The U.S. and North Korea have had a difficult history. The two countries were the primary combatants during the Korean War and still have not established a peace treaty. However, in the late 1970s, the Kim regime and the Carter administration considered normalizing relations. Carter’s national security team concluded there was little value in talking directly to North Korea[1] and, ever since, the U.S. has essentially “outsourced” North Korea to China.[2]

On its face, this decision makes sense. China is critically important to North Korea’s economy; more than 80% of North Korea’s foreign trade is with China. Mao described relations between the two countries as “close as lips and teeth.” However, relations are more than just economics. A review of historical relations between China and North Korea indicates a deep animosity that inhibits China’s ability to control the policies and decisions in Pyongyang.

In Part I of this report, we will begin our study of the historical relationship between North Korea and China, including a review of the Minsaengdan Incident and a broad examination of the Korean War. Part II will complete the analysis of the war, discuss the Kim regime’s autarkic policy of Juche and outline the impact of the Cultural Revolution on North Korean/Chinese relations. Part III will cover the controversy surrounding North Korea’s Dynastic Succession, the end of the Cold War and the ideological issues with Deng Xiaoping. Finally, we will recap this history and its impact on American policy toward the Democratic People’s Republic of Korea (DPRK) along with market ramifications.

[1] Carter was worried about being seen as weak by GOP critics. Creekmore, M., Jr. (2006). A Moment of Crisis: Jimmy Carter, The Power of a Peacemaker, and North Korea’s Nuclear Ambitions (chapter 7). New York, NY: Perseus Books Group.

[Posted: 9:30 AM EDT] Although U.S. financial markets are quiet, there is a lot going on. Here’s what we are watching this morning:

War in Iraq? Iraqi troops have taken a refinery and captured oil fields surrounding the city of Kirkuk. So far, only Iraqi regular army troops have been involved; the Iranian-dominated Iraqi Shiite militias have reportedly not been part of the action. Kurdish Peshmerga forces have withdrawn, avoiding a fight with Iraqi forces. Reuters[1] is reporting that General Qassem Soleimani, a key leader of the Iranian Republican Guard Corps (IRGC), has arrived in Kurdistan for talks. Soleimani is a somewhat shadowy figure in the IRGC but is considered to be the mastermind behind many of Iran’s tactics in the region. His presence there suggests Tehran is trying to contain the situation and prevent a wider war. To some extent, the tensions in Kurdistan are part of the collapse of IS. There is a power vacuum in western Iraq and eastern Syria; IS was the first to fill it, but it won’t be the last, and the process of determining who is in control will likely be difficult and lead to constant conflict. Oil prices lifted on the news.

A deadline for Catalonia: Catalan leaders are trying to support indigenous independence while avoiding a violent crackdown from Madrid. PM Rajoy has given Catalonia until Thursday to say, yes or no, whether independence was declared. If it was, look for a violent reaction from Spain. EU Commission President Juncker indicated today that he regrets that both parties in Spain didn’t heed his advice to talk sooner but said the EU would not mediate the crisis. Catalan leaders are stuck; if they back down from independence, they will likely lose their positions and more radical elements could replace them. If they declare independence, they will meet an ugly, aggressive response from Rajoy. So far, the EUR and Spanish debt have shown little signs of stress.

Austria moves right: As we noted last Friday, the Austrian vote went as expected, with the center-right People’s Party winning a plurality, making Sebastian Kurz the youngest leader of a major nation in the world. Kurz has moved the previously staid People’s Party into a more populist, right-wing party and has energized it with social media. He ran on an anti-immigration platform and will likely team up with the right-wing, populist Freedom Party. Although the general trend has been for populists to underperform in elections this year, as seen in France and the Netherlands, they have clearly done better in Germany and Austria. Populism remains a potent force in the West.

NAFTA worries: There are growing worries that the Trump administration will scuttle the agreement. There is talk of higher content rules for products (which would reduce imports of parts from Mexico and Canada) and sunset rules that would require renegotiation every five years. The former might be workable but the latter essentially kills the deal. Trade law changes business infrastructure; if it is open to major changes every five years then firms won’t make the investments into international supply chains and will simply produce more at home. Worries are starting to show up in the forex markets.

(Source: Bloomberg)

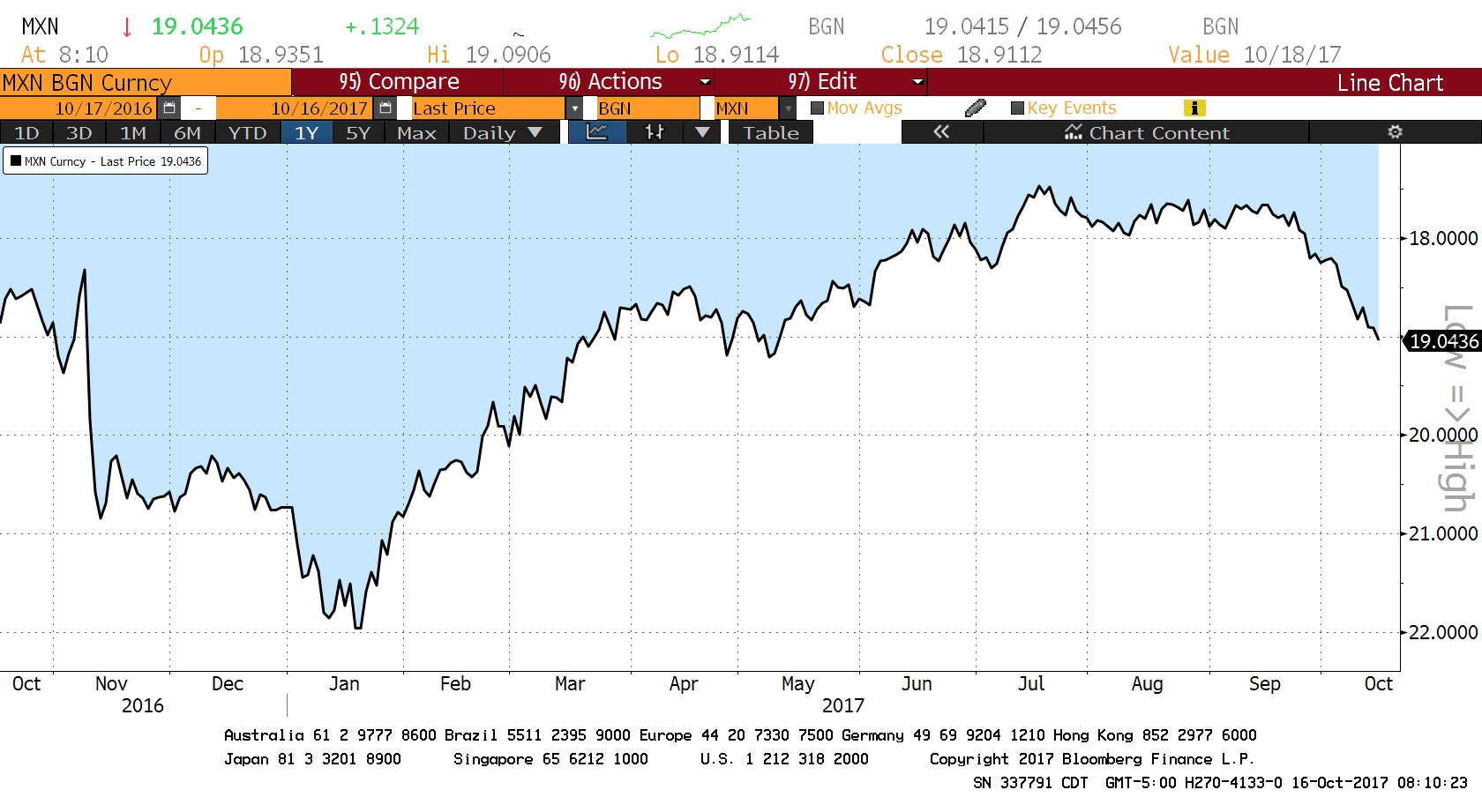

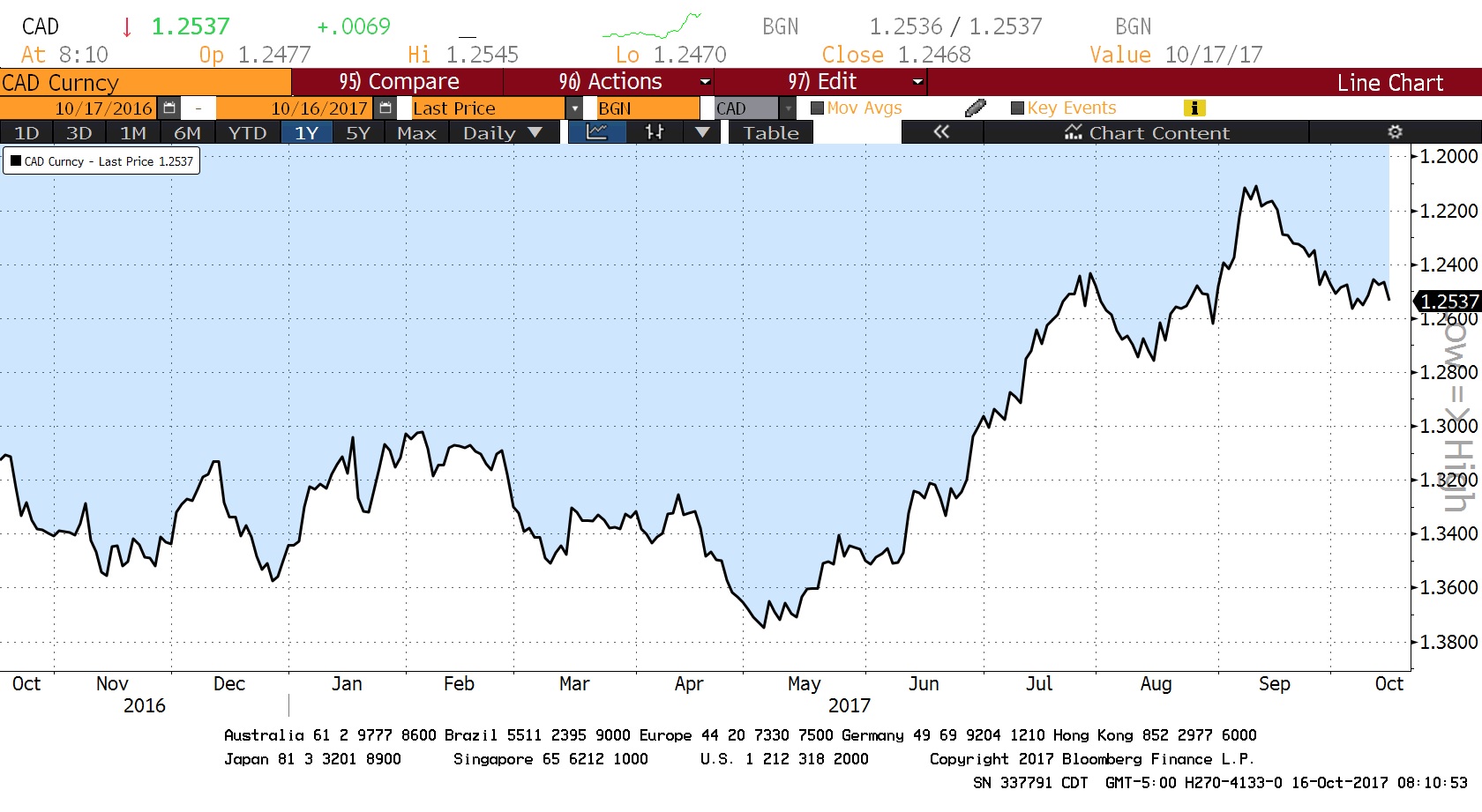

Concerns are clearly reflected in the MXN/USD (Mexican peso) exchange rate. This is the number of MXN per USD on an inverted scale. The MXN fell sharply after the election of President Trump but then the currency recovered on hopes that Trump, for all his rhetoric, would turn out to be a typical free-trade Republican. Note that the MXN has been weakening steadily since the middle of last month, reflecting worries about NAFTA. A somewhat less clear picture emerges on the CAD/USD (Canadian dollar) exchange rate.

(Source: Bloomberg)

Although the CAD didn’t weaken after the election (it was already quite weak), it rallied from May to September after the Bank of Canada raised rates. We have seen the currency weaken as NAFTA talks have deteriorated.

Yellen at the G-30: The G-30 is a group of finance officials from the industrialized nations. They met last weekend as part of the IMF meetings. Yellen reiterated her defense of the Phillips Curve and indicated that rates would continue to rise.

A worry for Turkey? A series of wiretaps suggests that PM (now President) Erdogan may have facilitated a violation of sanctions on Iran with gold for natural gas swaps in 2013.[2] The Turkish president has called the transcripts and tapes a fabrication but U.S. prosecutors think Turkey may have violated international sanctions on Iran. This case is damaging already strained relations with Turkey.

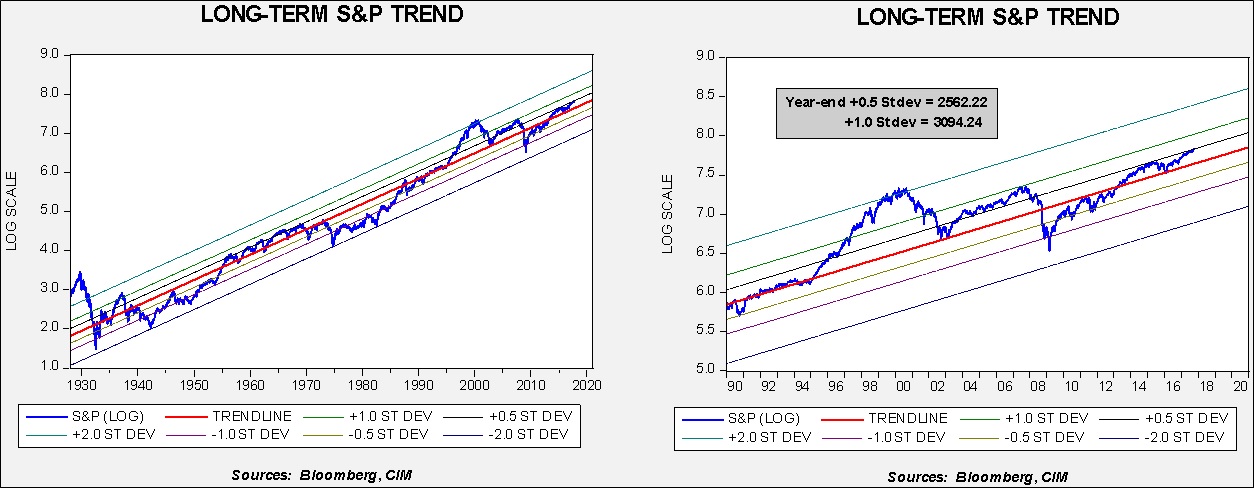

With the S&P making new highs almost daily, it is probably a good time to look at long-term trends to build some parameters.

This is a simple trend chart of the S&P 500 Index. We have log-transformed the weekly Friday closes of the index data and regressed it against a time trend. The chart on the left shows the index from 1929 while the chart on the right shows the index from 1990 (same regression trend lines for both charts).

Equities clearly trend higher over time. The yearly trend shows an average return for the S&P 500 Index of just over 6%. However, as the charts show, there is a fair degree of variation over time. The trend data shows that two standard errors above the trend is a dangerous area. One standard error above the trend is a concern. We are currently just below one-half standard error above the trend. That level by itself isn’t a big worry. In the 1950s into the early 1970s, we saw the index vacillate between the trend and one standard error above trend. These are not inconsequential market moves; in the current context, the trend line for the S&P 500 Index is 2090.26, meaning a pullback from current levels to the trend line would be a decline of about 17.6%.

Simply put, barring a recession or geopolitical event, equities are not seriously extended on a trend basis. We also note that the last two bear markets dropped a full two standard errors from peak to trough. The bear market that began in 2000 fell from two standard errors above the trend to the trend line (the bold red line on the chart), and the 2008 bear market ran from one standard error above the trend to one standard error below. Thus, a recession-triggered bear market would be a significant market event.

So, what does this tell us? Although there is a rather elevated sense of concern among investors, overall, the path of least resistance is to grind higher. Equities are not cheap but alternatives are even more expensive. The other insight this research offers is that a “melt-up” would take us well above 3000. If investors were to become “irrationally exuberant” we would expect a move to this level. At this point, there appears to be enough caution to prevent that from occurring. However, if a dovish Fed chair is nominated or a major tax cut appears likely to pass, a rise to these levels might be triggered. A recession is a clear worry; falling to one standard error below the trend line, which would be a drop of lesser magnitude than normal, would be to 1454.81 by year’s end. Obviously, because the trend line moves higher over time, the longer it takes to have a correction, the higher the expected bottom. For now, equities, based on this analysis, are not at levels that would usually signal a major bear market. At the same time, this doesn’t mean that there are no risks. It just means that, in terms of trend, we are not at extremes.

[Posted: 9:30 AM EDT] Markets are quiet again this morning; we are seeing the dollar weaken a bit and bonds rally on the weaker than forecast CPI data. On the other hand, retail sales were strong, although some of that is coming from hurricane distortion. Here is what we are following this morning:

ECB—less but longer: Reuters[1] is reporting that ECB policymakers have agreed on a plan to begin tapering. According to reports, the bank will extend the stimulus program by nine months but bond buying will be reduced to a range of €25 bn to €40 bn, down from the current €60 bn. The EUR eased modestly on the news. One of the problems is that the ECB is running out of eligible bonds to purchase so it needed to reduce its buying levels. At the same time, if this action is taken, the ECB is signaling its desire to remain accommodative. We view this action as modestly bearish for the EUR.

Tensions rise in Iraq: Iraqi forces are moving into the Kirkuk region, an area claimed by the Kurds. According to reports, Kurdish forces are withdrawing in front of the Iraqi deployment. Kirkuk is a key city in northern Iraq; both Kurds and Arabs see it as theirs (and both have controlled the town during various periods in history). It is also an important oil city. If open fighting develops, we would expect a disruption in oil flows and potentially higher prices.

Saudis buying Russian arms: Reuters[2] is reporting that Russia and Saudi Arabia are nearing a deal in which the latter will purchase the S-400 air defense system from Russia. This is a sophisticated air defense system, considered one of the best in the world. In fact, it seems odd the Saudis would need such a sophisticated air defense system because it isn’t obvious they face that sort of threat. We suspect this is a gesture of goodwill and a signal of deepening cooperation between Russia and the kingdom. Although the Trump administration has been working to improve relations with Saudi Arabia, it’s no secret that U.S. geopolitical interest in the region has lessened with the end of the Cold War and the advent of shale oil. We would expect continued cooperation between the two states as Saudi Arabia adjusts policy to emerging U.S. actions.

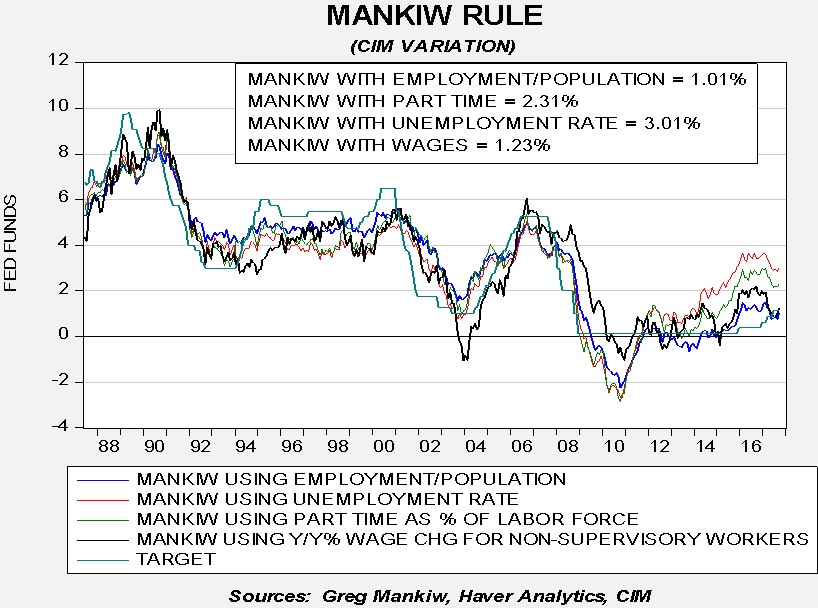

Fed policy: With the release of the CPI data we can update the Mankiw models. The Mankiw rule models attempt to determine the neutral rate for fed funds, which is a rate that is neither accommodative nor stimulative. Mankiw’s model is a variation of the Taylor Rule. The latter measures the neutral rate using core CPI and the difference between GDP and potential GDP, which is an estimate of slack in the economy. Potential GDP cannot be directly observed, only estimated. To overcome this problem, Mankiw used the unemployment rate as a proxy for economic slack. We have created four versions of the rule, one that follows the original construction by using the unemployment rate as a measure of slack, a second that uses the employment/population ratio, a third using involuntary part-time workers as a percentage of the total labor force and a fourth using yearly wage growth for non-supervisory workers.

Using the unemployment rate, the neutral rate is now 3.01%. Using the employment/population ratio, the neutral rate is 1.01%. Using involuntary part-time employment, the neutral rate is 2.31%. Using wage growth for non-supervisory workers, the neutral rate is 1.23%. The improved labor market data has lifted each model’s neutral rate calculation by 15 bps to 25 bps, putting all but the employment/population ratio variant below the current target.

Although the core rate rose less than forecast, we suspect there is enough support for a December hike to keep the likelihood of a move high. Fed funds futures still put the odds at 78% for an increase.

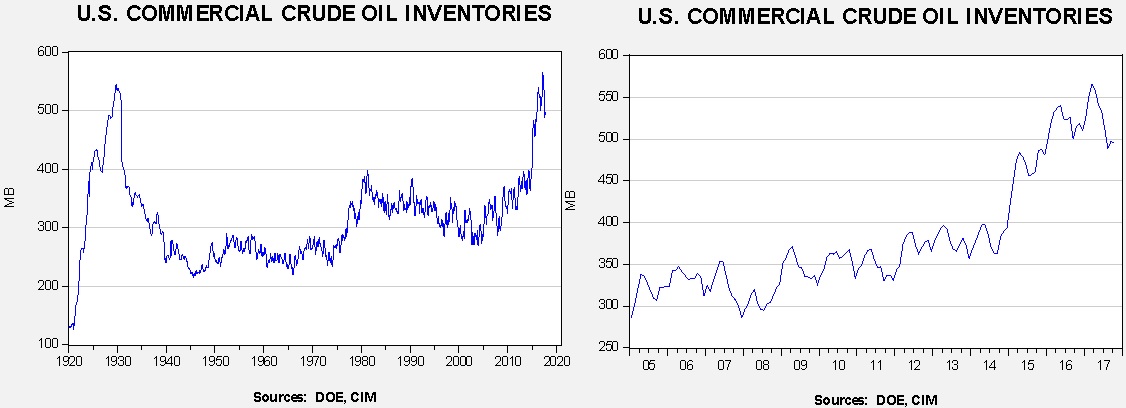

Energy recap: U.S. crude oil inventories fell 2.8 mb compared to market expectations of a 2.0 mb increase.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but have declined. The impact of Hurricane Harvey is diminishing as refinery operations recover. We also note the SPR fell by 1.8 mb, meaning the total draw was 4.6 mb.

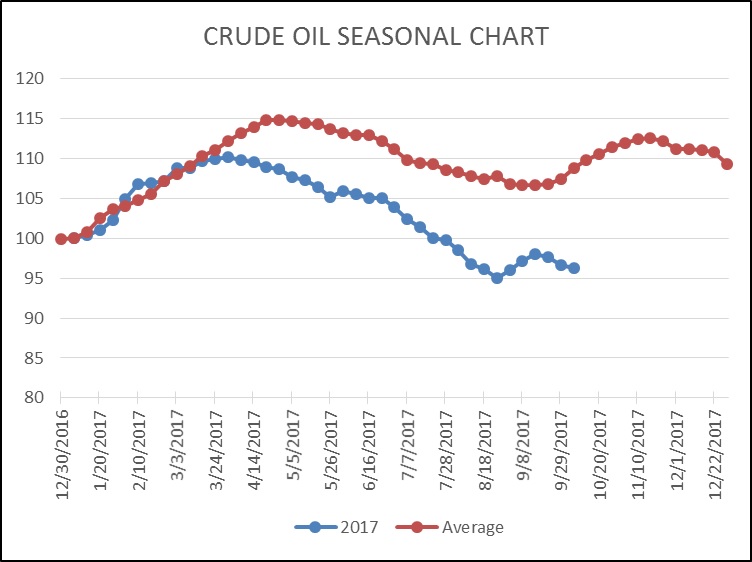

As the seasonal chart below shows, inventories fell this week. It appears we have started the inventory rebuild period sooner than normal this year due to the hurricanes. However, over the past two weeks, inventories have declined, which is a modest surprise based on the seasonal pattern.

(Source: DOE, CIM)(Source: DOE, CIM)

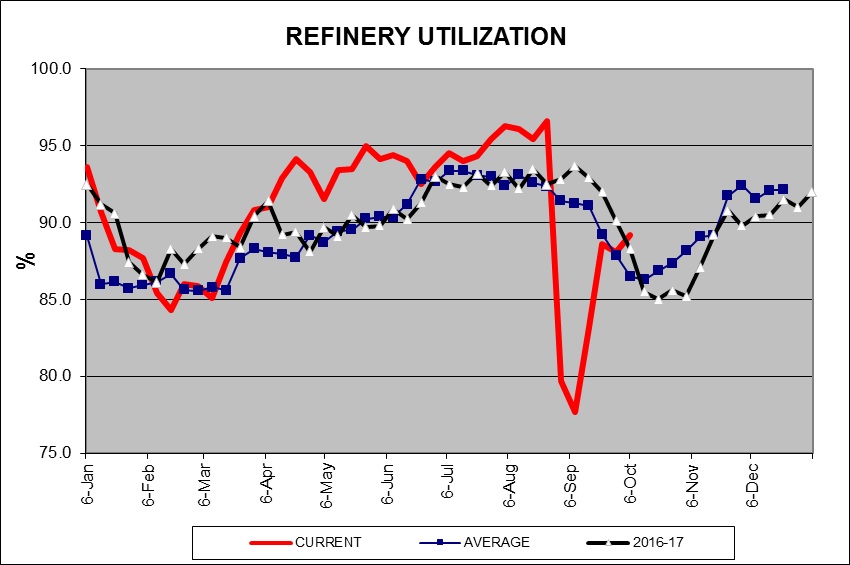

Refinery operations unexpectedly rose last week, which is a divergence from seasonal norms. Strong product demand and attractive refining margins are supporting strong utilization. The seasonal trough usually occurs next week; this week’s activity suggests that the maintenance season may be concluding early, which is bullish for oil prices.

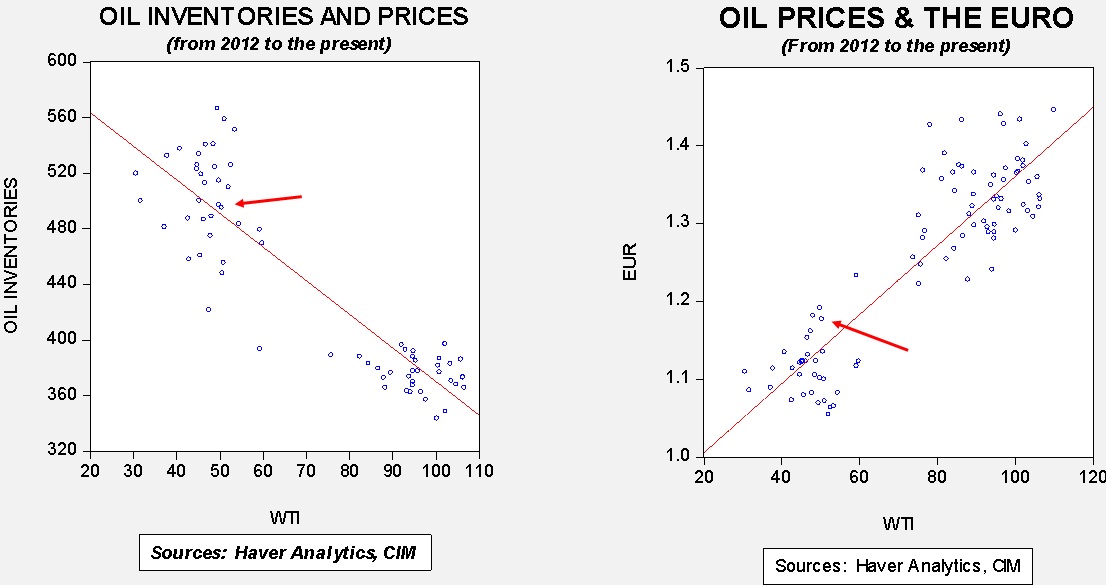

Based on inventories alone, oil prices are undervalued with the fair value price of $52.79. Meanwhile, the EUR/WTI model generates a fair value of $63.15. Together (which is a more sound methodology), fair value is $59.27, meaning that current prices are well below fair value. For the past few months, the oil market has not fully accounted for dollar weakness. If the oil market begins to recognize the dollar’s weakness, a broader rally in oil is possible.

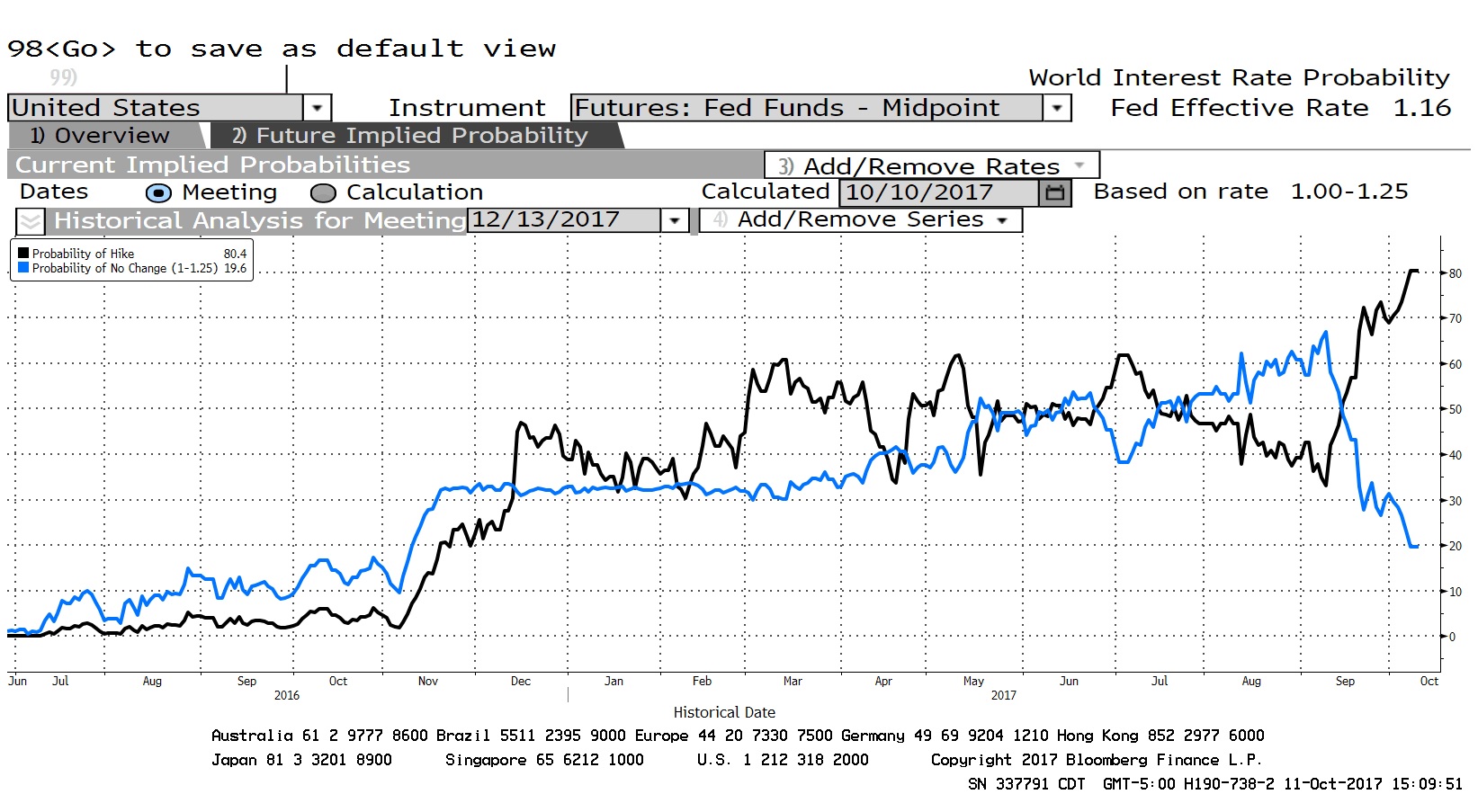

Fed minutes: The Fed minutes didn’t have a lot of surprises; we would characterize them as modestly dovish. Going off the terms used, “several” members were uncertain about inflation and wanted more data to improve their confidence, while “a few” believed that additional increases should be delayed. On the other hand, “many” thought another increase in the target before year’s end was warranted. That would suggest a rate hike in December is probably likely, but the decision may not be as unanimous as the market seems to think. Here are the current odds of a December hike in fed funds futures.

(Source: Bloomberg)

Current expectations call for an 80% probability of a December hike. The odds didn’t decline after the minutes were released.

The Chair race: Politico[1] is reporting that Treasury Secretary Mnuchin is promoting Jerome Powell for the Fed chair job. The secretary has worked with him on issues in the past and sees him as a safe pick that he will have some influence over. At this point, we believe the two front-runners are Powell and Kevin Warsh and, of these two, we would wager that Warsh gets the nod. However, Mr. Trump has a history of surprises. Although his name isn’t on any lists, we would not be shocked to see the president appoint an überdove like Minneapolis FRB President Kashkari. Kashkari is a Republican, which would make him acceptable to the GOP establishment. President Trump has also indicated he prefers low interest rates. We think Warsh is the front-runner because he will likely be beholden to the White House. The president’s comments suggest he may be more Nixonian in his stance toward the U.S. central bank and, if so, it would be dollar bearish.

Brexit talks stall: EU Chief Negotiator Barnier indicated this morning that the two sides have not made any “great steps forward” and that talks are “deadlocked.” Britain wants talks to shift to trade, but the EU wants the U.K. to inform the EU what it intends to pay to honor its EU commitments as the price of exit. Naturally, the May government has no interest in spelling out the costs but it appears that the EU won’t negotiate on trade until the U.K. makes an offer. Although talks are not doomed, there was some market impact from the announcement of a deadlock.

(Source: Bloomberg)

The GBP tumbled on the deadlock news but has started to recover.

Is NAFTA in trouble? Although negotiations continue, reports indicate that talks are contentious and negotiators are struggling to save the agreement. The impact of a repeal would be significant. U.S. agricultural exports would be harmed; Mexican tariffs on agricultural goods are steep and thus U.S. exports of grain and meat would likely decline. U.S. manufacturing is deeply integrated with Canada and Mexico, so production dislocations could be significant if trade flows are disrupted. For example, if trade barriers prevent auto parts from flowing across borders, auto production could cease for a period until new arrangements are created. More than 310 state and local Chambers of Commerce have sent letters to the White House urging the president to keep the U.S. in NAFTA. On the other hand, leaders of the AFL-CIO are supportive of the president’s efforts. Although we generally expect inflation to remain low, our position is that mild inflation is mostly a function of globalization and deregulation. If either is disrupted, supply constraints and higher prices will result. If such an outcome accelerates, it will have a significantly negative effect on financial markets. Inflation lifts interest rates and lowers P/Es. It is quite possible that NAFTA falls and is followed up with bilateral agreements that mimic NAFTA. However, the shift would not be frictionless and, in the interim, an inflation scare could prompt tighter monetary policy and increase the odds of recession. We are watching this issue closely.

Austrian elections: If current polls are correct, Austrian voters are going to side with the center-right People’s Party and its young leader, Sebastian Kurz. At 31, he would be the youngest head of government in the world. Usually, Austrian governments are grand coalitions of center-left and center-right parties. However, Kurz is expected to form a government with the xenophobic Freedom Party. Kurz has tried to limit the number of asylum seekers in Austria, opposing the German refugee policy. The anti-immigrant policy has been popular; when Kurz became party leader, People’s Party polling rose 10%. One of the other interesting elements of this election is that consultants for the Social Democrats apparently made fake Facebook (FB, 172.74) pages that purported to be from racist groups suggesting Kurz planned to open Austria’s borders at the behest of George Soros. The campaign appears to be rather nasty by European standards but, in the end, Austria appears to be turning rightward which will raise worries for Germany and France.

In my last letter I wrote of the tendency of investors to think of the economy and the markets as linear phenomena, rather than cyclical phenomena. In other words, an inclination to think that a good economy will continue its upward path forever unless some villain intercedes and causes a recession. However, at Confluence we believe that both the economy and markets are cyclical because they are the products of human behavior, which always tend toward extremes, extremes which sow the seeds of their own reversals. This quarter I’d like to call your attention to another fallacy of thought that many investors fall prey to: “fighting the last war.”

If you left the gate to your backyard open and your dog ran away, it’s natural for you to fear that that might happen again. Thus, you’ll worry greatly about it and be extraordinarily vigilant about locking the gate ever after, such that it’s most unlikely your dog walks out of your open gate again. It is more likely, however, that he gets out of the yard some other way that you haven’t thought of.

Investors are unusually well attuned to how the last bear market unfolded, and take measures to make sure they are not injured in that manner again. Usually, however, the next bear market unfolds in an entirely different fashion and catches most investors unaware. Citizens and politicians also take measures to “cure the ills that led to the last recession,” which unfortunately often leaves them unprepared for the next recession that unfolds quite differently.

As investors, it’s important to study the history of the economy and markets, not just that of the last ten or twenty years, but of the last several centuries. There are many ways that recessions can unfold and there are many types of bear markets. The same type of recession rarely strikes twice in a row and two identical bear markets usually don’t occur back-to-back. One must be vigilant to all the possible ways the economy can get into trouble and look for all kinds of impending trouble.

I mention these things because in my recent travels visiting many clients in all parts of the country, I’ve been hearing a constant theme: fear of a return to the travails of 2008-09, when the economy hit a major recession and stock indices fell more than 50% over 18 months. While I believe it’s inevitable that we’ll have a recession again in the next several years, I’m fairly certain it won’t look anything like 2008-09. Why? The last recession was driven by a liquidity crisis of the highest order, i.e., almost nobody, individuals or businesses, had any cash. The real estate bubble of the preceding decade had led everyone to believe that property prices would never decline, thus, “Why hold cash? Put all that money to work!” In fact, legions borrowed lots of money to buy all the property they could. When real estate prices finally fell, everyone (well, almost everyone) was cash poor. People scrambled to sell assets (stocks, bonds, property, you name it!), raise cash, and pay down debt. This led to a recession as people stopped buying other stuff all at the same time. And, debt reduction has continued for most of the last eight years, which has led to very slow growth since.

Today, even though both real estate and stock prices have recovered, few investors are cash poor. In fact, both data and anecdotal evidence show that investors and institutions (especially banks) are still sitting on “big piles” of cash (that’s not a technical term). In other words, people are not going to let 2008 happen to them again. They have padlocked the backyard gate. Whatever sort of recession occurs next, it’s most unlikely to be similar to the last one.

In fact, fears by so many that a recession and bear market are just around the corner is good evidence that they are not. Recessions and bear markets are usually the product of complacency, not fear. Our economic analysis leads us to conclude that the precursors of recession are not yet visible. And while this bull market is getting old, it doesn’t appear to us to be ready to reverse course. Of course, bad things can go bump in the night and unsettle the world, and we watch for those. But inasmuch as everyone seems to be ready to fight the last war, that last enemy is not likely to show up.

Thank you for your confidence in us.

Gratefully,

Mark A. Keller, CFA CEO and Chief Investment Officer

[Posted: 9:30 AM EDT] Although overall market activity is quiet this morning, there is a good bit of news. Here is what we are watching this morning:

Catalonia blinks—Rajoy presses: Yesterday, Catalan leader Carles Puigdemont declared and suspended independence, asking for talks with Madrid. PM Rajoy is having none of this, calling for Puigdemont to either send him a document outlining what he intends or stop talking about independence. If Catalan leaders follow through on independence, we expect Rajoy to respond with force and disband the provincial government. Puigdemont his trying to thread a needle, holding his independence coalition together while avoiding a crackdown from Madrid. We suspect the Catalan leadership doesn’t have enough support to risk civil conflict and so it will back down. Clearly, that is what the market expects.

PM May backtracks on Brexit? In a series of interviews, PM May would not say she would vote to leave the EU if another referendum were held today. May made a rookie political mistake—never comment on hypothetical questions. May has indicated she voted “remain” and we suspect she probably would again. This is raising pressure on her from Tory backbenchers who strongly lean toward Brexit. May is on shaky political ground which is making it difficult for her administration to negotiate Brexit with the EU. Political risks in the U.K. are rising. Corbyn’s Labour Party would probably win if an election were held today. There is great dissent within the Tories over May’s leadership but the party wants to avoid a leadership challenge, fearing a no-confidence vote and new elections.

Minutes today: The Fed minutes are due later this afternoon. We will be watching this release closely to monitor the degree of dissent from the recent path of policy tightening.

Rattling sabers: The U.S. flew two strategic bombers over the Korean Peninsula and President Trump met with military leaders to discuss a response to the North Korean threat. In addition, the U.S. Navy performed a freedom of navigation operation, sailing near islands claimed by China in the South China Sea. Perhaps the most interesting comment to emerge from the White House is that NBC is reporting that President Trump said in a meeting earlier this year that he wants to increase the U.S. nuclear arsenal.[1] This idea flies in the face of established trends and international agreements. The U.S. nuclear arsenal peaked in terms of warheads in the 1960s. From a strategic standpoint, the U.S. arsenal is large enough that the survivability of the human race would be in question if deployed. Thus, adding to that number of warheads seems counterproductive.

IMF upbeat: The IMF annual meetings are being held in Washington this week and the new World Economic Outlook is favorable. The IMF says the world is enjoying its most widespread and fastest growth spurt since the bounce observed in 2010, which was off the low base of the 2008 Great Financial Crisis. The world economy’s growth forecast was raised by 0.1%, with advanced economies increased by 0.2%. The Eurozone forecast was raised by 0.4% while the U.S. was reduced by 0.1%. Global growth is expected to rise 3.6% this year and 3.7% in 2018. Emerging economies are forecast to see 4.6% growth, with 4.9% in 2018.

Turkey increases tensions: A court in Turkey has sentenced a WSJ reporter, Ayla Albayrak, to two years in prison on terrorism charges based on an article she wrote. Albayrak is currently residing in New York, and carries dual citizenship in Finland and Turkey. Her article reported on the war between Kurdish militants and the Turkish state. We suspect this high-profile sentencing was designed to raise tensions with the U.S, which are already elevated due to a spat over travel visas.

[Posted: 9:30 AM EDT] Although it was mostly quiet overnight, we are awaiting a potential declaration of independence from Catalonia. Here is what we are tracking this morning:

A declaration of independence? Catalan Leader Carles Puigdemont is expected to address the regional parliament in Barcelona at 11:00 EDT amid growing speculation that he will declare independence. According to reports, the Spanish national police are poised to arrest him if he follows through. However, there is a bit of nuance in the announcement. Puigdemont may make a declaration of independence but it may not be immediate or unilateral. That outcome would be crafted to avoid his arrest and open a dialogue with Madrid. Of course, that action would disappoint much of his separatist coalition. On the other hand, if he goes for a unilateral declaration of independence, the region could face a military crackdown. The risk of a hard response from Madrid is that it could trigger sympathy for independence. Reliable polling is rather scarce but the latest polls from July indicate 41% support for independence, with 49% opposing separation. We suspect these numbers are a reasonably accurate reflection of voter attitudes. If Rajoy simply allows for a broad vote without interference (last week’s vote was boycotted by supporters of remaining in Spain), we suspect independence would lose. Apparently, Madrid feels uncomfortable with taking that chance. So far, problems in Spain have mainly been contained in Spanish financial assets. However, a breakaway problem in Spain could trigger similar movements elsewhere and lead to a collapse of the unity movement create by the European Union. If such a drive to self-determination gains momentum, the EUR could be undermined and depreciate.

North Korean hack: Korean lawmakers said yesterday that there is evidence North Korea hacked into classified South Korean military documents which included the blueprint for leadership decapitation operations against Kim Jong-un. North Korea is known to have sophisticated cyberwar capabilities. They are believed to have hacked into Sony Pictures (SNE (ADR) $37.04) and recently have attempted to steal bitcoin from South Korean cryptocurrency exchanges.[1] This news should be treated with caution. Although it is quite possible that North Korea was able to steal this information, it is also possible that South Korea allowed the North to take the data as part of a disinformation campaign.

Macron, Merkel disagree on EU reform: French President Macron has proposed reforms to the EU that include a unified fiscal budget and loose rules about debt restructuring. Germany, as expected, wants strict restructuring rules, which would likely lead to a greater divergence in Eurozone borrowing costs and reliance on individual nations to manage their fiscal affairs. Germany is a creditor state; it has no interest in making things easier for debtor nations. What the Germans fail to realize is that their pile of savings will do them little good if they can’t find a place to loan and invest these funds. For now, both nations remain in their respective corners with little likelihood of massive changes along the lines of further unification of the EU.

Occasionally, we find a book that has such an interesting message that we dedicate a Weekly Geopolitical Report to reviewing it. This week, we will look at The Great Leveler by Walter Scheidel.[1] The book is an extensive historical analysis of inequality and the factors that reduce it.

In this report, we will discuss the premise of the book, the “four horsemen” of income leveling and the future it portends. As always, we will conclude with potential market ramifications.

The Basic Premise

Inequality has become a critical issue. In 2013, President Obama said the following about inequality:

And that is a dangerous and growing inequality and lack of upward mobility that has jeopardized middle-class America’s basic bargain—that if you work hard, you have a chance to get ahead. I believe this is the defining challenge of our time: Making sure our economy works for every working American.[2]

Interestingly enough, Scheidel’s historical analysis makes it clear that the current level of inequality is hardly unique. And, a certain degree of inequality has been with us since the early stages of human existence. Archeologists note that even early gravesites of hunters and gatherers show distinctions of wealth and status. These differences steadily became more widespread as civilization developed.

In theory, society could take steps to prevent or reduce inequality. However, history suggests the opposite usually occurs. As agriculture developed, Scheidel’s analysis shows that wealth became increasingly concentrated. Scheidel’s key insight is that civilization and peace tend to bring rising income and wealth inequality.

However, a casual observation of history also suggests that wealth and income distributions are not permanent. Sadly, Scheidel’s conclusion is that massive societal disruption reduces inequality. He refers to these as the four horsemen of equality.

The Four Horsemen

The “Four Horsemen of the Apocalypse” comes from scripture.[3] The biblical reference is widely debated but, in general, it refers to tribulations. Scheidel suggests that his four horsemen refer to events that cause inequality to decline. Here is his list: Mass Mobilization War, Transformative Revolution, Societal Collapse and Plague.

[1] Scheidel, W. (2017). The Great Leveler: Violence and the History of Inequality from the Stone Age to the Twenty-First Century. Princeton, NJ: Princeton University Press.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Accept