Three weeks ago, we began our series on nationalism. In Part I, we discussed social contract theory before and after the Enlightenment. We examined three social contract theorists, Thomas Hobbes, John Locke and Jean-Jacques Rousseau. In Part II, we recounted Western history from the American and French Revolutions into WWII. From there, we examined America’s exercise of hegemony and the key lessons learned from the interwar period. This week, we will begin with an historical analysis of the end of the Cold War and the difficulties that have developed in terms of the post-WWII consensus and current problems. We will discuss the tensions between the U.S. superpower role and the domestic problems we face. Next, we will analyze populism, including its rise and the dangers inherent in it. As always, we will conclude with market ramifications.

[Posted: 9:30 AM EDT] Sixteen years ago, the U.S. suffered its worst terrorist attack in its history. The nation was changed in numerous ways, both large and small. Every time we fly commercial we are reminded that our safety was compromised. The country is still trying to unwind two wars related to the attack. On the other hand, the fears that the U.S. would suffer a subsequent similar attack have not come to fruition. This is due, in part, to America’s security and intelligence apparatus. It is also due to the likely fact that 9/11 was something of a long shot by al Qaeda that worked much better than expected. In any case, we still remember those directly affected by the event and keep them in our prayers.

Risk-on has returned to the financial markets. Here is what we are watching today:

A quiet Korean Peninsula: Although there was great fear that Kim Jong-un would test another ICBM, nothing occurred over the weekend. It’s possible that, despite Saturday being a major holiday in the DPRK, there are backchannel discussions going on and the lack of launch is a good faith effort. Or, it may mean Kim simply decided to enjoy the weekend. Meanwhile, the UNSC is working on some rather meek sanctions that probably won’t matter much. We would not be surprised to see the U.S. apply unilateral financial sanctions on North Korea, but it won’t be possible to put a direct oil embargo on North Korea because China won’t cooperate. At the same time, the NYT reports that the trade imbalance between North Korea and China is widening.[1] It isn’t clear what currency China uses when it settles trade with North Korea. Nobody wants the North Korean won and so we suspect North Korea simply builds arrears in CNY. Eventually, either trade will stop because firms will no longer want to accept IOUs from the DPRK or the Chinese government will swap the IOUs to pay the firms and settle the debt. Simply put, Chinese trade with North Korea could become more like aid, something we doubt China will continue with indefinitely.

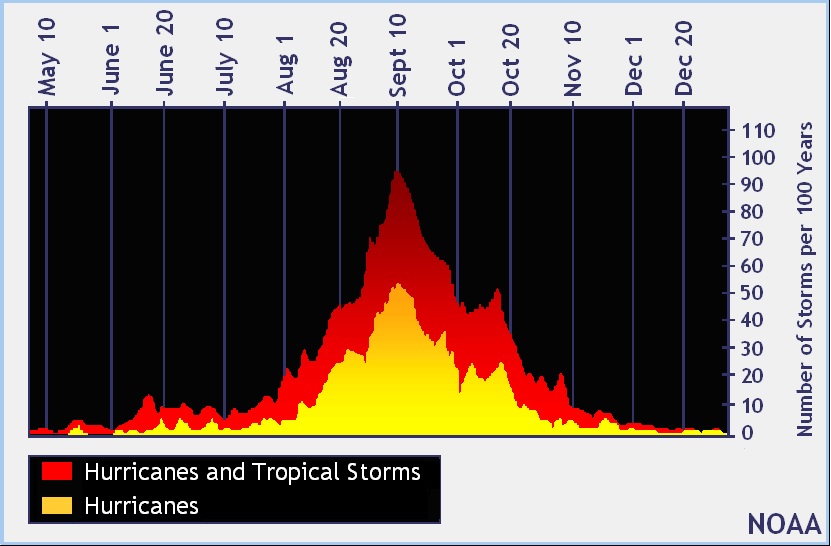

TS Irma: Hurricane Irma, which has been downgraded to a tropical storm, is now at the bend of the Florida panhandle. Although it led to devastation in the Caribbean, the impact on Florida, though significant, has been less than anticipated. It is rapidly turning into a rain event for Georgia and Alabama. Hurricane Jose looks like it is going to circle itself in the Atlantic. We will continue to monitor the storm but, for now, it doesn’t appear to be a threat to the U.S. On average, hurricane season peaks on Sept. 10th, so activity should steadily decline going forward.

China continues to clamp down on cryptocurrencies: China has shut down all virtual trading platforms as it takes steps to rein in cryptocurrencies. These electronic currencies are useful in skirting capital controls, something the Xi administration has been tightening over the past couple of years. Although XBT/USD rates remain elevated, the exchange rate is weakening, probably due to China’s restrictions on the use of cryptocurrencies.

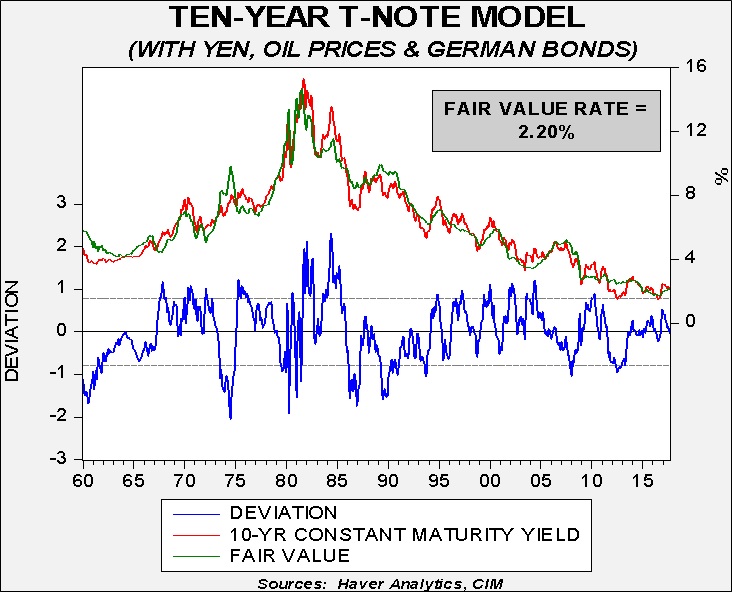

As the FOMC prepares to reduce its balance sheet, it’s a good time to update our views on long-term interest rates. The chart below shows our current estimate of fair value for the 10-year Treasury.

The model uses fed funds, the 15-year moving average of CPI (an inflation expectations proxy), the yen/dollar exchange rate, oil prices and German bond yields. The current yield is on fair value. Assuming the other variables remain steady, the current yield on the 10-year T-note is assuming the FOMC is going to hold rates steady for the foreseeable future.

Is this assumption on the policy rate reasonable? Currently, fed funds futures don’t reach a 50% chance of a rate hike until the June 2018 meeting, and even by next December the odds of a rate increase are only 67%. We expect the Yellen FOMC to use balance sheet contraction to placate the hawks on the committee and thus avoid increases in fed funds until it becomes abundantly clear that inflation is rising.

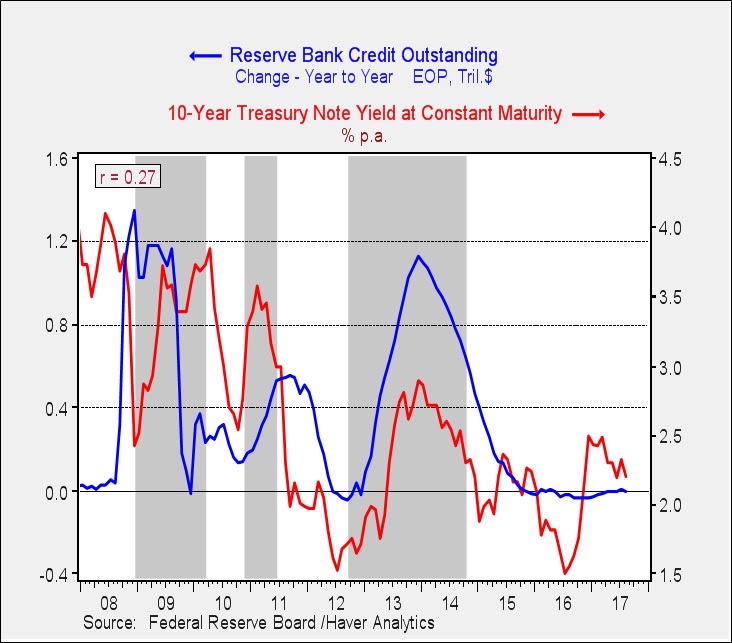

One of the reasons for expanding the Fed’s balance sheet was to lower long-term interest rates. In reality, the evidence of success is mixed.

This chart shows the 10-year T-note yield with the yearly change in the balance sheet. The gray bars show official periods of QE. A zero reading indicates no change in the balance sheet compared to the prior year. Rates fell in QE1, at least initially, although they did rebound as the recession came to an end in mid-2009. However, rates generally rose in QE2 and QE3. Although the Fed was buying longer dated Treasuries, which reduced its supply, it appears the demand may have weakened on fears that QE would trigger inflation. Thus, a case could be made that reducing the balance sheet would have a similar effect and push rates lower.

Our base case is that reducing the balance sheet will have an asymmetric effect on markets; in other words, it won’t have a significant impact on interest rates, unlike the apparent bearish impact that QE2 and QE3 had on long-term interest rates. This is because the FOMC is framing the reduction in the balance sheet as “normalization,” whereas QE was designed to be stimulative. Thus, our analysis suggests that the most important impact of QE was psychological. However, it is possible that QE did more than just boost sentiment; if so, balance sheet normalization could be bullish for long-duration bonds.

[Posted: 9:30 AM EDT] Market action is sluggish this morning; the big story is the continued weakness in the dollar. Here is what we are watching today:

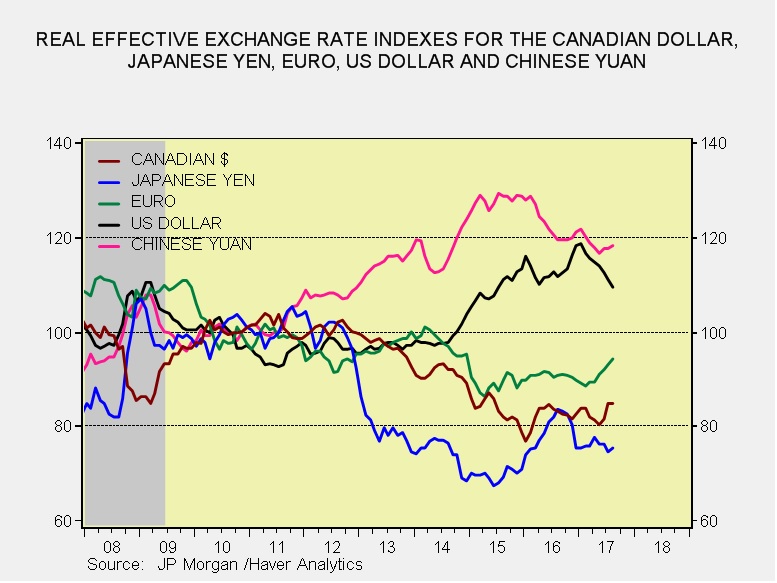

The dollar in perspective: The EUR is threatening $1.210 and the greenback continues to slide despite dovish comments from ECB President Draghi yesterday. The chart below shows the real effective exchange rates for the USD, CAD, EUR, JPY and CNY.

Although the dollar is weakening, it is worth noting that it remains unusually strong against most major currencies except the CNY. If exchange rates are in the process of normalizing, the dollar still has a lot of room to decline. In the foreign economic sector, we note that both China and Germany had disappointing export numbers. Although it’s probably too soon for the dollar’s weakness to have a significant impact on trade, it is possible that we are seeing the early effects. We also note reports that China is becoming “concerned” about currency strength. We remain dollar bears and expect greenback weakness to continue.

Nature bites: Hurricane Irma’s path has shifted westward and is now expected to move through the entire Florida peninsula into Georgia and end up as a depression in Tennessee by next Wednesday. Hurricane Jose looks like it will head into the Atlantic away from the U.S. mainland but is on target to hit Bermuda later next week. Finally, Katia is expected to make landfall near Veracruz tomorrow morning. Adding to Mexico’s woes, the country was hit with a major 8.1 (or, based on some reports, an 8.2) Richter scale earthquake yesterday evening. The epicenter was 60 miles from Mapastepec in the state of Chiapas. This is the most powerful earthquake to hit Mexico in over a century. Tsunami alerts were issued for Ecuador, Vanuatu and New Zealand. All these events will distort economic data for the next two to three quarters.

Warnings of a North Korean missile test: It’s a holiday in North Korea, commemorating the 69th anniversary of the founding of the Democratic People’s Republic of Korea (DPRK). South Korea is reporting that there are signs of another missile test. Worries about tests are boosting the JPY and gold this morning.

More on Washington: Yesterday, we detailed Trump’s triangulation with the Democrats. There are reports the president is working with lawmakers (mostly Democrats) to end debt ceiling votes. Debt ceiling votes began with WWI; before that, each act of government borrowing required an act of Congress. To handle the increased spending for the war, Congress set a limit for debt and allowed debt spending to occur until the limit was reached. Once reached, a new limit would have to be set. Note that the debt limit pays for spending that has already occurred. About the only impact the debt ceiling vote should have is to act as a reminder to lawmakers that debt is rising. However, it has become a tool of the party in opposition to use the leverage of shutting down the government to get its priorities passed. What is interesting about this potential change is that it is being pushed by a GOP president with Democrat Party support against the will of a significant faction of Congressional GOP members. We will see if the president can craft a workable legislative majority of Democrats and “Tuesday Group” Republicans to isolate the Freedom Caucus in order to pass other legislation.

Catalonia: Catalonia has voted to set a referendum on self-determination (or secession) for October 1, 2017. Madrid opposes the vote and will try to prevent it from occurring. It is possible the courts will prevent the referendum from being held, but even if it is held the Spanish government will likely choose to ignore it. There are various separatist movements in Europe. Scotland has been drifting toward leaving the U.K., and Czechoslovakia split into two states in 1993. This is a real problem for the EU; while EU elites try to unify Europe, states within Europe are facing pressure to split even further. This makes European unity an even more distant goal.

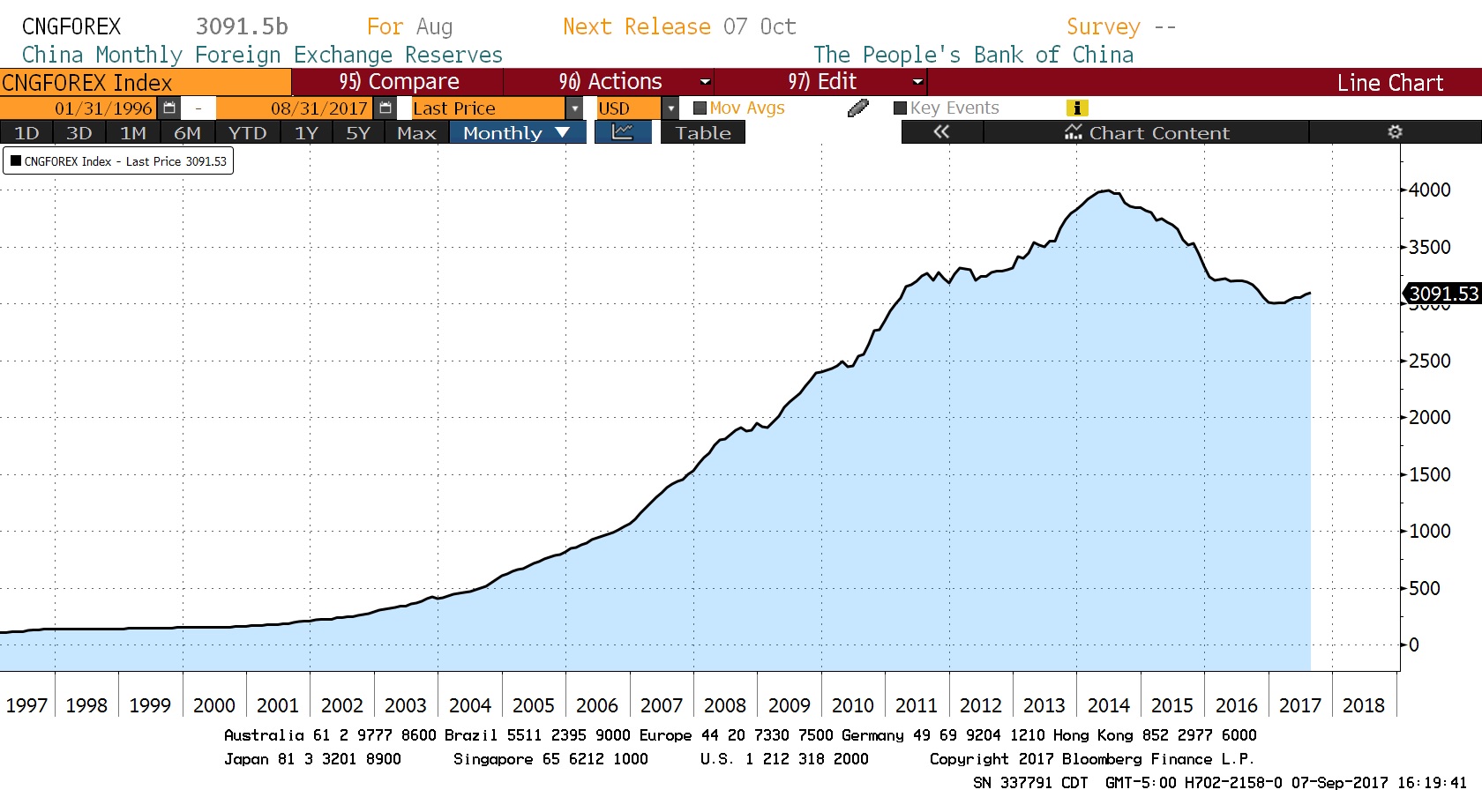

China’s foreign reserves: China’s foreign reserves rose $11 bn to $3.09 trillion.

(Source: Bloomberg)

Although reserves remain well below their 2014 peak, they have recovered from the recent trough of $2.998 trillion. China has taken steps to slow outflows and, thus far, is having some success.

EU rules that nations must take refugees: The EU Court of Justice has ruled that nations must take their assigned quotas of refugees, rejecting actions brought by Slovakia and Hungary.[1] It remains to be seen if these two nations will be forced to take refugees; we actually doubt they will. Many nations in the EU passively rejected their obligations to take migrants coming from the Middle East and Africa. Hungary reacted angrily to the news and Poland may also face retribution from the EU for its rejection of some migrants. This is yet another example of the EU overriding national sovereignty in Europe and will raise political pressure for other nations to follow Britain’s example. That’s why Germany and France are adamant that the U.K. face significant penalties for Brexit to create an example of the cost of leaving the union.

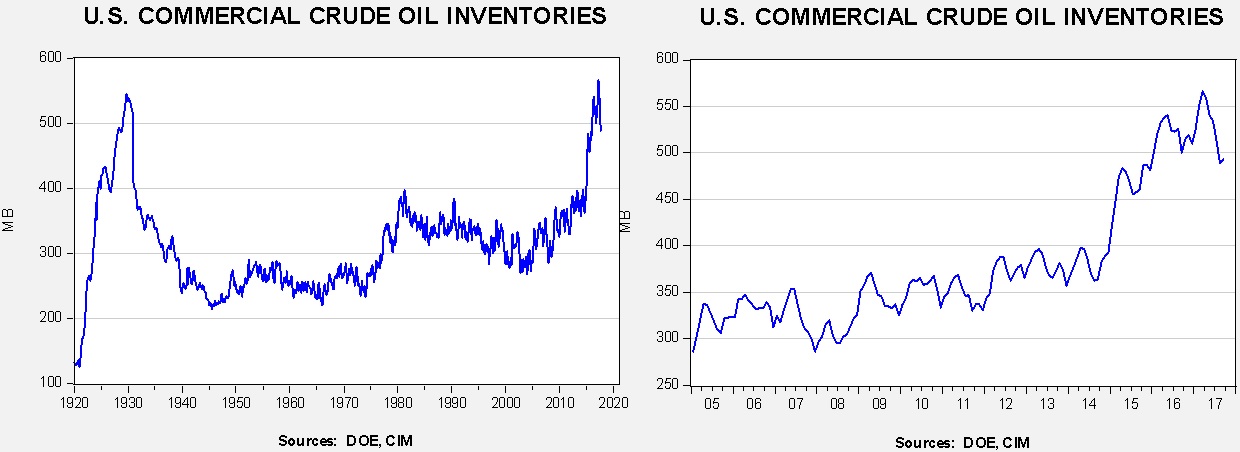

Energy recap: U.S. crude oil inventories rose 4.6 mb compared to market expectations of a 2.5 mb increase.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but they have declined. Hurricane Harvey had a dramatic impact on the energy market data this week; the effects should continue for several more weeks.

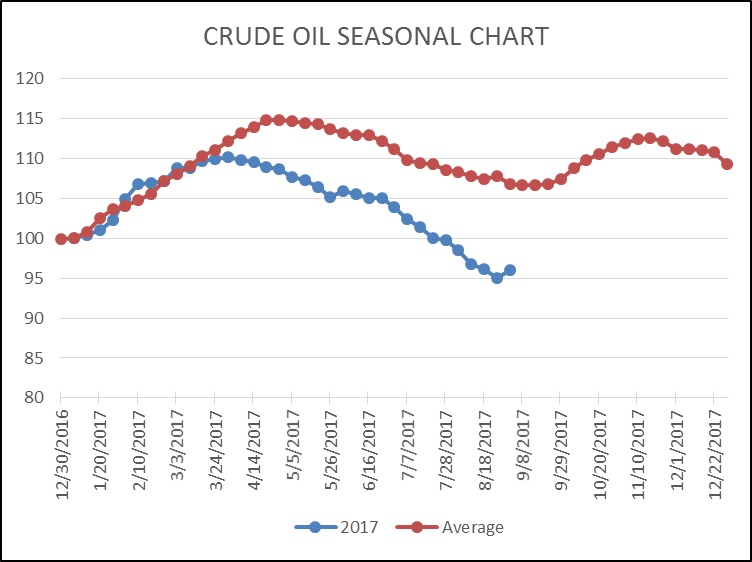

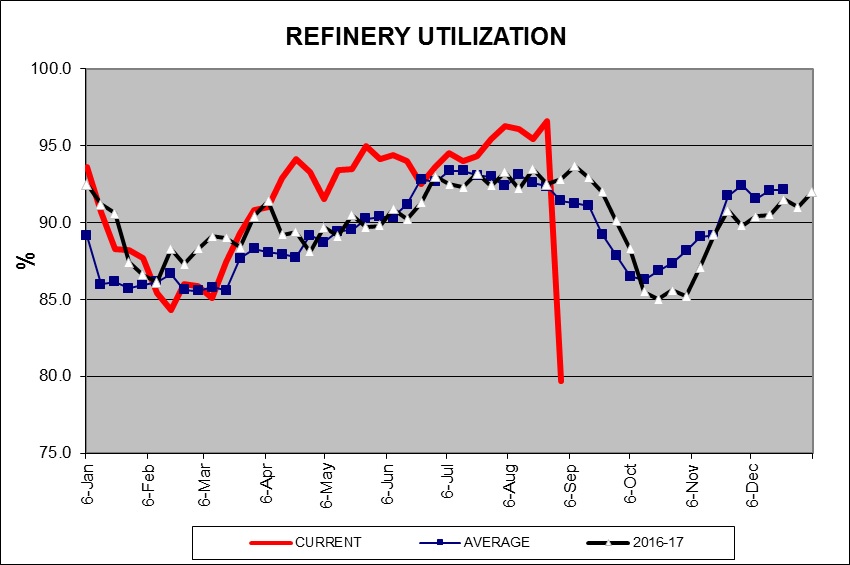

As the seasonal chart below shows, inventories did turn higher this week but they were affected by the aforementioned hurricane. We are probably going to start the inventory rebuild period sooner than normal this year. Although oil imports did decline by nearly 0.9 mbpd and production fell by almost 0.8 mbpd, refinery capacity utilization dropped to 79.7% from 96.6%, or 3.2 mbpd. Media reports suggest that refineries are working hard to restart operations, but it will probably take a couple of months before the industry can achieve pre-Harvey refinery levels.

(Source: DOE, CIM)

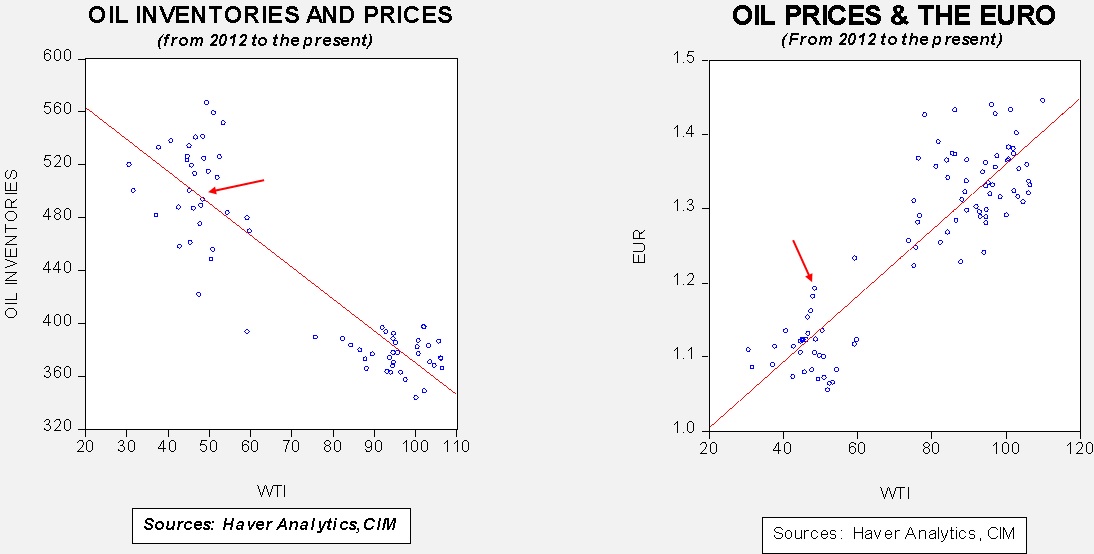

Based on inventories alone, oil prices are undervalued with the fair value price of $53.39. Meanwhile, the EUR/WTI model generates a fair value of $66.68. Together (which is a more sound methodology), fair value is $62.16, meaning that current prices are well below fair value. Although the most bullish factor for oil is currently dollar weakness, the rapid decline in inventory levels is also supportive.

The drop in refinery operations is stunning.

(Source: DOE, CIM)

We do expect operations to recover in the coming weeks. Note that we are close to the onset of the maintenance season. As noted earlier, we do expect to see a recovery in the coming weeks but only to about 85% next month, with a gradual recovery to 90% by winter.

[Posted: 9:30 AM EDT] Happy productivity day! Lots of news this morning; here is what we are watching:

The ECB: The ECB’s statement was a repeat of the one from a few weeks ago. In the press conference, the reporters focused most of their questions on the exchange rate. President Draghi deftly fended off these questions by not commenting on any particular level and by discussing the exchange rate outside the parameters of broader policy goals. In response to the lack of direct opposition to the recent rise in the EUR, the currency rose rather sharply, shown in the chart below.

(Source: Bloomberg)

The fact that policy didn’t change and there is no indication that policy will markedly tighten anytime soon, the EUR’s rise suggests that (a) the financial markets realize the EUR is still undervalued (we put fair value around $1.300), and (b) the dollar’s weakness is originating from the U.S. and not from abroad.

The Trump Shuffle: President Trump stunned the GOP leadership (and probably much of the party) by cutting a deal with the Democrat Party leadership to pass a short-term debt ceiling bill. House Minority Leader Pelosi and Senate Minority Leader Schumer engineered a deal that will raise the debt ceiling but only until December. The media is full of reports from GOP activists apoplectic about this turn of events. Although the degree of anger is understandable, we are somewhat surprised by the shock. Our position has been that our two-party system is a program of enforced coalitions; history shows that these coalitions change over time. The GOP houses a number of different factions. The GOP establishment is mostly center-right; supportive of markets, deregulation and moderately conservative on social matters. This group is generally resigned to large government and thus wants to shape that government to its own ends. There is a small government faction, often called the “Tea Party” and includes the Freedom Caucus in the House, that wants to return government to the pre-Roosevelt period; Grover Norquist is the key leader of this group. Social conservatives have also gravitated to the GOP. The key to Trump’s victory was wooing the disaffected white working class voters; traditionally Democrats, this group has discovered that the Democrats are focused more on identity rather than class. In other words, the Democrat Party leadership will celebrate differences in culture while purposely ignoring economic issues. This explains why the Democrat leadership was caught flat-footed by the rise of Bernie Sanders. Trump promised to restrict globalization (in both trade and immigration) and increase government support (he wanted a bigger health care program and infrastructure spending).

After the election, the GOP leadership wanted to accommodate the goals of the Tea Party and the establishment through tax cuts and spending reductions. Although Trump wasn’t necessarily opposed to these measures, his focus was on the white working class. When the Freedom Caucus wanted to tie spending cuts to the debt ceiling increase and was willing to risk hurricane aid to get what it wanted, Trump decided to get a better deal from the opposition party. Although the media is suggesting Trump has no ideology,[1] we would suggest otherwise; he wants to help the working class who have been harmed by a nearly four-decade bipartisan policy of deregulation and globalization. Note that he characterized the GOP health care plan as harsh and is ok with tax cuts, but has no worries about the deficit. In other words, he sees no need to cut spending.

Although other presidents have “triangulated” between their own party and the opposition (Bill Clinton was a master at this), we see Trump as doing something different. He is creating conditions that will lead to a realignment of party coalitions. We don’t know how that will evolve; third parties might emerge for a time. It’s important to remember that the Whig Party existed from 1834 to 1854 but was unable to hold together (slavery led to the dissolution). A multi-ethnic (or, perhaps, multi-identity) working class party and a market-oriented party of globalization and deregulation could emerge.

In the short run, although the debt ceiling issue is probably off the table for now, it will return soon enough. For the opposition party, making the majority vote to raise the ceiling multiple times before the midterm elections is a favorable outcome. However, Democrats should be careful in how they embrace the president. If Trump can craft a protectionist policy and raise infrastructure spending, he could woo some Berniecrats and widen the divisions within the Democrat Party as well. In our opinion, the key point here is that the party coalitions are shifting; instead of thinking about party, investors should focus on factions. Conditions will likely become increasingly confusing if one’s thinking remains in the framework of traditional GOP/Democrat characteristics.

Fed Drama: Vice Chair Fischer dropped a blockbuster yesterday by unexpectedly resigning, effective Oct. 13, for “personal reasons.” We have no insight into what those might be, but we note he is 73 years old and the grind of central banking is probably a lot for anyone. Although we expected Fischer to be out early next year, this removes a mainstream voter and a sage central banker from the FOMC. At the same time, Gary Cohn, who was thought to be a lock for the Fed chair job, is apparently unlikely to get the position. The president doesn’t handle criticism well; the very public criticism that Cohn expressed over the Charlottesville issue appears to have changed the president’s mind. The combination of these two events probably means the odds that Yellen gets extended have increased markedly. It is also worth noting that virtually all the candidates for governor positions reported in the media are hawks. We suspect that Trump is figuring this out and has no interest in appointing a hard money person to the Fed. Thus, we would not be shocked if none of the names mentioned are actually nominated and more dovish candidates are recommended by the White House. As noted in the above discussion, the president really isn’t a small government, low inflation person. He is ok with deficits and inflation and it would make more sense for him to choose Fed governors who share those positions. And, we would not be surprised to see Cohn leave soon.

The Tropical Situation: We have three active hurricanes; one will likely hit Mexico, Jose will probably go out to sea, but Irma is another matter. Its forecast path is to hit Florida and then move into the Atlantic Seaboard. Next week, we could see weather disruptions in this region.

[Posted: 9:30 AM EDT] Financial markets are easing off the flight from risk exhibited yesterday. There wasn’t a lot of breaking news overnight, but there are currently several significant news items. Here’s a recap:

Hurricane Irma: There are three tropical events in the Atlantic but Irma is the current focus of attention. It is a massive Category 5 storm that is presently hitting the Caribbean islands. Yesterday, a majority of the computer models were showing the storm taking a northward hook into Florida by the weekend, but there were a couple of models that suggested the turn may occur late enough for the storm to enter the Gulf of Mexico. If the path continued west, Texas and Louisiana might be hit again by a major storm. However, there is universal agreement among the models this morning that Irma is going to move straight up the Florida peninsula by Monday. The cold front that moved across St. Louis on Monday will steer the storm northward. As we have covered energy since 1989, we do know that computer models are not perfect; if the cold front stalls, a more western drift is possible. But, for now, it appears that the Sunshine State will be the target on the U.S. mainland.

This will be the second major storm to strike the U.S. this hurricane season. The need for emergency government spending should end any uncertainty surrounding the debt ceiling passage, at least in the short run. However, this issue may return by late December. Interestingly enough, financial markets are not convinced that the hurricanes will force a debt ceiling reconciliation.

(Source: Bloomberg)

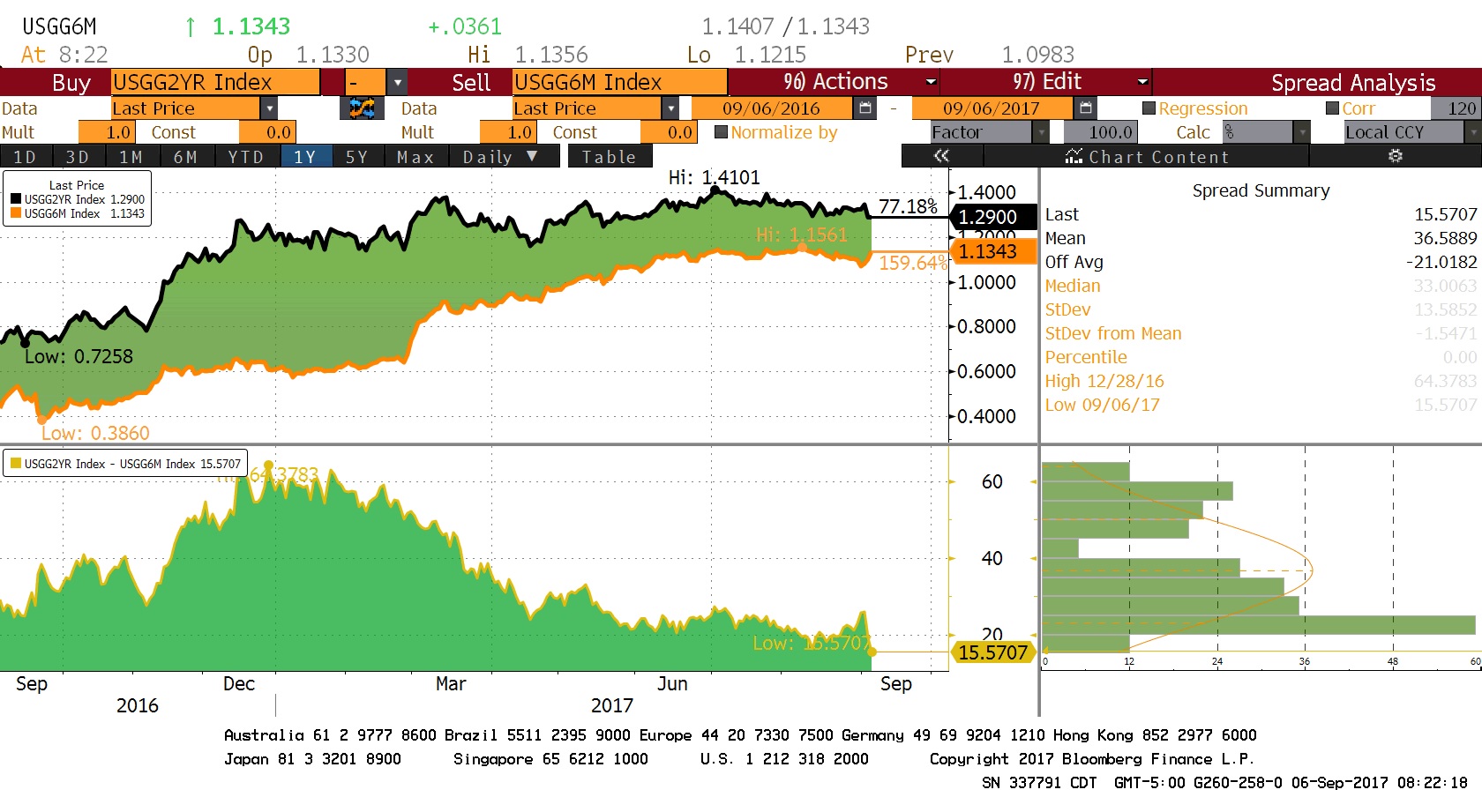

This chart shows the six-month T-bill rate along with the two-year T-note rate. Note that the spread has significantly narrowed recently as bill rates increased while two-year rates fell. We suspect that fears of a short-term disruption related to the debt ceiling are boosting bill yields, while the feared negative impact on the economy weighs on the potential for future Fed rate hikes, easing the note rate. We would expect this spread to widen again if our analysis is correct and the hurricanes force a clean debt ceiling rise.

When doves cry: Fed Governor Brainard and Minneapolis FRB President Kashkari gave talks yesterday. Both are doves; the latter has dissented from recent rate hikes and the former has expressed deep caution about moving rates higher too quickly. Kashkari said yesterday that the recent hikes may have already adversely affected the economy. We find this argument difficult to support; GDP growth is running around 3% and the current Atlanta FRB GDPNow forecast for Q3 GDP is 3.2%, incorporating the somewhat weaker than expected employment data. Maybe Kashkari will be right in the future but, for now, the impact of recent hikes doesn’t appear onerous. Brainard’s comments appear to be on more solid theoretical footing. She suggests that current low inflation isn’t just a series of idiosyncratic events but is, in fact, structural in nature. In other words, inflation is coming down on a secular basis, and running monetary policy on the premise that price levels will normalize will likely lead to overly tight policy and invite a recession. Essentially, Brainard is arguing that inflation expectations are becoming unanchored to the downside and that monetary policy should take this idea into account and perhaps lean against this trend.[1] Our economic work suggests that the central bank has little impact on inflation; instead, inflation is the intersection of aggregate supply and demand. And, in a globalized and deregulated world, the aggregate supply curve is nearly horizontal, meaning that increased demand has little impact on inflation. However, the central bank does have an impact on inflation expectations; if it appears too accommodative, it can spook businesses and households into precautionary spending. Simply put, if a household or business fears future price increases, it “saves” by holding inventory, further boosting price levels. The central bank isn’t the only factor in inflation expectations, though. One’s experience of inflation over a 10- to 20-year time frame also affects inflation expectations. Essentially, the Fed now has the opposite problem it faced in the 1970s. At that time, inflation expectations were elevated and the Volcker Fed had to act aggressively to convince households and firms that it would take steps to bring down inflation. Now, expectations of continued low inflation have become so entrenched that the Fed faces the need to convince economic actors that it won’t snuff out the economy prematurely.

The key question is whether or not Brainard’s position will sway her fellow FOMC members. It’s probably unlikely. Although it’s too simplistic to say that age affects the process of monetary policy, in fact, a significant number of influential members, including the chair and vice chair, came of age during the 1970s and are probably affected by that experience. It is no coincidence that Brainard and Kashkari are among the youngest members of the FOMC. Perhaps the only way the Fed becomes comfortable with persistently easy policy is through generational change. It is true that policy has been persistently accommodative, but it is also true that the preponderance of policymakers at the Fed appear to view current policy as an emergency measure and not a structural shift. Brainard is arguing for a structural shift. We doubt her argument will carry the day at the current Fed but it may in the future.

DACA: We haven’t commented on this issue yet because our focus is on financial markets. However, now that action is being taken, this issue will begin to affect the financial markets. DACA now becomes another distraction for a Congress that has lots of them. So, instead of working on tax reform or infrastructure spending or a budget, Congress will have to deal with this issue. Given the deeply divided nature of Congress, it is hard to see how they can address such a contentious problem and thus working on DACA will delay other agenda items.

[1] We recently discussed the issue of weak wage growth and noted that while nominal wage growth is running well below where it historically should be based on labor market conditions, real wage growth is actually consistent with current labor market conditions. https://www.confluenceinvestment.com/asset-allocation-weekly-july-14-2017/

[Posted: 9:30 AM EDT] Goodbye summer! We are now moving into autumn. Here is what we are watching today:

North Korea: The Hermit Kingdom was active over the holiday weekend. It detonated another nuclear device, claims to have miniaturized it for a warhead and is reportedly preparing for another missile test. The U.S. is working with the UNSC on additional sanctions but the Russians appear to have killed the idea, suggesting additional sanctions won’t work. In some respects, nothing has changed. The U.S. doesn’t want to see North Korea acquire a nuclear weapon that can threaten the U.S. South Korea doesn’t want any military action, fearing it will face an artillery barrage that will leave thousands dead. China isn’t pleased with North Korea’s actions but (a) doesn’t want any drama before the CPC’s October meetings when Chairman Xi gets his second term and his own team of advisors, and (b) doesn’t want to lose a buffer state on the Korean peninsula. Russia likes to see the U.S. occupied with something other than Russia. Japan fears a North Korean attack; it also worries that the U.S. will be willing to sacrifice Tokyo to a nuclear attack in order to spare Los Angeles. The situation is a mess; the U.S. must work quickly if it wants to prevent North Korea from acquiring a nuclear threat to the U.S. mainland. Although the Hermit Kingdom has missiles and devices, it hasn’t proven it can actually deliver a warhead. Clearly, it is working hard to acquire such capabilities.

War isn’t inevitable. Diplomacy can still work. However, it appears that warlike actions will be necessary in order to really deter North Korea. One way to achieve this would be a total blockade, which is considered an act of war; to work, China must be on board. China has mixed aims with North Korea but probably wouldn’t support a blockade, which would cut off oil supplies. There are reports the military has a year of oil reserves in storage but the rest of the economy has only about a month; on the other hand, the Kim regime has historically been willing to tolerate extreme deprivations of the civilian economy to achieve its aims.

We continue to monitor the situation. Clearly, the financial markets are worried but don’t think war is imminent. Our position is that the potential for conflict is still well below the 50/50 threshold but probably higher than the market expects. In today’s market, we are seeing some risk-off trading, with Treasuries and the JPY higher.

Good world growth: As the PMI data below shows, the global economy is doing rather well. The JPMorgan Global Manufacturing PMI hit 53.1, the highest level since May 2011. In addition, 96.3% of nations are seeing readings above the expansion line of 50, and 92.6% are seeing positive yearly readings. Developed markets are outperforming emerging and Europe is putting in the strongest data.

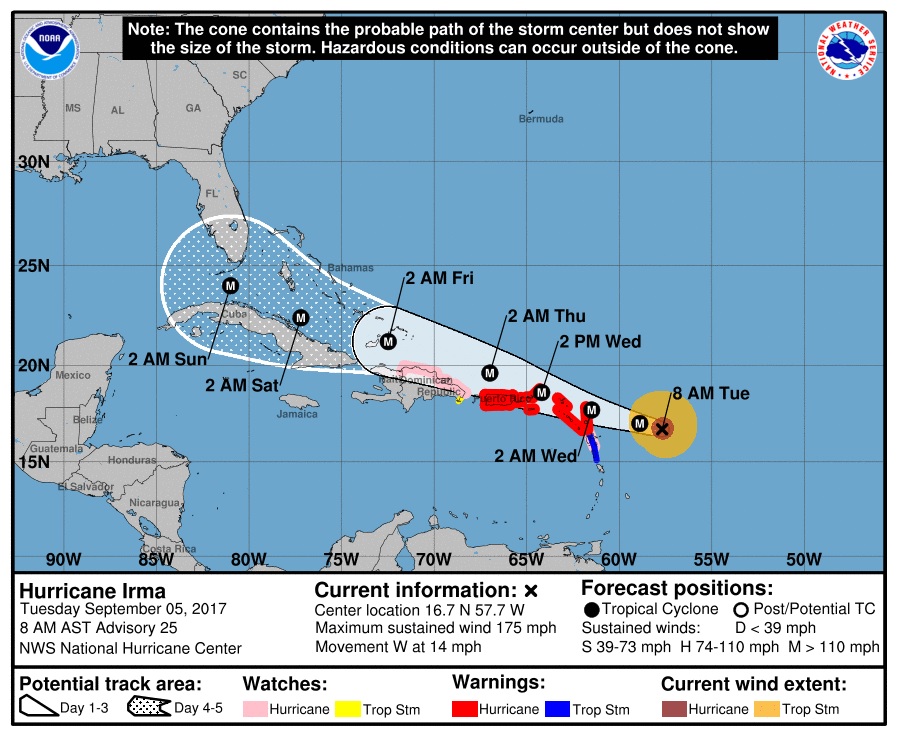

Hurricane Irma: This cyclone is now a Category 5 hurricane. The five-day forecast cone shows it entering the Gulf of Mexico on Sunday.

(Source: National Hurricane Center)

There is a high-pressure cell over the mid-Atlantic; meanwhile, a cold front passed through St. Louis yesterday evening, bringing rain and cooler temperatures. The steering of these two factors will determine the path of Irma. At present, forecasters are assuming the combination of these two factors will push Irma up into Florida, Georgia and the Carolinas. Nearly all the models show it taking a sharply northern turn early next week. However, if the cold front stalls, Irma could end up in the GOM and perhaps affect recovery efforts in Texas.

The debt ceiling: We believe the debt ceiling issue is now probably resolved with the spending needed for Texas’s recovery. We will be watching for how far borrowing limits are extended. If they are not moved significantly, we could revisit this issue by December.

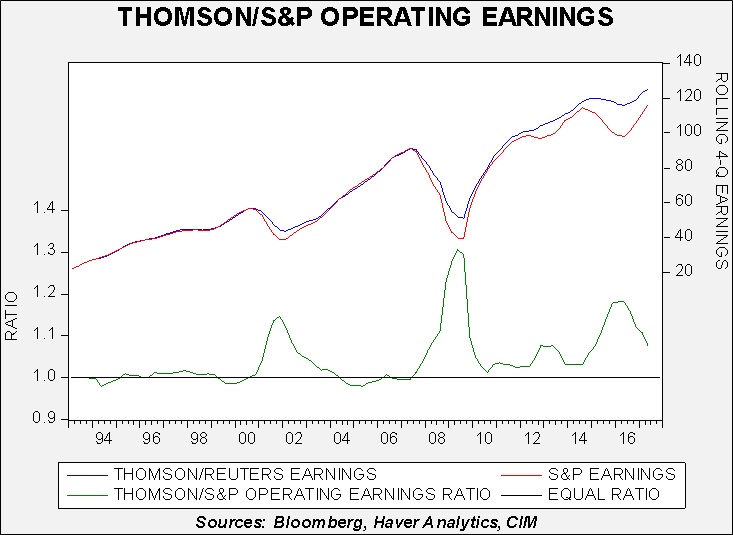

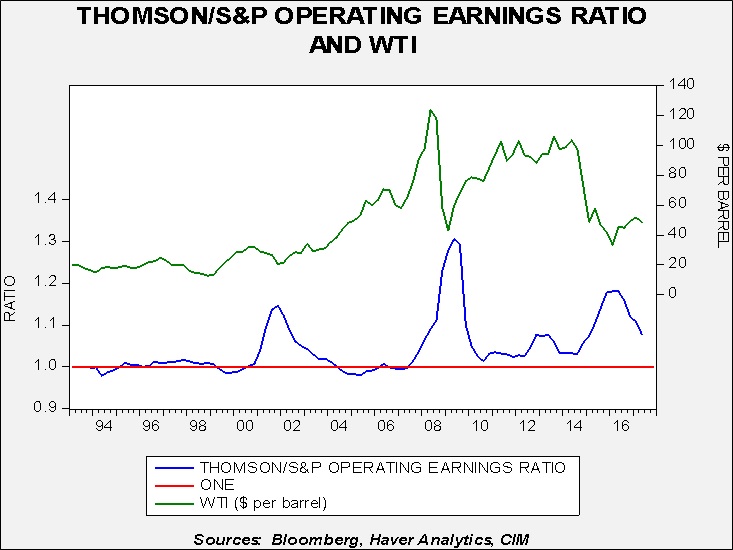

We have previously documented the difference between S&P 500 operating earnings reported by Thomson/Reuters and Standard and Poor’s. Although both series purport to measure the same thing, there can be rather wide divergences. These exist due to differences in how unusual events are accounted for; we do often see long periods where the two series are identical but, in this bull market, the Thomson/Reuters data has tended to consistently exceed the S&P numbers.

This chart shows the two series from 1994, with the lower line showing their ratio. The reason we monitor these divergences is that an elevated ratio has led to bear markets and recessions in two previous instances. Fortunately, the ratio is narrowing, although the difference in terms of the past four quarters is still notable, with Thomson/Reuters at $125.07 while the S&P is at $116.14.

One reason for the recent change in the ratio could be oil prices.

The drop in oil prices coincided with a widening of the ratio. Thus, it is possible that S&P treats the impact of falling oil prices on earnings differently than Thomson/Reuters. If oil prices remain elevated from recent lows, the spread between the two series should also narrow.

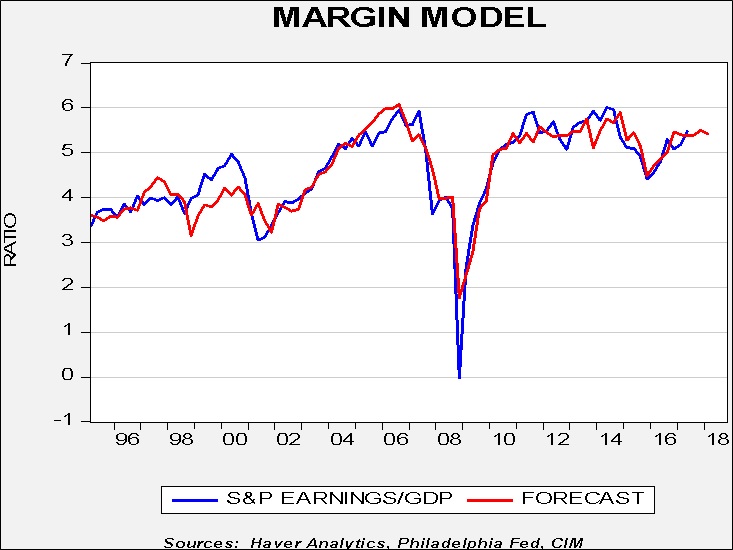

This year’s earnings story continues to be the expansion of margins. Looking at S&P operating earnings compared to GDP, we have seen a solid recovery in margins. Our margin model has been projecting a recovery and stabilization around the level of 5.5% of GDP. If that is the case, the growth rate in earnings should slow to the pace of nominal GDP over the next few quarters.

Based on our analysis, we are on pace for a year-end operating earnings number, basis Standard and Poor’s, of $121.50, a 14.3% rise over this series report from last year. A similar growth number for Thomson/Reuters would put this year’s earnings at $136.10 compared to the current expectation of $131.10. However, since the gap between the two earnings series is narrowing, current expectations are probably about right as that would be consistent with the current ratio. If the two narrow further, current expectations may be too high. Still, in any case, margins remain strong and should offer support for equities.

[Posted: 9:30 AM EDT] Happy Employment Day! We recap the numbers below. Here is what we are watching today:

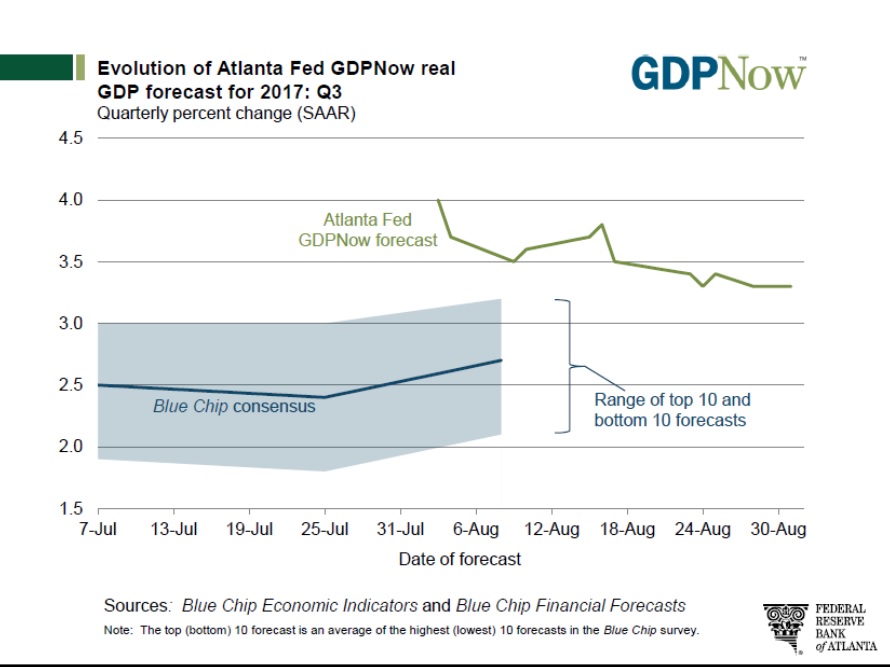

Q3 GDP looking strong: Q2 GDP was revised to 3.0%, and the Atlanta FRB is projecting a 3.3% growth rate for Q3. We present the relevant charts below.

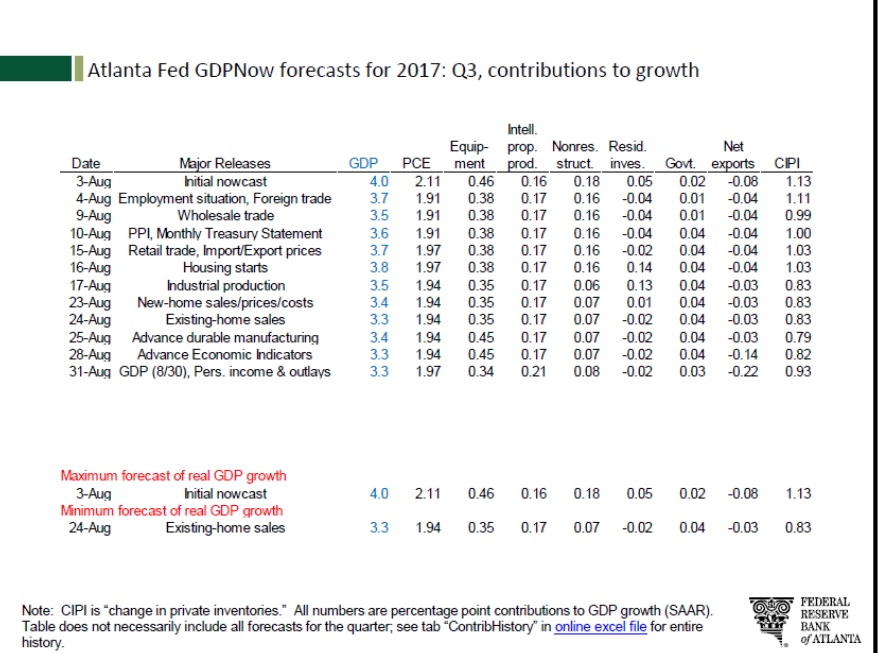

The estimated growth rate is coming down but is still stronger than the consensus estimate. Below is the breakdown by contribution.

Consumption remains strong and inventories are expected to add a point to growth; in fact, inventories and PCE contribute most of the growth in the forecast, representing all but 40 bps of the expected increase. The data suggests a steadily improving economy. We will be watching to see the impact of Harvey in the coming weeks.

CPC meetings in October: The Communist Party of China (CPC) announced that its 19th Party Congress meetings will begin October 18. This is the meeting where Xi Jinping will announce his new Standing Committee, the body that is effectively his cabinet. In a Chinese leader’s second term, he gets to select his own Standing Committee, whereas the Standing Committee is usually filled with allies of the previous leader in the initial election. So, unlike the U.S. system, the Chinese leader has more power in his second term. We will be watching closely for an “heir apparent”; if Xi fails to pick a Standing Committee member that looks like the next president, it is possible that Xi might try for a third term.

Kenya elections: Last night, Kenya’s Supreme Court ruled that the results from last month’s presidential election were invalid; as a result, new elections will take place within 60 days. The unprecedented ruling was a stunning blow to the incumbent, President Uhuru Kenyatta. The previous election’s results showed that he had defeated his opponent, Raila Odinga, with 54% of the vote. Although it is likely that there were some forms of voter intimidation and voter fraud on both sides, which are fairly common in developing countries, we believe these irregularities are unlikely to explain the margin of victory. The decision is the first time in Kenya’s history, as well as Africa, in which an election was overturned by the Supreme Court and is likely to raise tensions as the new election draws near. Trading on the Nairobi stock exchange was halted temporarily due to fears that political uncertainty could harm the economy.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Accept