Author: Rebekah Stovall

Asset Allocation Weekly – Has Bitcoin Become a Substitute for Gold? (October 8, 2021)

by the Asset Allocation Committee | PDF

Over the last half-decade, one of the most dramatic developments in finance has been investors’ embrace of cryptocurrencies such as Bitcoin. Once considered merely an exotic technology with little relevance to investment portfolios, Bitcoin has now become a popular tool for investing. One reason for its popularity is that some investors see Bitcoin and other cryptocurrencies as a substitute for gold and other precious metals in the face of the currency debasement implied by today’s loose fiscal and monetary policies. This report takes a quick look at whether Bitcoin can really be seen as a substitute for gold.

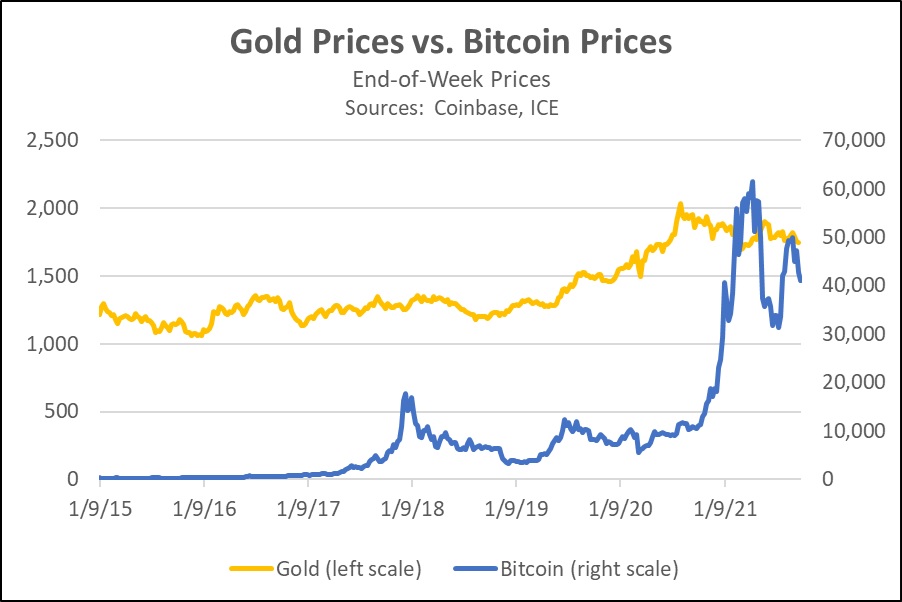

Although Bitcoin was invented in 2008, we rely on the pricing data from cryptocurrency exchange Coinbase starting in 2015, when Bitcoin trading really began to take off. As shown in the chart below, Bitcoin prices and gold prices have both risen from the beginning of 2015 to the present. Over the entire period, weekly Bitcoin and gold prices have had a positive correlation of approximately 0.71. Similarly, a simple regression model relating Bitcoin prices to gold prices suggests a strong positive relationship between the two. In that model, the weekly change in gold prices explains almost half the weekly change in Bitcoin prices.

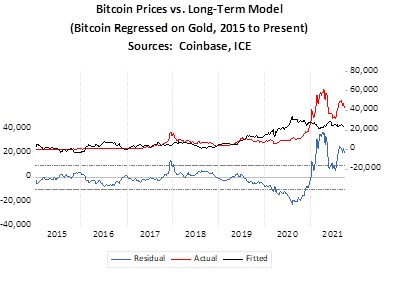

Even though Bitcoin and gold prices have both risen over the last six and a half years, Bitcoin has often diverged widely from the trend in gold prices, and our analysis suggests the relationship between the two assets has recently flipped. As shown in the chart below, actual Bitcoin prices since mid-2020 have diverged widely from what the long-term relationship would suggest.

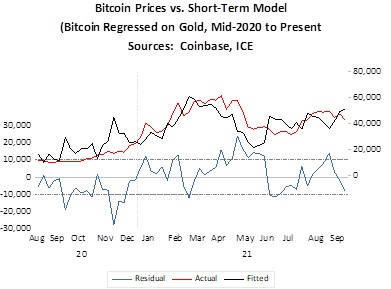

Importantly, a shorter-term model relating Bitcoin prices to gold prices only from August 2020 to the present suggests their relationship has reversed, most likely because investors now see Bitcoin as a true substitute for gold rather than just a complementary asset as in the prior period. Since August 2020, the correlation between Bitcoin and gold prices has come in at -0.80, suggesting that rising Bitcoin prices are now associated with falling gold prices. A short-term regression model covering August 2020 to the present not only confirms that the two asset prices now move in opposite directions, but the model also does a better job of explaining the change in Bitcoin prices. One version of the short-term model using gold prices lagged by four weeks and explains almost 70% of the change in Bitcoin prices.

This evidence suggests that as Bitcoin trading expanded and more investment funds have been channeled into the asset, it has taken on the characteristics of a substitute for gold. At first glance, this makes sense. As the world’s fiat currencies are increasingly threatened by loose fiscal and monetary policies, the limited supply of Bitcoin makes it look like it could retain its value, just as the limited supply of gold does. Indeed, Bitcoin has features that are even more attractive than gold, such as being much easier to transfer among investors and cheaper to hold (you don’t need a warehouse or security guards for your Bitcoin, after all!). All the same, we think investors should be wary about trying to substitute Bitcoin for gold. As we saw in China over the last week, governments intent on preserving their sovereignty and issuing their own central bank digital currencies could outlaw Bitcoin and other cryptocurrencies at any time or at least impose onerous regulations that would undermine their value. In other words, investors looking to protect themselves from currency debasement should probably continue to favor gold and other precious metals over cryptocurrencies.

Weekly Geopolitical Report – Afghanistan, Part IV: China (October 4, 2021)

by Thomas Wash | PDF

In Part I of this report, we reviewed the history of Afghanistan and why great powers have fought over it for centuries. Part II examined how the United States exit from Afghanistan will affect Pakistan, India, and Iran. Last week, Part III focused on how the U.S. exit will play out for Russia and the Central Asian countries. This week, we wrap up the series with a look at the implications for China and beyond, along with a discussion of the overall investment ramifications of the U.S. withdrawal.

Historically, China has tried to maintain a relatively low profile in Afghanistan. However, the U.S. troop withdrawal from the region has forced China to confront the problems that it has hoped to avoid. Without a U.S. presence in the region, Islamist extremism could potentially run rampant along Chinese borders. Additionally, instability in Afghanistan could hinder Chinese efforts to expand its influence into Central Asia and the Middle East. As a result, we suspect that China will embark on a potentially costly effort to fill the power vacuum left by the U.S. in Afghanistan. In this report, we will discuss how the U.S. withdrawal impacts China and how China may look to stabilize the region.

Asset Allocation Weekly – #55 “The Prices We Don’t See” (Posted 10/1/21)

Asset Allocation Weekly – The Prices We Don’t See (October 1, 2021)

by the Asset Allocation Committee | PDF

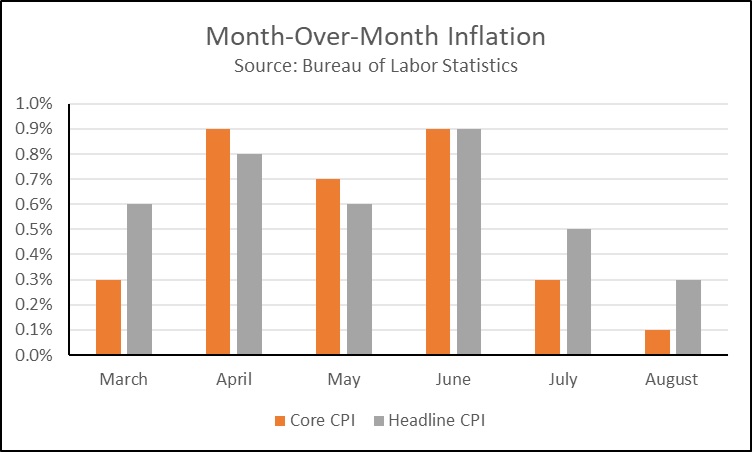

For four consecutive months, consumer prices as measured by the Consumer Price Index (CPI) have risen 5% from the prior year. The pace of inflation has sparked concerns that the Federal Reserve may be wrong in describing inflation as being transitory. However, our research suggests there may be more validity to the Fed’s claim than meets the eye. In this report, we discuss some evidence supporting the argument that inflation will be transitory. We also discuss the possibility that inflation may last longer than expected as well as the length of time in which we expect inflation to normalize.

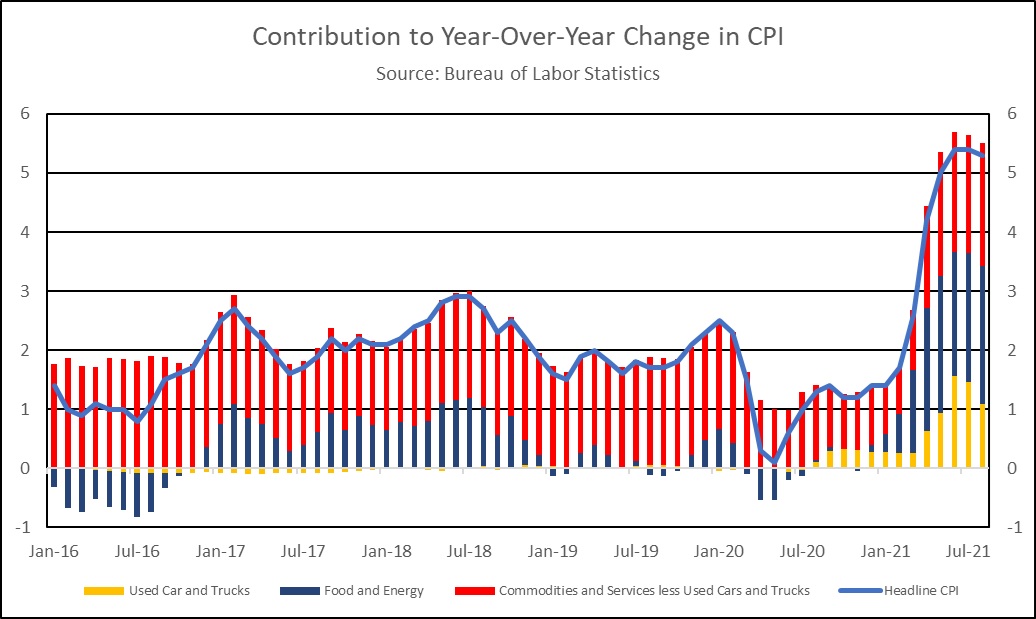

The most recent CPI report showed that inflationary pressures have eased sharply over the last two months. Monthly inflation (which is more sensitive to incremental change compared to annual comparisons) as measured by the CPI excluding the volatile food and energy components (Core CPI) went from a 30-year high in April to benign levels in August. The reduction in inflationary pressures coincided with a steep deceleration in the month-to-month inflation of used cars and trucks. In August, used car and truck prices fell 1.5% from the prior month. The decline in used car and truck prices likely relieved much of the pressure on the overall price index.

To help illustrate the impact that used car and truck prices have had on inflation, the above chart shows contributions to the yearly change in CPI. Used car and truck prices, in yellow, went from being a relatively insignificant part of CPI prior to the pandemic to accounting for about one-fifth of the annual increase in CPI from May to August. This single category was the biggest contributor to inflation over the last few months. The boost in used car prices has elevated the overall index drastically and the impact will likely reflect in the annual change numbers in CPI at least until mid-2022.

That being said, we are not certain that a slowdown or reversal in the rise of used car prices will automatically result in lower inflation. There are other price categories that have yet to recover to their pre-pandemic lows, and their recovery could offset the declines in used car and truck prices. Shelter prices, for example, are still rising at a slower pace than prior to the pandemic as people have been slow to move back into cities.[1] Meanwhile, increases in COVID-19 cases around the country have prevented hospitals from raising prices for many services. Thus, it is possible that inflation could rise even further over the next few months as services continue their recovery.

However, there is a risk of longer-term inflation. As the chart above shows, the contributions of energy and food to CPI have also increased over the last few months. Rising shipping and warehousing costs have had an adverse effect on food prices. These higher costs have forced firms to raise prices or accept lower margins. So far, firms have been reluctant to push all of the costs onto their consumers, but they may not have a choice if prices remain elevated. Additionally, energy prices have rallied over the last few months as demand has recovered. Demand for energy products could subside over time, while new climate restrictions could make it costlier to produce these energy products. Even though the recent ban on new drilling on federal land has not completely hampered production, it does appear that the industry could be headed for a decline in the future. In response to this threat, it appears that energy firms have now prioritized paying down debt and repaying shareholders over reinvesting into new drilling. If this trend continues and production falls, prices will likely rise.

In our view, the rise in inflation should decline over time as supply chain disruptions and other pandemic-related distortions subside. Nevertheless, we are not confident that inflation will revert to its pre-pandemic level. Our expectation is that inflation could start to stabilize around mid-2022.

[1] CPI is weighted by city population, thus prices in major cities such as New York are weighted heavier than prices in mid-sized cities like St. Louis.

Business Cycle Report (September 30, 2021)

by Thomas Wash | PDF

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. The intention of this report is to keep our readers apprised of the potential for recession, updated on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

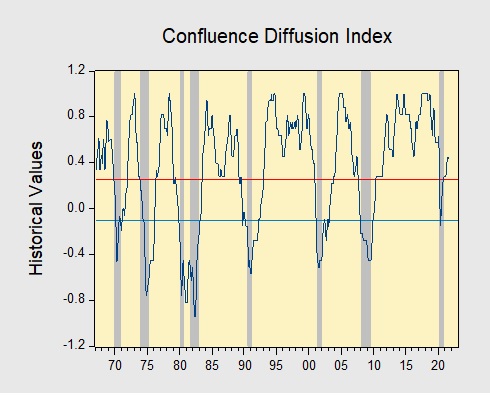

In August, the diffusion index rose further above the recession indicator, signaling that the recovery continues. In the financial markets, a sharp rise in COVID-19 cases led to a modest sell-off in equities throughout the month. Meanwhile, construction and manufacturing activity improved due to stable levels of demand. Lastly, a huge miss in employment payrolls led to doubts about the strength of the recovery. As a result, eight out of the 11 indicators are in expansion territory. The diffusion index rose from +0.4545 to +0.4697, remaining well above the recession signal of +0.2500.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is headed toward a recovery. On average, the diffusion index is currently providing about six months of lead time for a contraction and five months of lead time for a recovery. Continue reading for a more in-depth understanding of how the indicators are performing and refer to our Glossary of Charts at the back of this report for a description of each chart and what it measures. A chart title listed in red indicates that indicator is signaling recession.

Weekly Geopolitical Report – Afghanistan, Part III: Russia and Central Asia (September 27, 2021)

by Patrick Fearon-Hernandez, CFA | PDF

In Part I of this report, we reviewed the history of Afghanistan and why great powers have fought over it for centuries. In Part II, last week, we examined how the United States exit from Afghanistan will affect Pakistan, India, and Iran. This week, our focus is on how the U.S. exit will play out for Russia and the Central Asian countries. We’ll wrap up the series next week with Part IV, which will look at the implications for China and beyond, as well as the overall investment ramifications of the U.S. withdrawal.

Asset Allocation Weekly – #54 “The Supply Side Worry on Inflation” (Posted 9/24/21)

Asset Allocation Weekly – The Supply Side Worry on Inflation (September 24, 2021)

by the Asset Allocation Committee | PDF

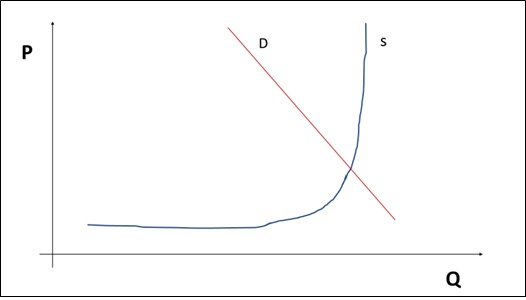

In the 1970s, the U.S. had a serious inflation problem. By the end of the decade, it had become the most critical economic policy issue. Although inflation can be a complicated topic, one way of simplifying it is to see it through the intersection of aggregate supply and aggregate demand.

On this stylized graph, prices levels are rising. In the short run, the most common way to address price levels would be to engage in austerity policies, e.g., raising interest rates, increasing taxes, reducing spending. However, that outcome also reduces output, meaning growth declines.

In the late 1970s, President Carter started implementing deregulatory policies. The goal was to affect the supply side. By expanding supply, price levels would decline and output would rise.

The supply side policies of the Reagan/Thatcher revolution were mostly deregulation and globalization. Deregulation allowed for the rapid introduction of new techniques and new technologies. Globalization naturally expanded the available supply. Both undermined the power of labor to push price increases into the economy.

The recent rise in inflation raises questions about the future path of prices. The FOMC maintains that inflation will be “transitory.” Although the actual definition of the word, at least in the context of policy, is “fuzzy,” it does appear that the rise in prices will moderate at some point.

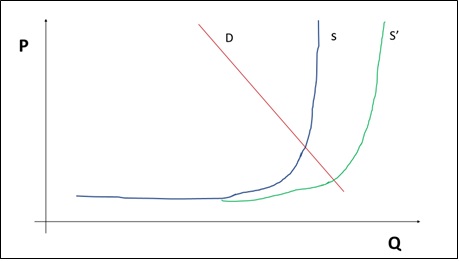

Our concerns are twofold. First, using the second graph, we would argue that the supply situation has moved from S’ to S. Supply chains have been disrupted and supply will remain tight until they are repaired. However, the degree to which inflation is transitory may depend on how these supply chains are fixed. It is important to note that globalization relies on a functioning hegemon that provides global security and a reserve currency. America’s standing as a hegemon has become less certain as Americans appear less willing to engage in the sacrifices required to maintain the role. If that is the case, a return to S’ is less likely.

Another factor is tied to deregulation. In the 1970s, there was clear under-investment and malinvestment. The “rust belt” occurred to reduce the malinvestment that had emerged. To make new investment, saving had to rise and the most effective way to increase saving is to lower taxes on upper income brackets. Although overall saving doesn’t necessarily rise, it becomes concentrated in fewer households which makes it easier to concentrate investment in a similar fashion. However, over time, deregulation has tended to create industry concentration. Concentrated industries may hamper the expansion of supply.

Under conditions of competition, extraordinary profits tend to attract new entrants into the industry. As new entrants enter the market, individual firm profits eventually decline. In addition, the expansion of competition makes it difficult to raise prices. Competition acts as a break on inflation; if higher costs affect the industry, it may simply end up causing a decline in profit margins. But, with concentration, the ability for new competition to enter the market may be thwarted. Consequently, profits may persist. An oligopolist or monopolist might not increase capacity under high prices and may instead just simply accept elevated profitability.

The economic term for this is “market failure,” where the market fails to deliver the best outcome for society. In the 1970s, the supply constraints came from the lack of incentive to invest. Taxes were too high, and regulation increased costs and discouraged investment as well. Our current situation appears to be different. As the world deglobalizes, prices will rise as supply tightens. Ideally, this increase in price levels will trigger a supply response; however, if industry is overly concentrated, the response may not occur to the degree required.

It is too early to tell whether this is the situation we are facing, but the longer transitory price levels remain elevated, we have to entertain the notion that a period of higher inflation may be upon us. We still don’t see signs that we are returning to the 1970s—labor power is still too weak, and inequality favors muted inflation. But just because we are not seeing circumstances that resemble the 1970s, it doesn’t mean we are going to see inflation levels consistent with the last two decades.