by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] | PDF

Our Comment today opens with a short discussion of what to expect from today’s monetary policy decision from the Federal Reserve. In short, we expect no substantive change in policy. We then discuss a range of news stories from abroad, including signs of increased domestic tension within Russia and international tension between the EU and the U.K. As always, we wrap up with a discussion of the latest coronavirus news.

United States: Officials at the Fed are completing their latest policymaking meeting today, but no substantive changes are expected in either its benchmark interest rate or its asset purchasing programs. That’s especially true given that the recent upswing in longer-term yields has come to a halt amid strong demand for Treasury obligations. That will likely forestall any immediate need for the Fed to impose “yield curve control” over longer-term yields. The key focus for investors regarding the meeting today will likely be how the officials assess economic conditions and prospects going forward.

United States-Russia: The White House said President Biden held his first call as president with Russian President Putin and raised concerns about issues including the detaining of opposition leader Alexei Navalny, Russian threats to Ukrainian sovereignty, the massive SolarWinds computer hack, and reports of Russia offering bounties on U.S. troops. A readout on the call from the Russian government stated it was “open and businesslike,” suggesting some tough positioning on both sides.

Russia: In a sign that President Putin has become concerned about the large pro-Navalny demonstrations across Russia last weekend and the Navalny organization’s video exposé of a massive palace built for Putin using public funds, the president admitted at an event yesterday that he had seen part of the exposé and insisted it was false. At the same time, Russian state television ran several lengthy attacks accusing Navalny of being a corrupt, failed politician working on behalf of western intelligence agencies. The attacks underscore a sense of irritation and worry in the Kremlin at Navalny’s ability to harness national public anger while representing the latest in a series of missteps by Putin’s administration in its attempts to sideline the activist.

EU-U.K.: Just when we all thought the whole Brexit saga was over, the U.K. has sparked a row by refusing to grant full diplomatic status to the EU ambassador overseeing the post-Brexit trade deal signed late last year. British Foreign Secretary Raab insists that the EU official should be regarded as representing merely an “international organization,” but the EU is insisting that the official be recognized as representing a sovereign state, as it is by all other countries with which it has diplomatic ties.

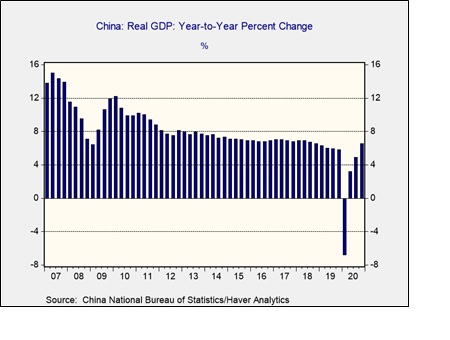

China: Jack Ma’s fintech giant Ant Group, which Beijing has clamped down on because of Ma’s pushback against government regulation, has reportedly caved to government pressure to become a holding company regulated by the Chinese central bank. Besides signaling the government’s intention to maintain control over the private sector, the move will force Ant to meet higher capital standards than would otherwise be the case. Since the news will reinforce perceptions of increasing state interference in the Chinese private sector, going forward, it will probably be a negative for Chinese equities.

China-Hong Kong: As more financial services firms leave Hong Kong in response to China’s clampdown on it and implementation of its new security law, officials are worried about the city’s future as a financial hub and are putting executives through what appear to be “exit interviews.” Hedge fund managers who have been subjected to the process say they were asked for a full picture of the decision-making process behind the moves and the significance of the timing. The grilling highlights the risk that China’s greater control over Hong Kong will probably drive a lot of its financial services industry to other Asian locales, like Tokyo or Singapore, potentially creating investment opportunities there.

COVID-19: Official data show confirmed cases have risen to 100,381,254 worldwide, with 2,160,783 deaths. In the United States, confirmed cases rose to 25,445,699, with 425,257 deaths. Vaccine doses distributed in the U.S. now total 44,394,075, while the number of people who have received at least their first shot totals 19,902,237. Finally, here is the interactive chart from the Financial Times that allows you to compare cases and deaths among countries, scaled by population.

Virology

- Newly confirmed U.S infections totaled approximately 142,000 yesterday, marking their tenth straight day under 200,000. Hospitalizations related to the virus fell to below 109,000 for the first time since December 12. Of those hospitalized, the number in intensive care fell to just above 20,000. On a less positive note, however, the number of virus-related deaths rebounded to almost 4,000.

- The Biden administration said it will boost the supply of vaccines sent to states by about 16% for the next three weeks and purchase enough additional doses to vaccinate most of the U.S. population with a two-dose regimen by the end of the summer. The updated plan would involve purchasing an additional 100 million doses for each of the vaccines developed by Pfizer (PFE, 37.31) and Moderna (MRNA, 151.85).

- The state government in California said it will change the way it prioritizes who gets vaccine doses, creating a statewide standard and basing the intermediate stages of its vaccination program on age alone. The first two groups to be vaccinated will continue to be health-care workers and residents of long-term care facilities, followed by residents aged 65 years and older, education and child-care workers, emergency services personnel, and food and agriculture workers.

- Despite surging cases in Japan, the government is insisting on Japan-specific clinical trials before approving the various vaccines already in use abroad. The requirement for Japanese clinical trials means the earliest that Japan can start mass vaccinations would be late February. Separately, Prime Minister Suga said he will decide next week regarding whether to extend the pandemic state of emergency, currently planned to expire on February 7, in Tokyo and other areas.

- Even with the rollout of vaccines, scientists say infection prevention protocols will still be needed for months. Now that we have a year’s worth of experience with the virus, scientists are reaching a consensus on which protocols are most important: mask-wearing, social distancing, and maintaining good air circulation are at the top of the list.

Economic and Political Impacts

- In India, the recent loosening of pandemic restrictions is not yet prompting any rebound in consumer spending, as consumers continue to hold on to their savings out of fear for the future. The development highlights how the pandemic could leave more lasting economic scars on less developed countries that couldn’t afford massive fiscal and monetary support measures like those in the U.S.

U.S. Policy Response

- Some small businesses trying to access second loans from the reopened Payroll Protection Program are getting rejected because of flags on their files related to problems with their initial applications. The flags relate to anything from clerical errors to indicators of fraud. In order to get more loans in place, the SBA has announced it will issue new guidelines to make sure the flags can more easily be overcome.

Foreign Policy Response

- In an interview with the Financial Times, French Finance Minister Le Maire called on the EU to overcome bureaucratic obstacles slowing the disbursal of its €750 billion recovery fund to member states. He also warned that overcoming the pandemic would probably require re-evaluating eurozone fiscal constraints.