by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] | PDF

We have published our latest Weekly Geopolitical Report, which is Part II of our two-part series on the Western Sahara. We also have several other recent multimedia offerings. There is a new chart book recapping the recent changes we made to our Asset Allocation portfolios. Here is the latest Confluence of Ideas podcast. A new Asset Allocation Weekly, chart book, and podcast are also available. This week’s Weekly Energy Update is available. You can find all this research and more on our website.

We open today’s Comment with a quick review of key international news, including an important overview regarding how U.S. firms see their business in China developing. Then, we focus on the latest developments in the coronavirus pandemic, where President Biden’s $1.9 trillion “American Rescue Plan” looks increasingly certain to become law this week. That’s giving a boost to U.S. stocks in general today. Just as important, the bond market appears to be showing signs of nascent stabilization, perhaps because some bond buyers are reportedly taking advantage of the recent runup in yields. If it lasts, the new buying could potentially put a cap on yields, which helps explain why technology stocks are jumping so far this morning.

United States-China: A membership survey by the U.S. Chamber of Commerce in China showed that only 56% of respondents reported earning a profit in the country last year. About 20% suffered losses, up from 11% reporting losses in 2019. Two-thirds of U.S. companies said their revenue in China rose or remained stable in 2020—below the 79% that reported increasing or steady sales in last year’s survey.

United Kingdom-European Union: British business leaders are already complaining that the government’s new minister for EU relations, Lord David Frost, is too abrasive concerning his dealings with Brussels, and he is threatening to undermine the U.K.-EU trade relationship.

Germany: Ahead of critical state elections next weekend, Chancellor Merkel’s Christian Democratic Union is being pummeled by a scandal in which two CDU lawmakers earned substantial commissions on deals to procure urgently needed masks during the first wave of the coronavirus pandemic. Both lawmakers have been forced to resign, but the scandal will make it even more difficult for the CDU to win in states like Baden-Württemberg and Rhineland-Palatinate. It also raises questions about the leadership of new CDU chief Armin Laschet.

Brazil: A supreme court judge has annulled the graft convictions of former President Luiz Inácio Lula da Silva, restoring the left-wing leader’s political rights ahead of elections next year. If the decision stands, it could set the stage for an election battle between Lula da Silva and incumbent President Jair Bolsonaro, a right-wing populist and one of the most strident critics of Lula da Silva and his left-wing Workers’ party, also known as PT. The potential political uncertainty is likely to be negative for Brazilian assets.

COVID-19: Official data show confirmed cases have risen to 117,250,914 worldwide, with 2,604,123 deaths. In the United States, confirmed cases rose to 29,045,983, with 525,904 deaths. Vaccine doses delivered in the U.S. now total 116,378,615, while the number of people who have received at least their first shot totals 60,005,231. Finally, here is the interactive chart from the Financial Times that allows you to compare cases and deaths among countries, scaled by population.

Virology

- Newly confirmed U.S infections topped 50,000 yesterday, although the new case count remained far below the figure reached at the beginning of the year. Perhaps more importantly, new deaths related to the virus totaled just 719. Vaccinations against the disease also continue apace, as 18.1% of the U.S. population has now received at least one shot.

- In an update to its pandemic safety guidelines, the CDC recommends that people who are fully vaccinated should continue to use facemasks and practice social distancing when around non-vaccinated people. However, they can dispense with those precautions when around other fully vaccinated people. Under the new guidelines, vaccinated individuals will not need to quarantine or receive a COVID-19 test after being exposed to the virus if they have no symptoms.

- The organizing committee for the Summer Olympic Games in Tokyo has decided to ban spectators from the ceremony launching the Olympic torch rely on March 25. The committee will decide sometime in mid-March whether it will ban overseas spectators from the Games themselves, which are scheduled to open July 23.

Economic and Financial Market Impacts

- New polling by Axios/Ipsos indicates many people may be slow to return to normal life even after getting vaccinated. Just 7% of respondents said they plan to stop wearing masks in public after receiving their shots, and only 13% said they plan to stop social distancing. 81% said they would continue to wear masks, and 66% said they would continue to social distance until the pandemic ends. That raises a risk that the economic rebound this year could potentially be a bit more sluggish than currently expected.

U.S. Policy Response

- Several prominent Democrats in the House of Representatives signaled they would approve President Biden’s $1.9 trillion pandemic relief package when it comes up for a final vote this week, despite some provisions being watered down in the Senate.

- That means the bill, formally designated as the “American Rescue Plan,” is increasingly certain to be passed into law, most likely on Tuesday or Wednesday. This Wall Street Journal article provides an overview of the bill’s major provisions.

- Not only would the new stimulus provide a jolt to U.S. economic growth in 2021, but the OECD today said it would boost global growth by an additional 1%. In updated forecasts, the OECD now expects global GDP to rise by 5.6% this year, up from a forecast of 4.2% last November. There is one potential downside: The OECD also warns that the rise in U.S. government bond yields in response to higher growth and inflation expectations could spark capital flight from emerging economies, where vaccine campaigns have barely begun and whose economic recovery is expected to take longer.

- The Federal Reserve yesterday said it would allow most of its remaining emergency asset purchase programs from last spring to expire as scheduled at the end of the month. The plans include the Commercial Paper Funding Facility, the Money Market Mutual Fund Liquidity Facility, and the Primary Dealer Credit Facility. According to the Fed, the programs are now seldom used.

- Several other major programs expired at the end of December, including the Corporate Credit Facilities, the Municipal Liquidity Fund, and the Term Asset-Backed Securities Loan Fund.

- The Fed said it would renew the Paycheck Protection Program Liquidity Facility, which extends credit to eligible financial institutions that originate PPP loans, through to the end of June.

- Even though many of the Fed’s emergency programs are going away, the ultra-low fed funds benchmark interest rate and the Fed’s broader asset purchase program are keeping monetary policy extraordinarily loose. This should lend additional support to risk assets on top of the strong forthcoming fiscal stimulus and the impending reopening of much of the economy.

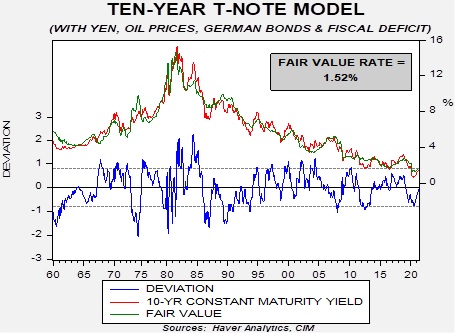

- Still, a key question is whether the Fed will extend an emergency policy exempting cash and Treasury securities from banks’ supplementary leverage ratios (SLRs). Some observers argue that the recent runup in yields stemmed, at least in part, from major banks running up against their SLR limits and not being able to buy more Treasuries without raising new capital or scaling back planned dividends. Extending the exemption past its planned end on March 31 could give banks more capacity to gather deposits and buy government bonds, which could help calm the bond market.

Foreign Policy Response

- Despite European Central Bank chief Lagarde’s statement of concern over rising bond yields, new data show the ECB slowed its bond purchases in recent weeks, even as those yields spiked. Regardless of Lagarde’s rhetoric, the data suggest that the ECB, like the Fed, is reluctant to actually intervene to cap yields just yet. More detail about her views could come out in Lagarde’s press conference after the ECB’s March policy meeting on Thursday.