Author: Rebekah Stovall

Asset Allocation Weekly – Powell and Fed Independence (September 10, 2021)

by the Asset Allocation Committee | PDF

Chair Powell’s term as leader of the FOMC comes to an end in early February 2022. It appears likely, at this time, that he will be reappointed for another four-year term. Decision markets currently put the odds of another term at 85%. Given all the policy actions that are on the docket for this autumn—an infrastructure bill, the budget, and the debt ceiling—not to mention the political capital lost over Afghanistan, it seems unlikely that the administration has enough bandwidth to push a new Fed chair through Congress. The path of least resistance is to renominate Powell.

However, least resistance doesn’t mean no resistance. Left-wing populists in Congress want a different Fed chair. This group thinks Powell is too lenient on bank regulation and wants someone more committed to climate change policy. Powell has mostly conducted an accommodative monetary policy.

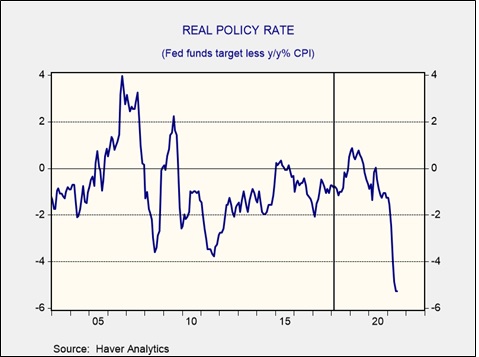

This chart shows the real fed funds rate; Powell’s term is shown by the vertical line. Although he briefly had a positive real policy rate in parts of 2018 and 2019, most of his tenure has seen negative real policy rates. And, his quick reaction to the pandemic has been widely complimented.

Opponents to Powell’s reappointment are really getting at philosophical issues surrounding the central bank. The question really is whether or not central banks should be independent. There is a longstanding difference of position on central bank independence. For those who oppose it, the argument is that the central bank should have monetary policy aligned with fiscal policy. This is what is often called the “whole of government” approach. It makes sense that policy should move in a single direction; it makes little sense for government policy to work at cross-purposes and that outcome is possible with an independent central bank. During WWII, the Fed stabilized interest rates in order to support the war effort. This is a classic whole of government policy. It would have caused problems if the Fed had raised rates to offset the effects of government spending on the war effort.

It appears to us that Powell’s opponents are really pushing for a whole of government approach. The argument seems to be that the issues of inequality and climate change are so critical that normal policy approaches are not justifiable. Instead, the Fed should conduct monetary policy to support government efforts to transform the economy away from fossil fuels and to reduce inequality. Therefore, fiscal spending to reduce the impact of climate change should be accommodated by expanding the balance sheet to provide affordable funding.

Those who argue for central bank independence point out that money is critical to the proper functioning of society. There are essentially two ways that societies have tried to enforce monetary stability. The first is through linking money creation to a commodity, often gold. The idea is that users will have more faith in the store of value function of money if the control of the supply is given to an entity outside of government. Since gold is created through mining, the supply of money is independent of government actions.

The second way that societies have created stable money is through central bank independence. The idea is that if the central bank’s primary job is defending the value of the currency (which ultimately is about stabilizing inflation), and if it can act independently of fiscal policy, then stable money can be created. For the most part, most nations have stopped using a metal standard for money; in practice, metallic standard money was too inflexible. During periods of industrialization, when the supply of goods rose, the supply of gold might not expand fast enough to prevent deflation. History shows that consumers and firms tend to act asymmetrically to deflation compared to inflation. Deflation tends to depress consumption and investment because there is less incentive to spend as prices are declining; the longer one waits to buy, the better the price. So, governments have concluded that moderate inflation is the best outcome for society. Since the 1980s, there has been a consensus that central bank independence coupled with a clear inflation target was the best way to stabilize money.

Policy differences have tended to be constrained within the framework of central bank independence. There have been debates between “hawks” and “doves” about how policy should be implemented. In general, the hawks lean toward maintaining a low inflation target and moving preemptively to ensure the target isn’t violated, whereas doves tend to be more forgiving on violating the inflation target to support economic growth. Recent actions, led by Chair Powell, to make the inflation target less stringent suggest he leans dovish on policy.

In general, the argument for the whole of government approach is that it makes little sense for government policy to work at cross-purposes. If the economy needs stimulus, why should fiscal policy be eased while monetary policy is tightened? The downside of this approach, as history indicates, is that every government believes its goals are sacrosanct and wants no constraints; this situation will tend to lead to higher inflation. The monetary stability approach, in contrast, suggests that money is too important to be left solely in the hands of the political class. Left to their own devices, the political class will tend to put less emphasis on monetary stability. Thus, either a metallic standard or central bank independence is necessary. Critics of this approach argue that policy can be overly constraining.

What the left-wing populists are proposing isn’t simply a dovish policy but a wholesale change in the conduct of monetary policy. Selecting a different Fed chair probably won’t accomplish that outcome; the Federal Reserve-Treasury Accord of 1951 established the Fed’s independence. It would likely take a broader act of Congress to accomplish what the left-wing populists want.

For investors, this debate is critically important. Although Chair Powell will likely be renominated, the push for a whole of government approach is something that bears watching. Modern Monetary Theory assumes a non-independent central bank and that theory has been in ascendency. A move away from central bank independence increases the odds of higher inflation and less constraint on government policy. Although the Fed remains independent, that policy isn’t scriptural; it comes from Congress and can be removed by that same body.

Asset Allocation Weekly – Are Strong Profits Sustainable? (September 3, 2021)

by the Asset Allocation Committee | PDF

(Note: due to the upcoming Labor Day holiday, there will not be an accompanying podcast episode this week.)

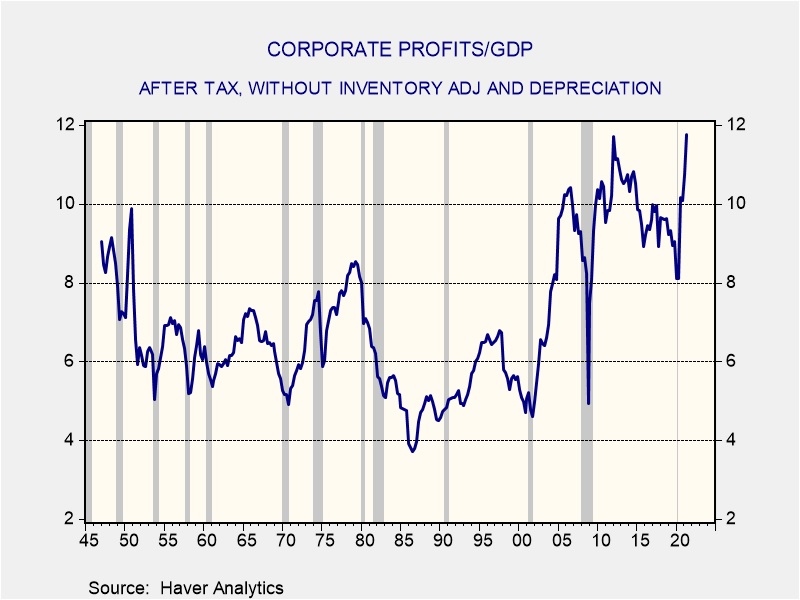

With the first update of Q2 GDP, the Commerce Department released its corporate profits for the economy. Using after-tax profits, which exclude inventory adjustment and depreciation, profits relative to GDP hit a new record.

By this measure, profits were 11.8% of GDP, edging out the previous peak of 11.7% in Q1 2012. The data show that it is not unusual for profits to decline in recessions and rebound in recoveries. However, this recession, though deep, was the shortest on record. The profit/GDP recession trough was the highest in the postwar era; in other words, the usual profit decline, scaled to GDP, was much less than seen in earlier recessions.

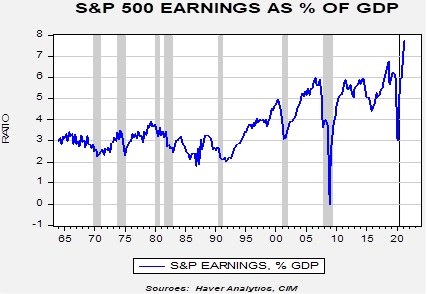

S&P 500 operating earnings relative to GDP have hit a new record as well.

The key question is whether the surge in profits, both on the national level and for the S&P 500, can be sustained. The history of both series suggests that, absent a recession, earnings tend to moderate but remain elevated. So, optimism about future earnings is justified. However, there is a broader issue at work. In the 1970s, when inflation was elevated, corporate profits tended to rise in tandem with prices. Firms, facing higher costs, were able to pass along these costs to their customers. This action exacerbated inflation. Until we see supply constraints ease, inflation will continue to rise unless consumers reduce their spending or profit margins fall. If margins are maintained, either inflation will remain elevated or consumers will have to reduce their spending.

Weekly Geopolitical Report – The Storm Before the Calm: A Review (August 30, 2021)

by Bill O’Grady | PDF

(N.B. Due to the Labor Day holiday, the next report will be published on September 13.)

Although we maintain an official reading list with capsule reviews, occasionally we come across a book that we think is important enough to review as a report. George Friedman’s newest book, The Storm Before the Calm: America’s Discord, the Coming Crisis of the 2020s, and the Triumph Beyond,[1] is just such a book. Friedman is a well-known geopolitical scholar who has written numerous books. He founded Stratfor in 1996 and went on to found Geopolitical Futures in 2015.

Historical analysis tends to break down into one of two schools. The first is the “Great Man Theory,” which suggests that history is dominated by towering historical figures who shape the world. The second is the “Great Wave Theory,” which postulates that history is driven by broad economic, social, political, and other trends, and that people and leaders are shaped by these trends. Those in the first school believe that people shape the trends. The second school holds that this idea is nonsense, and what we refer to as “great men” are really like great surfers—they are figures who understand the world they are in and “ride the wave” to glory. Like all hard categories, neither is perfect. In reading history, it’s rather clear that there have been some remarkable people. At the same time, they are often the right person in the right place at the right time, meaning that we are all, to some extent, shaped by our circumstances.

The school an analyst aligns with is important. Although history is studied for its own sake, we often study history to predict the future. A “great man” theorist is watching the principal actors to see how they will shape the world. Analysts in this school pay close attention to personalities, whereas analysts from the “great wave” school pay less attention to personalities and focus more on the conditions by which these people come to power. Great man theorists have great concern about who takes power, while great wave theorists are much more concerned about the situations in which those in power find themselves. In other words, there are fundamental differences in how analysts from either school predict the future based on history.

Friedman is a wave theorist. He doesn’t believe that individuals can reverse trends that are in place and that leaders are dependent on the circumstances in which they take power. When Friedman looks at the future world through the viewpoint of history, he is examining trends to see if they are enduring or about to change.

[1] Friedman, George. (2021). The Storm Before the Calm: America’s Discord, the Coming Crisis of the 2020s, and the Triumph Beyond. New York, NY: Anchor Books.

Business Cycle Report (August 27, 2021)

by Thomas Wash | PDF

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. The intention of this report is to keep our readers apprised of the potential for recession, updated on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

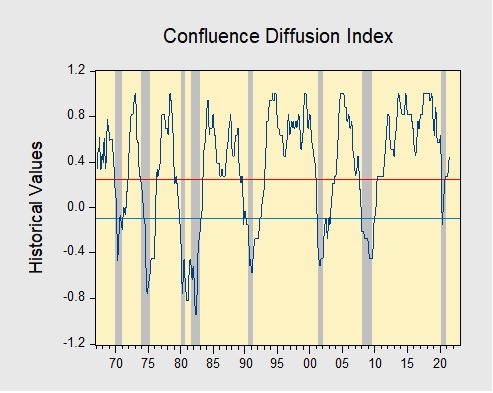

In July, the diffusion index rose further above the recession indicator, signaling that the recovery continues. In the financial markets, a sharp rise in COVID-19 cases led to a modest sell-off in equities throughout the month. Meanwhile, construction and manufacturing activity slowed as increasing costs for materials and labor continue to be a problem for homebuilders and factories. Lastly, the labor market remains strong as payrolls expanded at a faster than expected pace. As a result, eight out of the 11 indicators are in expansion territory. The diffusion index rose from +0.3939 to +0.4545, remaining well above the recession signal of +0.2500.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is headed toward a recovery. On average, the diffusion index is currently providing about six months of lead time for a contraction and five months of lead time for a recovery. Continue reading for a more in-depth understanding of how the indicators are performing and refer to our Glossary of Charts at the back of this report for a description of each chart and what it measures. A chart title listed in red indicates that indicator is signaling recession.

Asset Allocation Weekly – #51 “This Recovery is Different” (Posted 8/27/21)

Asset Allocation Weekly – This Recovery is Different (August 27, 2021)

by the Asset Allocation Committee | PDF

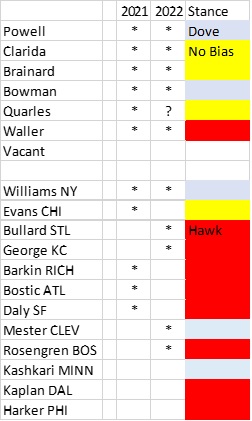

Since the Federal Reserve was granted independence in 1951 there have been 11 recessions. Although each recession and recovery are somewhat unique, analysts tend to compare them for clues about future economic activity and policy actions. In terms of monetary policy, Chair Powell has staked out a dovish path, suggesting that the first rate hike may not occur until 2023. However, recent comments from Fed officials suggest the chair’s position is becoming increasingly isolated.

On this table, voters are designated by stars. Currently, there are five committed doves on the FOMC. We expect the no-bias camp to vote for stimulus reduction next year at the earliest. The hawks, on the other hand, are committed to moving this year. Although we could see a rise in dissents later this year, we suspect that policy will remain steady until 2022.

Next year could be interesting, to say the least. Powell’s term as chair ends in February and Quarles’s term as vice chair for regulation ends in October 2021. His full term as governor extends to 2032; although it is customary for a governor to step down once a vice chair position ends, Quarles has indicated he will stay around for a while. If the no-bias group shifts to tightening, Powell may have to tighten or face losing a vote.

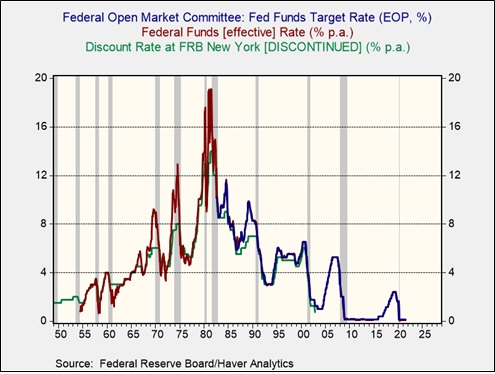

Monetary policy in recoveries and expansions has varied over the years. Prior to 1982, it wasn’t always clear from the behavior of fed funds alone whether policy had changed. To estimate changes, we can also use the New York FRB discount rate as an indicator.

Looking at the recessions from 1955 (the first after independence) onward, what is striking is that the FOMC often moved to raise rates rather quickly after the recession ended. During the seven recessions, the average number of months from the end of the recession to the first rate hike is 13 months. In the past three, the average is 48 months. It has been four decades since the FOMC raised rates quickly into a recovery. For three decades, investors have become accustomed to the slow withdrawal of stimulus.

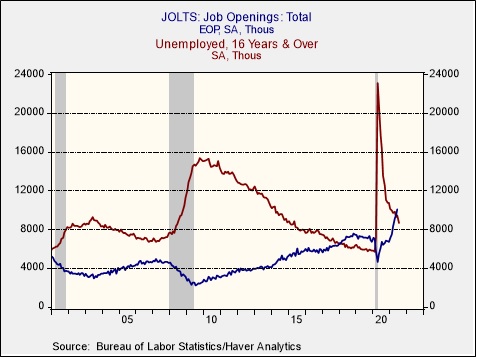

However, this recovery appears to be much different than the past three. In part, the recovery has been stronger due to massive fiscal and monetary policy support. But another factor is that the recession, although short in duration, was unusually deep. Although sometimes deep recessions have “L”-shaped recoveries, this one did not. One way to see this is by comparing job openings to the number of unemployed workers.

During the entirety of the recovery from the 2001 recession, the number of unemployed exceeded job openings. In the previous recovery, it took until March 2018, almost nine years after the recession ended, for openings to exceed the number of unemployed. In the current recovery, we crossed that line in May, 13 months after the last recession ended.

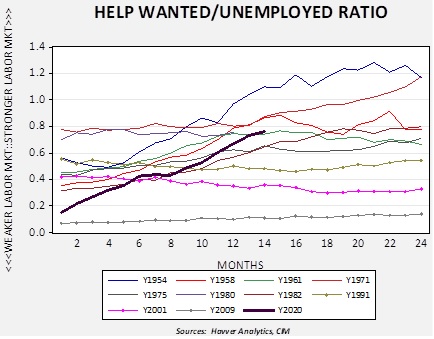

Unfortunately, the JOLTS report, which measures job openings, started in 2000, so it doesn’t provide a long-term history. The Conference Board had a series where it measured help wanted ads relative to the number of unemployed. It was discontinued in 2010. Although that number is a ratio based on an index, we created a model from the JOLTS report that approximates the help wanted/unemployed ratio to the present.

Comparing the behavior of the help wanted/unemployed ratio from the end of every recession since Fed independence, the current recovery is acting more like the pre-1990 cycles. We have denoted the past three with dots on their lines and it is notable that the labor market didn’t improve over the two years after the end of the recessions. So far, the FOMC leadership is acting as if this recovery is similar to the past three cycles; if it is not, policy will likely need to tighten much faster than the market expects.

Weekly Geopolitical Report – Data and Geopolitics: Part II (August 23, 2021)

by Patrick Fearon-Hernandez, CFA | PDF

In Part I of this report, we discussed why today’s political leaders and governments are now paying such close attention to the control of data and information, and what that means for geopolitics. In Part II, we will show how China is perhaps the best example of modern state control over data and information. Indeed, China’s current “industrial policy” is essentially a form of “information policy.” A central strategy for China’s current leadership is to generate, utilize, control, and protect information as a way of building up its geopolitical and economic power. To wrap up the discussion, we will discuss the ramifications of this trend for investors.

Daily Comment (August 23, 2021)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT] | PDF

Good morning and happy Monday! Schools are reopening, and it’s a risk-on day today. U.S. equity futures are higher, and gold and oil are rebounding as well. The Fed’s meeting at Jackson Hole is this week, but like last year, the meeting will be virtual. Our coverage begins with an active weekend for the weather. Tennessee had heavy rain, and there was a tropical storm in New England. An update on Afghanistan is next, followed by China news and the international roundup. We then discuss economics and policy, and we close with pandemic coverage.

Climate: It was a busy weekend for extreme weather events. Tennessee was hit with torrential rain over the weekend, with reports of 15” to 20” in some areas. Flooding was widespread, as was the damage. At least 22 people have died, and many more are missing. Tropical Storm Henri slammed Rhode Island and other parts of New England over the weekend. Hurricane Grace made landfall in Mexico as a category 3 storm; the storm caused at least eight fatalities.

China: Taiwan’s reliance on the U.S. for defense is a concern.

- Lithuania has faced the ire of Beijing for allowing Taiwan to open a diplomatic mission in Vilnius. China has retaliated by banning new food imports from Lithuania.

- One worry for U.S. military planners is that Taiwan isn’t really preparing to resist a Chinese invasion. Although the country has bought flashy military hardware from the U.S., it hasn’t actually hardened itself to make an invasion difficult. Taiwan needs to build shore barriers, lay sea mines, and take similar measures to make an amphibious assault difficult. Complicating matters is that Taiwan has gone to a volunteer military and is struggling to find recruits. Taipei’s plan appears to be hoping the U.S. intervenes. Although we think the U.S. would (and we feel quite certain Japan would) take military action to defend Taiwan, it’s hard to sell that to the U.S. when Taiwan doesn’t appear willing to defend itself.

- As China’s economy slows, iron ore prices are falling fast. Not only does a slowing economy need less iron, but Beijing is also pushing steel producers to use electric arc furnaces to make steel. The feedstock is scrap and is less polluting.

- As bitcoin mining leaves China, miners are returning to the U.S.

Afghanistan: Here is what we are following:

- Disorder around the Kabul airport continues. U.S. troops have reportedly expanded the security perimeter, but conditions remain chaotic. The British military reports that at least seven Afghans have died due to stampedes. There are growing concerns that Islamic State elements may begin attacking aircraft at the airport, pointing to the fact that the Taliban’s control is far from complete. Six U.S. air carriers have been ordered to assist in transporting evacuees. This action is part of the Civil Reserve Air Fleet, created as part of the Berlin Airlift in 1952. The planes appear to be mostly ferrying evacuees to air bases for processing.

- The U.S. may extend the deadline for troops to be out of Afghanistan past August 31.

- The Taliban have reportedly contacted former officials, including Hamid Karzai and Abdullah Abdullah, to build an inclusive government. It isn’t clear how this would work or why the Taliban is interested. It could be that the group realizes its hold on the country is tenuous, or it might be to soften or avoid sanctions. Even without clear sanctions, banks and other financial firms have been cautious about money transfers. We note that northern Afghanistan, which held out against the Taliban the last time the group held power, appears to be building opposition again.

- EU leaders have been meeting to discuss what to do about the almost certain flood of refugees that will occur because of the collapse of the Afghan government. What is being revealed, yet again, is that the EU has no unified plan for refugees.

Economics and policy: Budget and infrastructure start to move through the House, and fears of peak growth are upon us.

- Speaker Pelosi is preparing to move both the budget bills and the bipartisan infrastructure package. A moderate bloc of nine representatives is demanding the bipartisan bill go first; this plan is opposed by the populists, who fear that the budget will fail to pass in its current form, and thus, spending goals will fail. Pelosi usually wins out on these things, but so far, the moderates are holding tight. Our expectation is that both will eventually pass, but the current budget of $3.5 trillion won’t make it through in its current form; we expect something closer to $2.0 trillion.

- Economic data continue to come in strong but are weaker than expected. This development is leading economists and strategists to suggest we have already seen peak growth.

- Logistical snarls continue, and there are growing worries that there may not be enough container ships to meet demand. Supply constraints tend to trigger inflation, and this sort of inflation is difficult to address. Policymakers, in the short run, can usually only affect demand, so they are forced to tighten policy, effectively taking spending power away from firms and households as prices rise. In the longer run, deregulation can increase available supply, but with a rather long lag.

- The U.K. continues to deal with a severe chicken shortage. One chain restaurant in the country was forced to close 50 shops due to the lack of product.

- U.S. supermarkets report that supplies have become sporadic, leading to shortages and uncertainty of supply.

- The Arizona election audit is due today. Although we expect it to generate a lot of headlines, any real action (recalls, new elections) must first pass through the courts, where the veracity of the audit will face tests.

International roundup: Sweden’s PM is stepping down, and Merkel met with the leader of Ukraine.

- Sweden’s PM announced he is stepping down in November. Stefan Löfven, who lost a no-confidence vote in June only to form a new government in July, has decided he has had enough. His decision has increased political turmoil in the country. Sweden must hold elections by September 2022.

- Chancellor Merkel met with Ukraine’s leader over the weekend. The latter is still unhappy with Germany’s decision to support and complete the Nord Stream 2 pipeline. Merkel tried to assure President Zelensky that Russia won’t be able to use the pipeline as a weapon against Ukraine, but we doubt Kiev believes that.

- Meanwhile, the CDU/CSU continues to languish in the polls. The SDP continues to surge; although the average still shows the conservatives holding a majority, individual polls show the SDU tied with the CDU/CSU.

COVID-19: The number of reported cases is 211,925,410, with 4,433,615 fatalities. In the U.S., there are 37,711,989 confirmed cases with 628,504 deaths. For illustration purposes, the FT has created an interactive chart that allows one to compare cases across nations using similar scaling metrics. The FT has also issued an economic tracker that looks across countries with high-frequency data on various factors. The CDC reports that 428,531,345 doses of the vaccine have been distributed, with 362,657,771 doses injected. The number receiving at least one dose is 201,425,785, while the number receiving second doses, which would grant the highest level of immunity, is 170,821,621. For the population older than 18, 62.4% of the population has been vaccinated. The FT has a page on global vaccine distribution.

- In this most recent wave of infections, the affected population has tended to be younger, with more children being hospitalized. Breakthrough infections are becoming more common, although the majority of those hospitalized are unvaccinated. The Gulf Coast is being especially hard hit, straining medical resources.

- As cases rise, companies are returning to work from home arrangements. The longer such arrangements are in place, the more likely they will become lasting.

- Britain is starting an antibody surveillance program; the goal is to see how long antibodies last, what impact breakthrough infections have on antibodies, and determine how long natural immunity lasts.

- Israel is starting a vaccine booster program due to rising infection rates.

- Jesse Jackson and his wife have been hospitalized with COVID-19.