentive for businesses to shop for lower taxes; this is also a solution at the international level. Over the weekend, the G-7[1] nations agreed on a minimum corporate tax rate of 15% and would tax them based on activity in each nation and not on where the profits are booked. Is this a big deal? Yes, but it’s not too big. None of the seven nations in this group is a tax haven, like Ireland, for example. Selling the idea within these nations won’t be easy, but it pales in the difficulties in expanding the minimum’s reach. France, Germany, and Italy would be on board with this idea, but other nations within the EU won’t. Broadening out to the OECD will be even more difficult. There have been proposals among U.S. state and local governments to do something similar, but the temptation to defect from the agreement to attract a business is hard to overcome. So, this is an important development, but it’s also too early to start expecting lower after-tax earnings from this deal.

Off to Europe: President Biden is making a trip to the EU this week. There is great fanfare about uniting the world’s democracies. However, the underlying reality is that Europe isn’t that important to the U.S. anymore (China is a much bigger issue), and if the U.S. is going to become a proper empire, it means we do less of the dirty work while making allies do more. The U.S. hegemonic model from the Cold War was designed to contain the Soviets, so we made it attractive to work with the U.S. by providing security for low cost and allowing nations to run large trade surpluses with America. Those days, regardless of who occupies the White House, are over, and the world will either (a) have a world without a hegemon, a G-0 world, which history says is a world at war, or (b) a more traditional hegemon that is disliked, feared, and obeyed. Our position is that option “a” is the more likely outcome, but we cannot say, with certainty, that a “b” outcome isn’t impossible. For Europe, which dominated the world for centuries, both outcomes are attractive. Either they will face the tender mercies of Russia and China on their own or be directed by the U.S. to do what Washington wants. Europe wants a return to the Cold War policies; that outcome isn’t politically feasible anymore in the U.S. We expect lofty sentiments, but the reality is that the EU will be spending more on defense, and it will again face the internal dissension within Europe on its place in the world.

Election special: Germany and Mexico held local elections, and Peru had its presidential runoff.

- Germany holds national elections in September, and with Merkel retiring, there is uncertainty about who will be in power in the wake of the vote. In the last local election before the national polls, voters in Saxony-Anhalt kept the CDU in power and reduced the influence of the AfD. This outcome was a boost for the incoming CDU leader Armin Laschet; he is considered a lackluster campaigner, leading to worries about his leadership going into September’s election. The win this weekend is good news for Laschet.

- AMLO’s coalition, Morena, appears to have maintained its majority in the legislature but lost its supermajority in the lower house, meaning AMLO will be less likely to make changes to Mexico’s constitution. Morena continues to dominate Mexico’s political situation, but the opposition was able to reduce AMLO’s power to some extent.

- The Peru outcome is uncertain at this time. Fujimori does hold a slim lead over Castillo, but it may be a few days before the outcome is determined. The differences are stark; Fujimori is seen as conservative and business-friendly, while Castillo wants to push a hard-left agenda.

Economics and policy: Yellen prepares the markets for tighter monetary policy, and cryptocurrencies continue to make news.

- Although Janet Yellen no longer runs the Fed, her perch as Treasury Secretary is high profile. She is usually painted as an uber-dove on policy, a characterization that isn’t really accurate. She pressed Greenspan to tighten policy in the late 1990s when the economy was strong. He demurred, arguing that productivity gains meant policy could remain easy. Instead, we view Yellen as more of a left-of-center orthodox economist who believes in pre-emption in terms of monetary policy and would not advocate MMT. Note that in her support of the administration’s spending, she is also pushing for higher taxes. Over the weekend, she made the argument that the Fed should support higher interest rates and inflation which would represent a “normalization” of the economy. We see her point but note this normalization would not be welcomed by the financial markets.

- One item to watch here is that it is not at all uncommon that when a party has been out of power, when they return to government, there is something of an “all-star team” of policy people waiting to fill roles. It is usually after a year or two a president begins to realize that he needs people to execute his ideas rather than to advise him on what to do. It will be interesting to see if Biden continues with Yellen or moves to someone less orthodox down the road.

- Cryptocurrencies are all the rage. They are great for journalists—they are obscure in their origin, and the volatility means that headlines are easy to find. But for investors, it’s caveat emptor. The FTC says that $80 billion has been lost by investors in scams, and, as we will discuss later this month in an upcoming WGR series, it is the payment choice for organized crime.

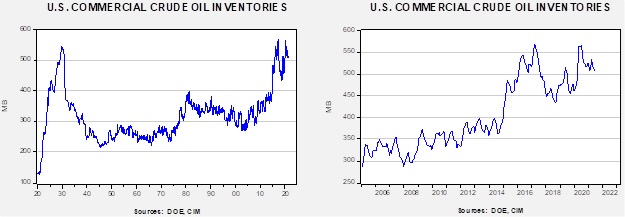

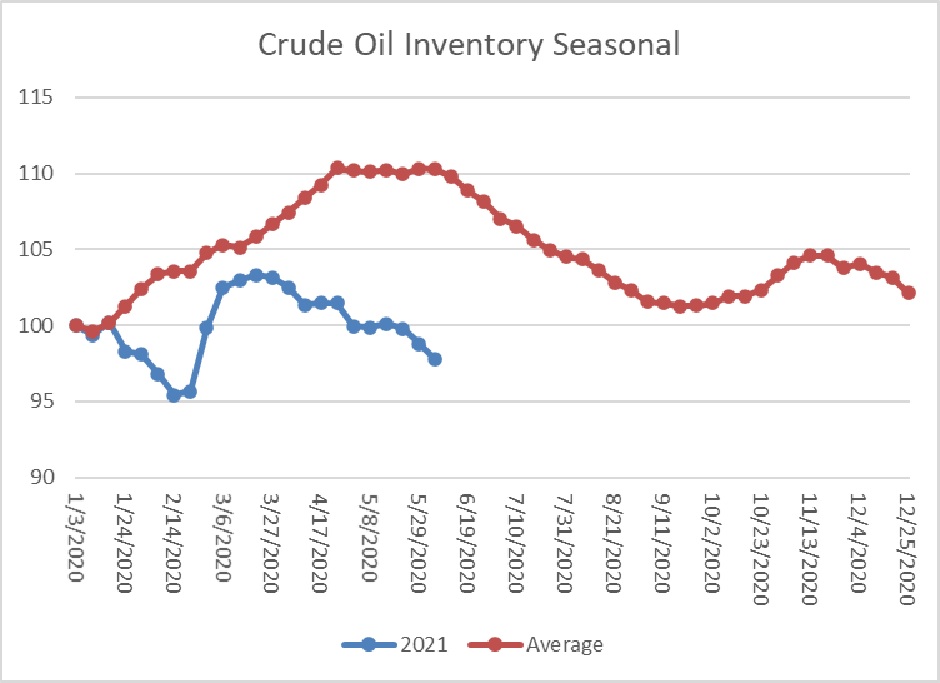

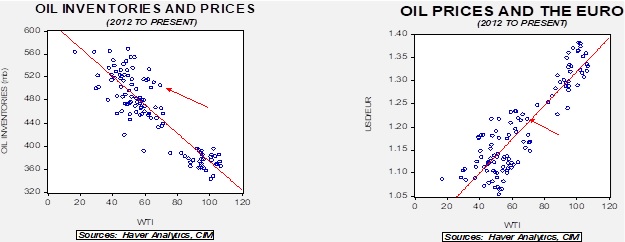

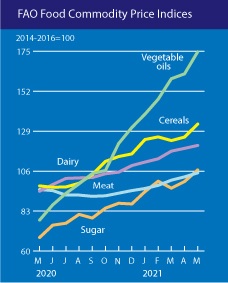

- We have been bullish on commodities as the world recovers from the pandemic. Grain prices have been soaring, and soybean oil, used for both cooking and in biofuels, is on a tear.

- Home prices are also strong, and price strength is spreading into modest homes and smaller towns.

- Semiconductor chip shortages will crimp auto supply until mid-2022.

- One factor roiling the labor markets is a growing reluctance to relocate. There is some evidence that the pandemic has caused some reconsideration of priorities and leading some workers to decide to stay put.

China: Biden continues some of Trump’s China policies, Hong Kong has changed, and Beijing is cracking down on tech.

- The media never seem to get the fact that policy is often shaped by circumstance. A president may want to change things, but the reality is that conditions restrict choices. As we noted above in the EU comments, Biden may be more polite to Europe than Trump, but the policy direction means that Europe can’t go back to the Cold War situation. China is a strategic competitor, and thus, there will be some level of consistency in policy. For example, the U.S. expanded its blacklist on Chinese companies that have ties to China’s military.

- For years, Hong Kong was seen as a capitalist haven in the Far East. As Deng moved to expand China’s economy, the former British colony became a bridge to the rapid growth in China that still offered the “comforts” of a Western legal system and the freedoms that come with it. That has all changed under Xi, and businesses are starting to realize that being in Hong Kong offers no special status.

- Technology firms are facing increased regulatory threats around the world. Their tendency toward monopoly market structures and their pervasive influence make them a target. Beijing is moving quickly to bring these firms to heel.

Technology: Google (GOOG, USD, 2451.76) agrees to a fine, and Apple (APPL, USD, 125.89) faces scrutiny.

COVID-19: The number of reported cases is 173,360,912 with 3,730,506 fatalities. In the U.S., there are 33,363,364 confirmed cases with 597,631 deaths For illustration purposes, the FT has created an interactive chart that allows one to compare cases across nations using similar scaling metrics. The FT has also issued an economic tracker that looks across countries with high-frequency data on various factors. The CDC reports that 371,520,735 doses of the vaccine have been distributed with 301,638,578 doses injected. The number receiving at least one dose is 170,833,221, while the number of second doses, which would grant the highest level of immunity, is 138,969,323. The FT has a page on global vaccine distribution.

View PDF

[1] U.S., U.K., Canada, France, Germany, Italy, and Japan.

(Source: Barchart.com)

(Source: Barchart.com)