[Posted: 9:30 AM EDT] Markets are very quiet in front of the FOMC meeting. We get the results later today at 2:00 EDT, with a press conference about 30 minutes later. Here is what we are watching:

The UN speech: On the surface, the president’s speech at the UN was more bellicose than we expected. The populist right was giddy; the centrist establishment was horrified. However, below the surface, we saw the speech as pure Andrew Jackson. As we have discussed before,[1] Jacksonian foreign policy rejects the globalist vision of policy, be it for the sake of business (Hamiltonian) or spreading American values (Wilsonian). Instead, it is based on supporting American sovereignty and supporting American interests first. At the same time, it is heavily invested in honor—the U.S. supports its allies but will react with overwhelming force against threats. Jacksonians reject the concept of limited war. This model of foreign policy, along with its more isolationist model, Jeffersonian policy, disappeared during the Cold War. It is clear the administration views North Korea and Iran as significant enemies. On the other hand, it seems willing to give more room to China and Russia. Although we expected a less aggressive speech, the content was no surprise. Thus, the potential for conflict in North Korea is elevated but, as we have noted before, there are no mobilization actions that one would expect if a conflict is imminent.

The Fed: Expectations are high for a beginning to the balance sheet runoff. We expect the Fed to stop reinvesting when bonds mature, initially allowing $5 bn per month to exit the balance sheet and eventually raising this to $50 bn. The dots plot will be of particular interest. Currently, fed funds futures put the odds of a December hike at virtually 50%. Thus, if the dots suggest the next rate hike isn’t coming until 2018, we could see some dollar weakness develop. This topic will likely be addressed in the press conference if it isn’t clear in the dots, which could lead to some volatility later in the day.

Another Russian bank in trouble: B&N Bank, one of the top five lenders in Russia, is reportedly in trouble and may need a bailout. This would be the second major bank in Russia in the past few months to require nationalization. Earlier, the Bank of Russia bailed out Bank Otkritie. To some extent, both banks have gotten into trouble by purchasing dodgy loans in smaller banks that were closed by the financial authorities. What is going on in Russia looks much like the Savings and Loan Crisis in the U.S. in the 1980s. The Bank of Russia is trying to consolidate the banking system and is encouraging larger banks to buy the smaller ones. However, the small banks apparently were in more trouble than they thought. We don’t expect these bank failures to become systemic; instead, the Bank of Russia will simply nationalize these bad banks. The risk comes from the potential for a forced expansion of the money supply, which would lead to higher inflation.

Catalan independence vote: The WSJ reports that the Spanish police have arrested 13 officials associated with the planned October 1st referendum for Catalonia secession. The Spanish government has stated that the referendum is illegal and has vowed to stop it by any means necessary. The government’s decision to crack down on officials will likely bolster support for the referendum within Catalonia. So far, the EU has refrained from intervening, apparently viewing it as an internal Spanish matter. However, the referendum can also be framed as a human rights issue and the EU’s failure to mitigate the tensions between the Spanish government and Catalonia could possibly undermine its reputation as a defender of human rights. If the problem festers, it could have a bearish effect on the EUR.

[Posted: 9:30 AM EDT] Markets are very quiet in front of the FOMC meeting, which begins later this morning. President Trump offers formal remarks to the UN this morning, too. Here is what we are watching:

The Fed: As we noted yesterday, we look for the Fed to begin balance sheet reduction after this meeting with no change in the policy rate. In general, there is still a chance the FOMC raises rates in December. We actually doubt that will happen; if the dots chart agrees with our outlook, the dollar could take another leg lower.

Tropical situation: Hurricane Jose will brush Long Island and the northeastern shore but will generally spin out to sea. Hurricane Maria is currently a Category 5 storm; it is expected to weaken modestly to a Category 4 but will slam the U.S. Virgin Islands and Puerto Rico then veer northward. The consensus of computer models have it moving almost due north by the weekend, sparing Florida and probably most of the U.S. mainland. Of course, conditions can change but missing the U.S. Atlantic coast is favorable news. Sadly, the Caribbean islands, many of them still reeling from Hurricane Irma, are set for a second hit that will severely set back recovery efforts.

North Korea: This week’s WGR, published yesterday afternoon, recaps the North Korean situation. SOD Mattis told Reuters today that the U.S. has military options that might spare Seoul from an artillery barrage but gave no details. Although it isn’t obvious to us just what such options might entail, as we noted yesterday, there is no evidence of U.S. mobilization that would be expected to precede military action. Thus, for now, financial markets are mostly ignoring North Korea.

Bitcoin: We continue to monitor the cryptocurrency market. Currently, the behavior seems more akin to gold than a currency. For the most part, a currency fulfills three roles—store of value, a numeraire and a medium of exchange. Gold and cryptocurrencies meet only one of these roles, the store of value. There is limited ability to use either for exchange or pricing things (the numeraire function) because of the volatility. The chart below shows the recent price behavior of bitcoin against the dollar. As a thought experiment, imagine that one borrowed in bitcoin in early January when it was trading around $1k. Your debt service costs have soared ever since. China is moving to quash bitcoin; it has shut down commercial exchanges and is now acting to inhibit peer-to-peer trading. We don’t expect the governments and the central banks to allow cryptocurrencies to undermine national currencies. After all, a currency is a symbol of national sovereignty. Thus, cryptocurrencies will likely be relegated to black market activities, allowing people to avoid capital controls and make cashless anonymous transactions.

The Kim regime has become increasingly belligerent, launching a number of ballistic missiles and testing what appears to be a hydrogen device. It is also claiming it has miniaturized a warhead, meaning, if true, North Korea is a nuclear power.

The U.S. has indicated this development is unacceptable. Although the Trump administration still says that “all options are on the table,” a full-scale war would be catastrophic and may be impossible to contain. The U.S. wants China to bring North Korea to heel; so far, the Xi government has been reluctant to push hard against Pyongyang. Meanwhile, Japan and South Korea are becoming increasingly worried about North Korea’s behavior.

Although the Hermit Kingdom has been the topic of reports on numerous occasions, an update on the basic geopolitical issue of North Korea is warranted given the volume of recent news. In this report, we will examine the motivations of North Korea and surrounding powers, including South Korea, Russia, China, Japan and the U.S. As always, we will conclude with potential market ramifications.

[Posted: 9:30 AM EDT] It’s Fed week! The FOMC meets this week, beginning tomorrow and ending on Wednesday. This meeting will bring new forecasts, dot plots and a press conference. Here is what we are watching today:

The President to the UN: President Trump will address the UN today. Although the media is watching this event very closely given the general anti-UN views Trump expressed during the campaign, we would expect a mostly neutral speech, read from a teleprompter. There is little to be gained politically by making a major negative speech at a venue where most of his political supporters will monitor. Although anything is possible, we would be very surprised by anything market moving.

The Fed: The consensus outlook is that the FOMC will keep rates steady and begin the process of reducing the balance sheet. This outcome is already discounted and shouldn’t have a major impact on financial markets. As we have noted before, most of QE ended up on bank balance sheets as excess reserves. Thus, removing those reserves shouldn’t have much of an effect on the real economy. On the other hand, sentiment could be adversely affected; expanding the balance sheet did have a positive effect on equity markets through a higher P/E. We will be watching to see if removing QE has a symmetric impact. Our expectation is that it won’t.

War drums: Although the financial markets are becoming inured to events on the Korean Peninsula, comments from Washington are becoming increasingly hostile. NSC Director McMaster believes that North Korea isn’t stable or rational enough to use nuclear deterrence policy if allowed to develop a fully operational nuclear weapon. If that is one’s stance, the only rational thing to do is attack before the weapon is fully developed. The plan appears to be to first lean on China aggressively, pushing Beijing to clamp down hard on the North Korean economy. The key there is an embargo on oil flows. If China were to cut off petroleum products to North Korea, the regime’s economy would grind to a halt in about a month. If this effort fails, military action becomes more likely. Despite all this war talk, we are not seeing the sort of actions we would expect if an attack was imminent. There is only one carrier group in close proximity; if a full-scale attack is going to occur, we would expect three groups to participate. We would also expect evacuations of non-essential Americans in South Korea. Until these two events occur, we do not see an impending military strike. We anticipate the financial markets will mostly ignore North Korea (barring an actual military strike from the Hermit Kingdom) until we see a buildup of carrier groups and evacuations.

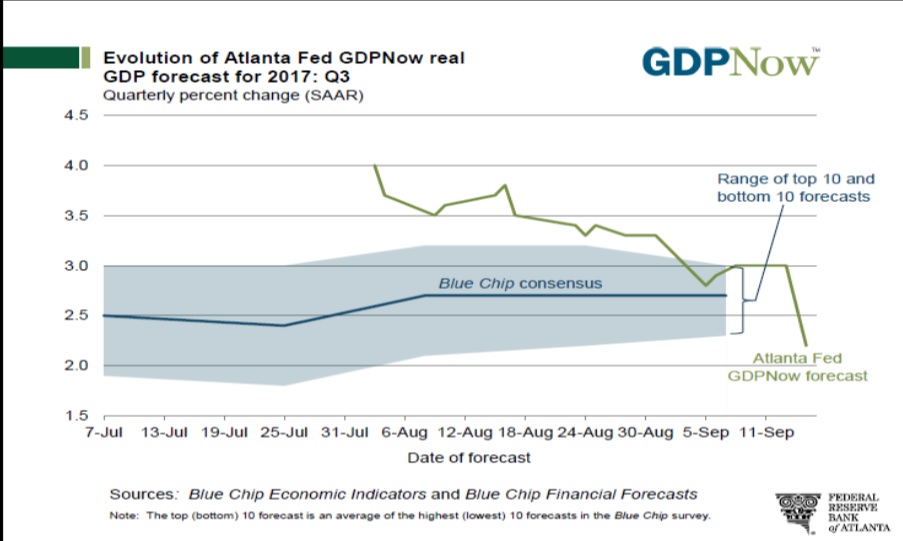

A tumble in GDP expectations: The Atlanta FRB produces a report called GDPNow that keeps a running estimate for the current quarter’s GDP based on the path of economic reports. The most recent report shows a rather sizeable dip in Q3 projections.

Estimates of GDP growth, which were running around 3%, have fallen sharply to 2.2%. Of the 80 bps drop, 52 bps came from a drop in expected consumption, reflecting last week’s weak retail sales data.

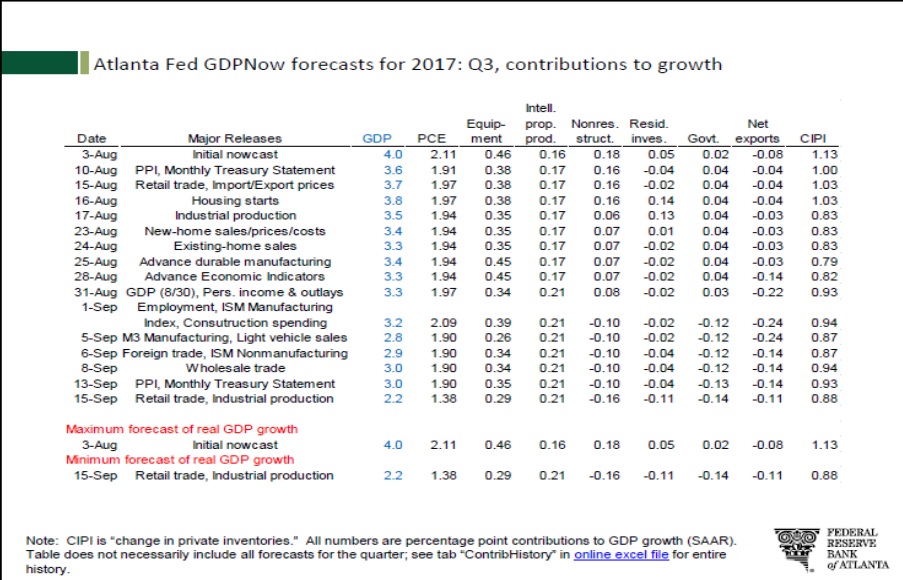

The table above shows the contribution to GDP from various components. The obvious drop in PCE is noted but investment in structures, both business and residential, fell 13 bps. Inventory rebuilding is expected to add 88 bps, down from 93 bps. We do think that much of this is coming from the hurricanes, which will drain inventories plus disrupt spending, at least in the short run. Of course, that will reverse as rebuilding begins.

Hurricane season isn’t over: Hurricane Jose is expected to brush the East Coast before dissipating over cool waters in the central Atlantic. On the other hand, Hurricane Maria is bearing down on several of the Caribbean islands recently devastated by Hurricane Irma. Given the level of damage already suffered, it is hard to imagine how recovery can continue if another major storm hits the region. Current tracking models suggest the path will be similar to Jose, moving north, then west and eventually reaching the northern Atlantic.

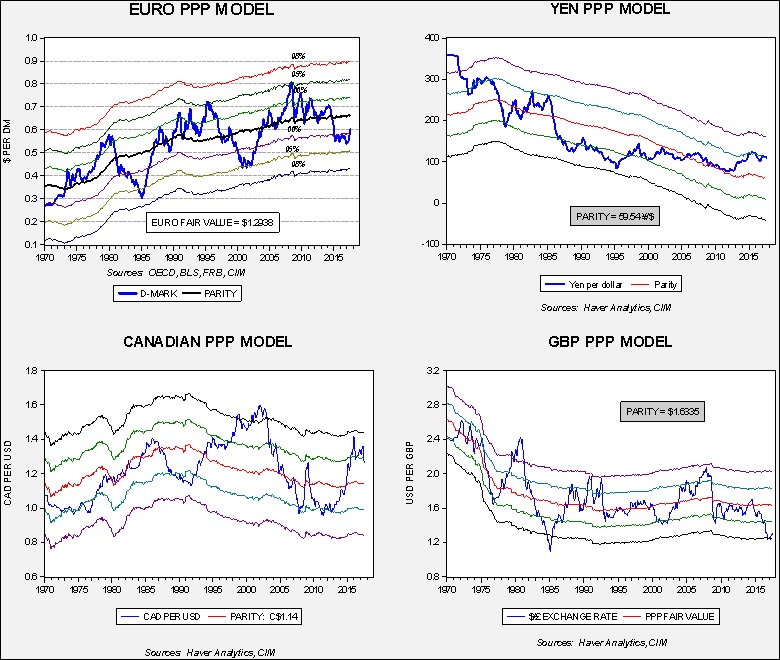

In our most recent asset allocation rebalancing, we added foreign allocations to our portfolios. Over the past few years, we had generally avoided allocations to non-U.S. markets in asset allocation portfolios due to two primary concerns. First, the dollar had been appreciating as a result of an improving U.S. economy and policy divergences between the U.S. and the rest of the world. The Federal Reserve was raising rates and tapering its balance sheet while the majority of other nations were still adding monetary stimulus. Second, we have had secular concerns about the stability and attractiveness of foreign investing in a world where the U.S. is seemingly reducing its hegemonic role.

We previously noted that the dollar was deeply undervalued on a purchasing power parity basis and vulnerable to depreciation. The catalysts for dollar weakness appear to be coming from two sources. First, the FOMC is moving very slowly to tighten policy while the rest of the world’s central banks are finally withdrawing policy stimulus. Second, uncertainty surrounding American governance appears to be undermining investor confidence and leading to dollar selling. In this week’s report, we wanted to update the valuation levels for the dollar against the yen, euro, Canadian dollar and British pound.

This chart shows four purchasing power parity models for the aforementioned currencies. In all four cases, the dollar was trading “rich” by more than one standard error, and nearly two standard errors from parity in two cases. Over the past two months, three of the four currencies have begun to appreciate and are indicating some modest improvement in valuation. However, these models all suggest that the dollar is still overvalued and thus, even with the recent depreciation, the greenback is still overvalued. Hence, the narrative that a weaker dollar should support further gains in overseas assets remains viable. If history is any guide, we are still in the early stages of a dollar reversal that should remain in place for the foreseeable future.

At the same time, the secular concerns about the impact of the withdrawal of U.S. hegemony will likely be a bearish factor for overseas investments. For now, we expect the dollar’s weakness to overshadow concerns over global stability. But, as some point, possibly in the next couple of years, the dollar will be closer to fair value and the case for foreign investment will be more difficult to justify.

[Posted: 9:30 AM EDT] Hawkish comments from the BOE continue to lift the GBP. Here is what we are watching today:

North Korea launches (yawn): As expected, North Korea launched a missile that passed over the Japanese island of Hokkaido. The missile appears to be an intermediate-range ballistic missile, not an ICBM. This missile’s distance exceeded the recent one over Japan and shows North Korea can now threaten Guam. Market reaction thus far has been enlightening. The usual flight to safety trade is long JPY, Treasuries and gold. All are lower today. Geopolitical tensions exhibit a pattern in markets over time. Unless conditions escalate significantly, each event has less impact with repetition. We have seen this pattern with terrorist events and now we are seeing it with missile launches. It does not appear that Kim Jong-un is taking into account Western financial market behavior with his provocations but, if he did, this one would be rather disappointing.

Terrorist attack in the London Underground: There was a terrorist attack in a London subway platform this morning. It appears to be an improvised explosive device that injured 22 people, none seriously. There was no obvious market impact, although follow-on attacks after these events do occasionally occur. We will continue to monitor the news flow.

Venezuela suspends dollar auctions, prices oil in EUR: Venezuelan President Maduro has indicated that his nation, in a bid to dilute the impact of U.S. sanctions, will be invoicing oil in EUR going forward. Iraq did something similar under Saddam Hussein. This scheme probably won’t work well for Caracas. The U.S. is a major trading partner with Venezuela and forcing U.S. firms to use EUR will simply discourage American buyers further. In addition, having EUR will increase the cost of servicing dollar-denominated debt, in that it will take another step in translation to adjust the debt. This move smacks of desperation.

The return of the Italian lira? Three of Italy’s largest political parties are calling for a dual currency to trade alongside the EUR. The Five Star Movement, the Northern League and Silvio Berlusconi’s Forza Italia have all proposed introducing a new currency following the election scheduled for next year. Italian lawmakers are using this as a threat to Brussels to allow Italy to violate the fiscal spending rules. In the last ECB press conference, Draghi shot down this idea, saying that there is only one legal tender in the Eurozone, the EUR. If Italy were to exit the Eurozone, it would be a serious blow to European unity, perhaps a bigger problem than Brexit. Although we have been bullish the EUR, this position would need to be reevaluated if this parallel currency movement gains momentum.

Bitcoin tumbles: China has outlawed cryptocurrency exchanges and various financial leaders in the U.S. have said derogatory things about these currencies. Bitcoin, the predominant cryptocurrency, has fallen over 30% recently. The sharp decline is an indication of the ephemeral nature of cryptocurrencies.

(Source: Bloomberg)

Saudi news: There were a few items of interest emerging from Saudi Arabia. First, Sputnik (admittedly, not the most reliable of sources) is saying the kingdom is looking for a vendor to build nuclear reactors for electrical power. The report indicates that no U.S. firms will be asked to bid on the project (which seems odd, given the warm relations the president seems to have with the king). The worry, of course, is that this plan will eventually lead to the kingdom getting nuclear weapons. Second, the crown prince appears to be behind a series of arrests designed to stifle dissent. According to reports, a number of clerics have been arrested.[1] We have been hearing rumors that the royal family is working to curtail the influence of the clerical establishment in a bid to loosen Saudi Arabia’s rather stodgy social scene. In addition to clerics, others have been arrested as well, including a member of the royal family. The NYT reports that Jamal Khashoggi, a long-tenured journalist and commentator, has moved to the U.S., fearing arrest.[2]

Iran deal approved: Yesterday, we noted that President Trump had to renew the Iran deal, which was expiring. Although there is growing concern he will end the deal, he did approve it yesterday but is indicating that he intends to curtail Iran’s influence in the region.

[Posted: 9:30 AM EDT] With the exception of the GBP, financial markets were quiet overnight. However, the CPI data and reports that North Korea may be preparing for a missile launch have led to increased volatility. And, there was a lot of news to cover this morning. Here is what we are watching today:

North Korea ready to launch: There are reports that North Korea may be preparing for a new launch. In a similar vein, analysts looking at the recent nuclear test are concluding that it was more powerful than first thought, increasing the likelihood that the Kim regime has developed a thermonuclear device.

The BOE: The Bank of England left policy unchanged, as expected, but in its statement the majority indicated that “some withdrawal of monetary stimulus is likely to be appropriate over the coming months.” The Monetary Policy Committee (MPC) voted 7-2 to keep policy steady, with the two dissenters calling for tighter policy. Although Governor Carney appears to remain dovish, fears of rising inflation are leading the majority of the MPC to lean toward raising rates. The GBP has rallied sharply on the news.

A DACA deal? Twitter lit up yesterday evening with reports that the president, along with “Chuck and Nancy,” made a deal on DACA, where the Democrats would support improved border security. Later, the White House indicated that a “deal” wasn’t done but discussions did occur. It appears the president is willing to trade DACA for border security. The important news here is that the president continues to form a working coalition with Democrats and moderate Republicans to isolate the Freedom Caucus. It isn’t obvious if this will become the main working coalition for this president or if he will create new groups on a continuous basis. However, there isn’t much evidence that President Trump has much sympathy for the Freedom Caucus; he doesn’t seem too inclined to shrink the government, deficits don’t bother him and a dovish Fed is preferred. Thus, isolating the Freedom Caucus may be his working position.

A Chinese deal blocked: The White House has blocked a Chinese investor from purchasing Lattice Semiconductor (LSCC, 5.72). The Committee on Foreign Investment in the U.S. (CFIUS) recommended scotching the deal. If the transaction had been consummated, it would have been the largest Chinese purchase in the U.S. microchip sector. CFIUS was concerned that the purchase would facilitate the transfer of intellectual property to China. Most of the time, once a company realizes that CFIUS isn’t going to approve its deal, it quietly kills it. The fact that Lattice and the purchaser, a private equity firm called Canyon Bridge Partners, continued to push the transaction is odd and suggests the firms may have thought the White House would overrule CFIUS. However, given the administration’s growing wariness of China, this hope seemed misplaced.

Iran nuclear deal at risk? The president must reaffirm the Iran nuclear deal every 120 days. President Trump has expressed displeasure with the Iranian deal; although we expect him to approve it today, we would not be surprised to see him try to reopen negotiations in the coming months. Every 90 days, the White House must certify that Iran is compliant to the agreement. The next date will be October 15th, and there are growing worries that Trump will declare Iran out of compliance. If the Iranian deal falls through, we would expect Iran to rapidly move toward building a bomb.

Russian war games: NATO leaders are watching Russia and Belarus hold large-scale war games. Officially, 12,700 troops are participating but Western government sources put the real numbers near 100k. The concern is that these exercises are a precursor to operations against the Baltic States. Thus, for the next week, the region will be on edge, closely watching the Russian military as it runs its war games.

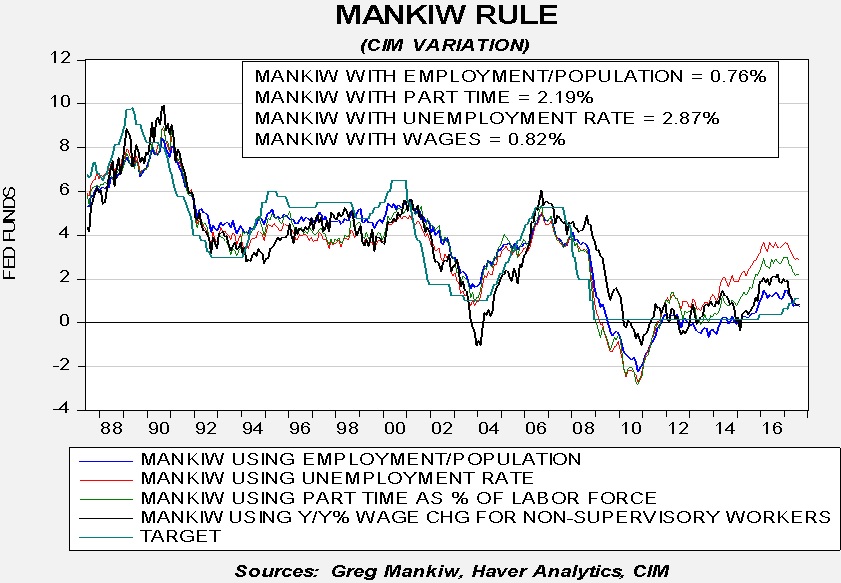

Fed policy: With the release of the CPI data we can upgrade the Mankiw models. The Mankiw rule models attempt to determine the neutral rate for fed funds, which is a rate that is neither accommodative nor stimulative. Mankiw’s model is a variation of the Taylor Rule. The latter measures the neutral rate using core CPI and the difference between GDP and potential GDP, which is an estimate of slack in the economy. Potential GDP cannot be directly observed, only estimated. To overcome this problem, Mankiw used the unemployment rate as a proxy for economic slack. We have created four versions of the rule, one that follows the original construction by using the unemployment rate as a measure of slack, a second that uses the employment/population ratio, a third using involuntary part-time workers as a percentage of the total labor force and a fourth using yearly wage growth for non-supervisory workers.

Using the unemployment rate, the neutral rate is now 2.87%. Using the employment/population ratio, the neutral rate is 0.76%. Using involuntary part-time employment, the neutral rate is 2.19%. Using wage growth for non-supervisory workers, the neutral rate is 0.82%. There wasn’t much change from last month; two of the models, the employment/population ratio and non-supervisory wage growth, are suggesting the Fed has achieved neutral policy. The other two remain elevated and indicate that at least another 100 bps of tightening are necessary to achieve neutral.

To a great extent, the issue for policymakers remains the proper measure of slack. The danger for the financial markets is that the proper measure is wage growth or the employment/population ratio but policymakers believe slack is best measured by involuntary part-time employment or the unemployment rate. If either of the latter two is their measure, policymakers will likely overtighten and prompt a recession. Although the headline data for inflation looks like price level growth is accelerating, core CPI is generally flat on a yearly basis. We are still not seeing much pricing pressure which means the FOMC will likely remain cautious.

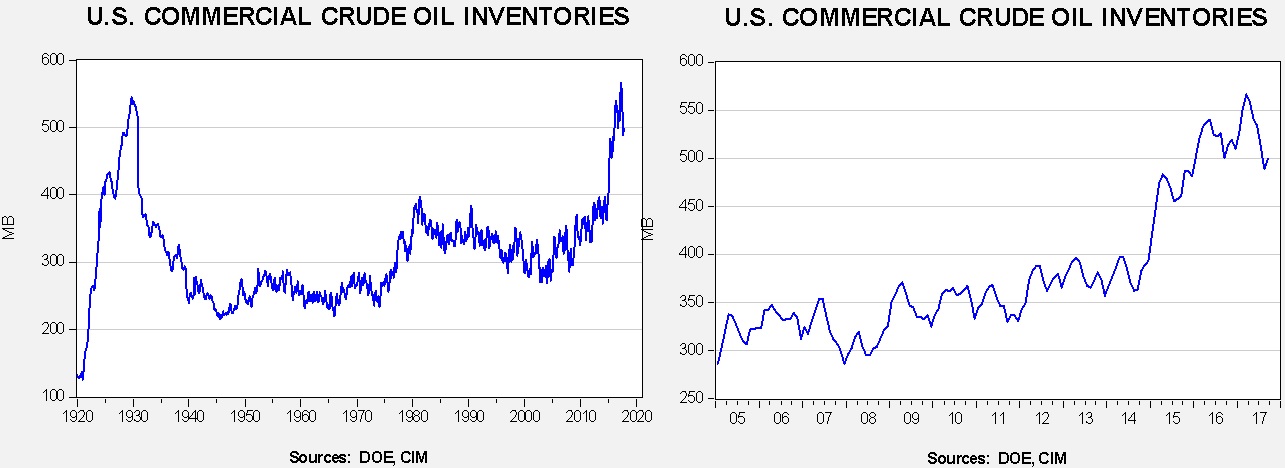

Energy recap: U.S. crude oil inventories rose 5.8 mb compared to market expectations of a 4.8 mb increase.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but have declined. Hurricane Harvey affected the energy market data again this week; the effects should continue for several more weeks.

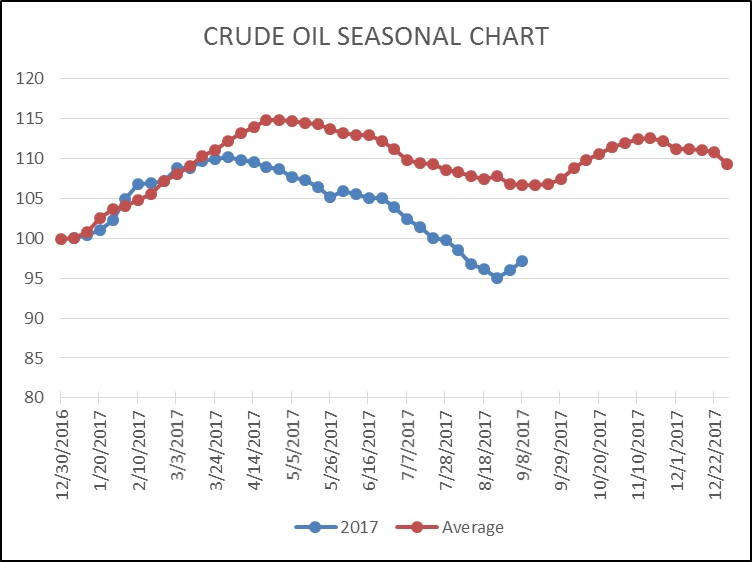

As the seasonal chart below shows, inventories did turn higher again this week but they were affected by the aforementioned hurricane. We are probably going to start the inventory rebuild period sooner than normal this year. Although oil imports remain depressed, dipping nearly 0.5 mbpd, and production recovered by 0.6 mbpd, refinery capacity utilized dropped 2% to 77.7%, or 4.4 mbpd below capacity. Media reports suggest that refineries are working hard to restart operations, but it will probably take a couple of months before the industry can achieve pre-Harvey refinery levels.

(Source: DOE, CIM)

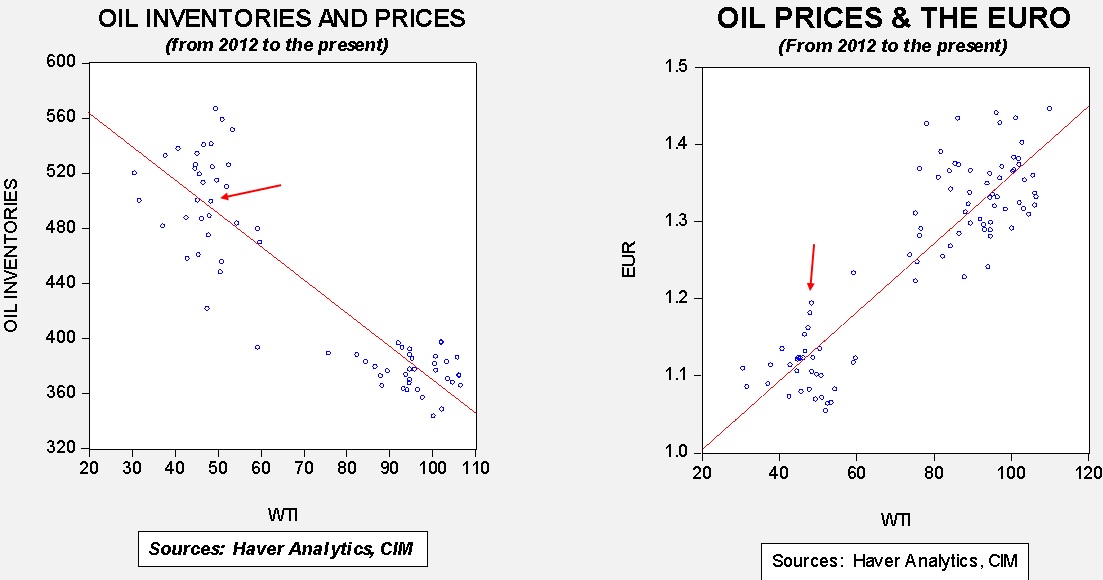

Based on inventories alone, oil prices are undervalued with the fair value price of $51.50. Meanwhile, the EUR/WTI model generates a fair value of $67.07. Together (which is a more sound methodology), fair value is $61.77, meaning that current prices are well below fair value. Although the most bullish factor for oil currently is dollar weakness, the rapid decline in inventory levels is also supportive.

Aramco delay: Saudi Arabia is suggesting that it may delay its IPO of the state oil company, Saudi Aramco, into 2019. That move suggests to us that the Saudis want to give the oil market more time to recover as they would likely want to price the offering in a better environment for oil prices. If so, that would mean they will probably continue to prod OPEC to keep output constrained. We view this as bullish news for the oil markets.

[Posted: 9:30 AM EDT] Financial markets are quiet this morning but there is a good bit of news. Here is what we are watching this morning:

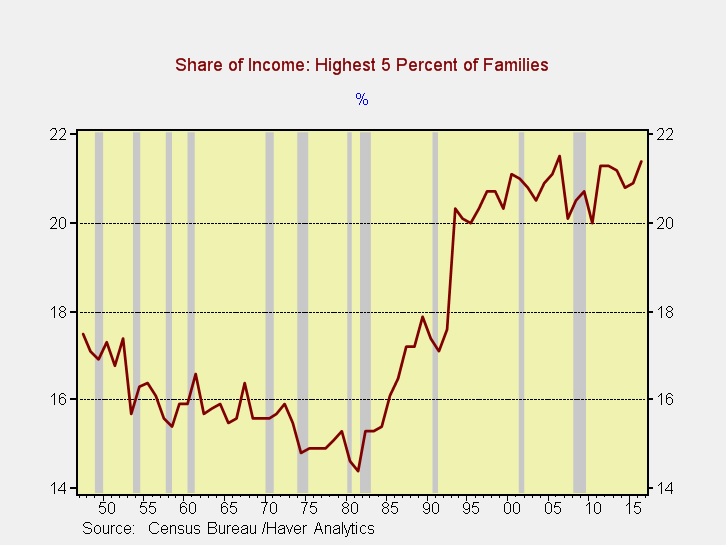

Census releases household income: The media is broadly reporting the Census Bureau report that real household income hit a new record at $59,039 in 2016, up 3.2% from the previous year. Although a clear improvement, most of the trends we have seen over the past four decades remain in place.

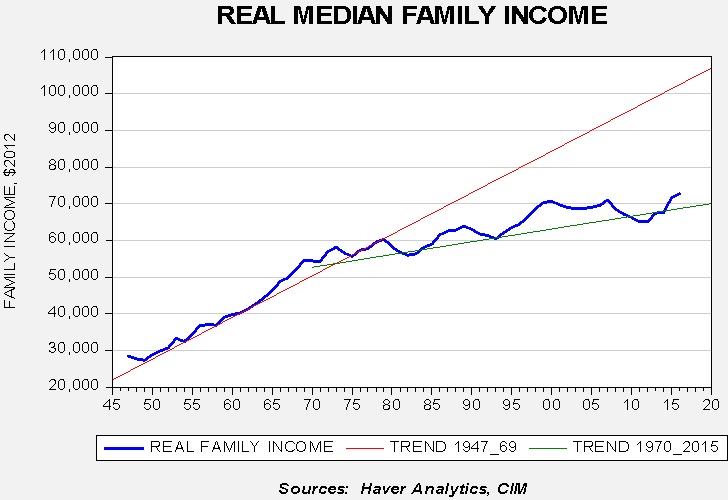

Census has another income unit, families (as compared to households). Family income is for those related by kinship or marriage, whereas household can be any group of cohabitating persons. In terms of family income, we remain on the mostly flat trendline that began in the 1970s.

As this chart shows, until about 1980, real family income was on a rather steep trajectory; after 1980, that trend leveled off substantially. Real family income for 2016 was $72,707; had we stayed on the earlier trendline, this number would be $102,465. When Americans complain about “falling behind” or questioning the American dream, part of that lament is that the trendline fell for family income growth. Why did this happen? There are a number of reasons, but the primary one in our opinion was the combined effect of globalization and deregulation. These two policies, key tenets of supply-side economics, were implemented to corral inflation. Although inflation clearly declined, the cost to society was higher inequality.

This chart shows the share of family income for the top 5% of families.[1] It reached its minimum in the early 1980s and rose sharply afterward. Essentially, growth in median family income stalled but rose sharply at the high end of the income scales. If a worker could compete in a globalized economy and cope with technology, that worker was amply rewarded. If not, the rewards were far less.

Politically, this disparity fostered the rise of populism. If the income distribution is going to change, we would expect policies designed to increase regulation of the economy and reduce globalization. Those policies would be inflationary over time, which brings us to our next point…

The rise of single-payer sentiment: Sen. Sanders (I-VT) is pushing the Democrat Party into a broad endorsement of single-payer health insurance. Politically, this is a minefield. Eliminating all forms of private insurance will be very disruptive. The hope of single-payer is, “I can get all the health care I want for free.” Of course, this is impossible. Tax rates would balloon to pay for this change unless cost containment is implemented. Clearly, this can be done because other nations do it, too. However, expensive treatments for various maladies are often not covered. The potential for disappointment is high. A much more reasonable approach would be to have a public option for health care and mandate an insurance coverage requirement. That would cover those who can’t afford private insurance. Several European nations use this model and it seems to work rather well. The problem for Democrats is that single-payer is rapidly becoming a litmus test for the primaries but it probably won’t be all that popular with the broad voting public.

Bullish IEA: The International Energy Agency, an arm of the OECD, released its August report today. It showed the oil supply fell 720 kbpd from July to 97.7 mbpd. OPEC cut output by 210 kbpd. Oil demand expectations were also lifted, expected to increase by 1.6 mbpd this year, which would be the strongest demand growth in two years. Meanwhile, Saudi Arabia is in discussions with OPEC to extend the production restriction agreement into mid-2018 (it’s scheduled to end in March 2018) and is chiding the group for cutting production but cutting exports less. Cartel members have been selling oil out of inventory to maintain market share. Saudi Arabia is pressing the group to cut sales, not just production. Oil prices could be poised to rally if Saudi Arabia can extend the output restrictions and convince OPEC to cut exports.

[Posted: 9:30 AM EDT] Yesterday’s market action was consistent with a sharp reversal in the recent risk trade. Amidst concerns about North Korea, the debt ceiling, trends in Washington, hurricane problems, etc., we saw Treasuries and gold rally, the dollar stumble and equities tread water. Those positions reversed yesterday with the dollar and equities rising strongly while the dollar dipped and Treasury yields rose. We are seeing some follow through overnight. It should be noted that renewed tensions with North Korea could bring a return of the aforementioned flight to safety trade. Here are some other items we are watching:

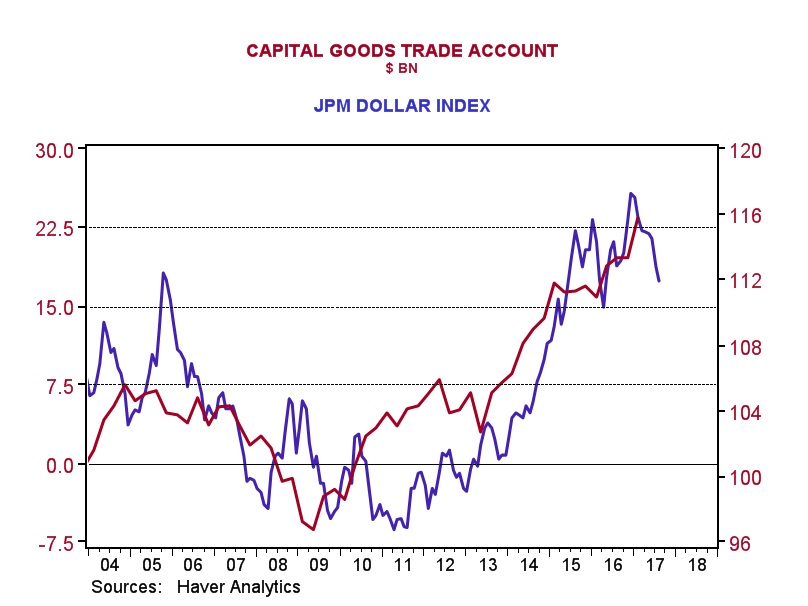

Capital goods balance and the dollar: We took a look at the capital goods trade balance; capital goods are goods designed for investment, e.g., machinery, rolling stock, etc. Over the past 12 years, dollar strength has led to a rising capital goods deficit.

Recent dollar weakness may slow the rising deficit, but a significant narrowing of this deficit would likely require further weakness in the dollar.

North Korea: As expected, the UNSC did approve additional sanctions on North Korea. However, these new sanctions are much less than the U.S. wanted. Given that China and Russia have veto power on the Security Council, getting any significant sanctions through the U.N. will be difficult. We do note that most major Chinese banks announced they will not open new bank accounts with North Korean ties. This action might be signaling that the Xi regime does not want to give into U.S. demands via the U.N. but wants to show its displeasure with the Kim regime over its behavior.

La Diada de Catalunya (Day of Catalonia): Yesterday, pro-independence supporters celebrated Catalonia’s national day by gathering in the streets of Barcelona in support of Catalonia’s independence referendum scheduled for October 1st. Last week, the Catalan regional government passed through legislation that would allow its citizens to decide whether to leave or remain as a part of Spain. The Spanish government has denounced the referendum as illegal and is looking for ways to stop the vote from happening. An independent Catalonia could potentially cause headaches for the European Union as there are no guidelines on how to deal with a breakaway state. In the past, the European Union has sought to quash separatist movements by stating that any breakaway state would have to leave and reapply. Currently, polls shows that the remain camp is ahead 49.4% to 41.1%. Although the vote is non-binding, a vote to leave Spain would embolden the separatists as they await the outcome of Brexit negotiations. If the U.K. is able to strike a decent deal with the European Union upon its exit, then separatists will likely argue that Catalonia could negotiate a similar arrangement.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Accept