Author: Rebekah Stovall

Bi-Weekly Geopolitical Report – Prospects for the Dollar in a Fracturing World (September 9, 2024)

by Patrick Fearon-Hernandez, CFA | PDF

As investment managers and strategists, we are often asked by clients about our outlook for the United States dollar. Very often, our clients have heard some worrisome news about a rival currency becoming more attractive than the greenback or global investors selling off the dollar because of economic or political problems in the US. Their concern is often about the US’s growing debt or political polarization. As the world continues to fracture into relatively separate geopolitical and economic blocs, another concern is that China, Russia, Iran, and some of their authoritarian allies want to stop using the dollar for trade and investment. If those countries cut their demand for the greenback, the fear seems to be that the currency will lose value, its purchasing power will decline, and consumer price inflation will rise.

In this report, we provide some guideposts for thinking about exchange rates. We then examine the main global forces that could theoretically reduce demand for the dollar and cut its value. We conclude with a discussion of the prospects for the dollar and the implications for investment strategy.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Asset Allocation Quarterly (Third Quarter 2024)

by the Asset Allocation Committee | PDF

- Domestic economic growth is expected to be solid on continued supply chain rearrangement, the resulting domestic industrial production, and supportive fiscal stimulus. There is no recession in our forecast.

- With the Fed remaining data-dependent regarding the fed funds rate, we believe the likelihood is diminishing for multiple rate cuts this year.

- Economic growth is likely to support credit conditions and domestic equities. Mid-cap equities offer attractive valuations and growth profiles. We have moved to an even weight in our growth/value style tilt.

- Volatility is likely to increase in economic readings as well as market movements as we head into the elections and beyond.

- We maintain the exposure to gold as a geopolitical hedge, and silver is also utilized where risk appropriate.

ECONOMIC VIEWPOINTS

Our three-year forecast period includes expectations for continued healthy economic growth, a constructive environment for risk markets, and support for all capitalizations of domestic equities. Lacking an external shock to the system, our expectations do not include a recession. Market participants have been surprised by the economic resilience despite the prolonged high level of the federal funds overnight rate. Conventional economic wisdom teaches us that rapidly tightening monetary policy should slow the credit cycle and dampen demand, pushing the economy into a contraction. Yet the economy has remained resilient.

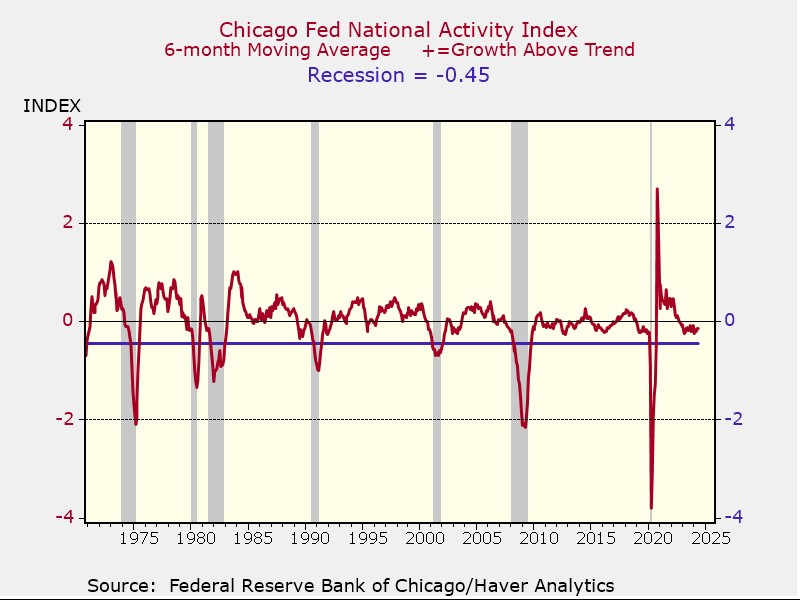

In our view, the economic resilience will persist on the back of structural changes driven by geopolitical shifts, private sector strength, and fiscal spending. Heightened geopolitical tensions and deglobalization will continue to foster a restructuring of supply chains, which is supportive for the domestic economy. At the same time, aging demographics and immigration uncertainty are likely to keep labor markets tight. These are longer-term trends which are not as sensitive to monetary policy and thus have boosted the economy. Despite the strength of aggregate economic activity, certain sectors are likely to experience pressures from high interest rates. For instance, we have already seen slowing residential construction, and higher borrowing costs are impacting smaller companies. This is confirmed by the Chicago Fed National Activity Index (shown in the first chart), which has fallen but is still well above recessionary levels.

We are expecting the private sector to remain strong in the current higher rate environment as many businesses took advantage of low rates over the past decade. Consequently, the impact of higher rates will be felt gradually as debt matures and is refinanced over the next several years. Meanwhile, the trend of reshoring continues to bolster investments in domestic capacity construction. Manufacturing capacity building is a multi-year process that will result in increased domestic manufacturing capability, buoying the economy when construction spending wanes.

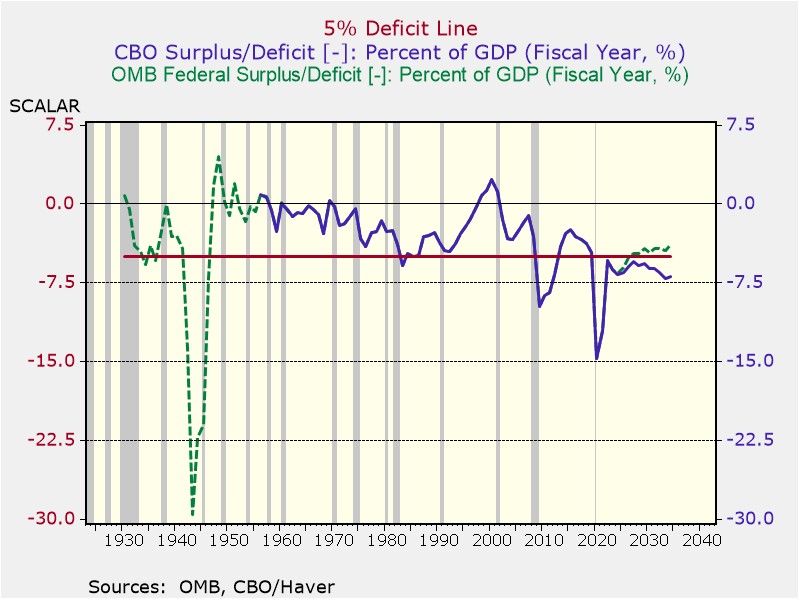

Fiscal spending is another key factor sustaining continued economic growth. This second chart shows the government deficit, which has largely expanded due to non-discretionary spending. Due to the non-discretionary nature of the increase and political gridlock, deficit spending is likely to continue in the near term which should support corporations as well as consumers. We note that, with the exception of the 1945 recession, the economy has never slipped into an official downturn when the fiscal deficit has been 5% or more of GDP.

We are likely to see inflation volatility in the near and medium term. In the medium to long term, due to structural reasons, inflation is likely to remain higher than we have generally experienced over the past decade. We expect the monetary policy response to be well-telegraphed and data-dependent. If inflation moves closer to the 2% target, the Fed could ease before year-end. Although we are now in the midst of the US election season, our expectation is that Fed policymakers will continue to be agnostic regarding the party in power among the branches of government and rely on economic data to guide them in their monetary policy decisions regarding the target fed funds rate and changes to the balance sheet.

STOCK MARKET OUTLOOK

Our outlook calls for solid domestic economic growth during the forecast period. Economic growth leads to demand and healthy margins, which benefit earnings, and also bolsters investor sentiment and valuations. This environment is typically supportive of risk assets and will generally be positive for all capitalizations. The mid-cap space, in particular, offers attractive valuations and therefore we continue to overweight US mid-cap equities. However, current higher interest rates do not equally affect all capitalizations. Small capitalization equities hold a larger proportion of floating rate debt, thus higher rates affect them disproportionately. Although we reduced our exposure to small caps slightly this quarter, we still find valuations attractive. To mitigate concerns about high interest rates affecting some small caps, we introduced a quality factor position, which screens for indicators such as profitability, leverage, and free cash flow.

While we remain cautious about the concentration risk in a handful of prominent growth equities, we believe economic conditions will support growth stocks, in general. Furthermore, the shift to passive investing should continue to spur growth stocks as long as the economy remains healthy. As a result, we shifted our growth/value style bias to even-weight.

We maintain an overweight position in the Energy sector and Uranium Miners due to geopolitical tensions in the Middle East and sustainable energy transition policies. Additionally, we maintain our exposure to the military-industrial complex through investments in military hardware and cyber-defense.

International developed equities remain attractive due to valuation discounts. Many large global market leaders in the developed world ETF are trading at lower valuations relative to domestic large cap companies. We maintain our country-specific exposure to Japan due to ongoing shareholder-friendly reforms and continued capital inflows, which could potentially lead to multiple expansion.

BOND MARKET OUTLOOK

According to a 2018 report by the San Francisco Fed, since 1955 the two-to-10-year segment inverted six to 36 months before the onset of each of the last six recessions. Though the bond market recently marked 24 months since the two-to-10-year portion of the Treasury curve inverted (the longest streak on record), many are now questioning the validity of whether it still serves as a harbinger for recession. With the Fed remaining data-dependent regarding the fed funds rate, the likelihood is diminishing for multiple rate cuts this year. As a result, the yield curve has the potential to remain inverted for an extended period. Underscoring this potential is our expectation regarding heightened inflation volatility throughout the forecast period. Note that we are not expecting the absolute level of inflation to necessarily remain elevated, rather the volatility of the measure from one period to the next. Finally, the net issuance of Treasurys to finance the federal deficit, and notable declines in the proportion of Treasurys held by foreign central banks, indicates growing risk on the long end of the curve, which we find to be uncompensated. Consequently, our positioning is geared to intermediate-term maturities, which we find hold the most allure due to modest stability of rates and resultant limits to market risk.

Among sectors, mortgage-backed securities (MBS) are attractive. Most fixed-rate MBS prices are now well below par, which help address prepayment risk; at the same time, refinancing trends are low enough to limit incremental extension risk. In addition, the Fed’s intentions to dampen its MBS runoff from its $7.3 trillion balance sheet should also help limit spread widening.

Investment-grade corporate bonds are currently trading at relatively tight spreads of +93 basis points to Treasurys, lessening their appeal. Therefore, we find little reason to overweight investment-grade corporates in the strategies with an income component. Speculative grade corporates, however, still offer an attractive spread of +325 basis points. The backstop programs put in place over the past few years by the Fed and US Treasury, notably during COVID and the Silicon Valley Bank run, provide an implied element of support for lesser-rated bonds during crises. Nevertheless, caution dictates our preference for the higher BB-rated bonds in this asset class.

OTHER MARKETS

The position of gold within the commodities asset class is retained as a hedge against elevated geopolitical risks. Gold also presents an opportunity given increased price-insensitive purchasing by international central banks. As in quarters past, we note that international central banks are increasingly positioning gold as a reserve asset in fear of continued weaponization of the US dollar. In the more risk-tolerant portfolios, silver is maintained as an additional precious metal holding. As has been the case for over three years, real estate remains absent in all strategies as demand remains in flux and REITs continue to face a difficult financing environment.

Bi-Weekly Geopolitical Podcast – #43 “Rebirth of US Nuclear Deterrence” (Posted 3/11/24)

Bi-Weekly Geopolitical Report – Rebirth of US Nuclear Deterrence (March 11, 2024)

by Daniel Ortwerth, CFA & Patrick Fearon-Hernandez, CFA | PDF

Fifteen years ago, a revolution in United States national security policy began very quietly. It occurred within a subject we have recently addressed in this forum and that is re-emerging as a hot topic of discussion in national security circles after a long hiatus: deterrence, and specifically the unique role of nuclear weaponry as the preeminent deterrent force. This report uses the timeline and key events of the last 15 years to illustrate the current modernization program for the US military’s nuclear enterprise and to examine how it relates to today’s global geopolitical landscape. The report concludes with a discussion of the program’s implications for investors.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify | Google

Asset Allocation Quarterly (First Quarter 2024)

by the Asset Allocation Committee | PDF

- The likelihood of a recession occurring during our forecast period has declined.

- Domestic economic growth should be robust over the forecast period, although momentum has slowed.

- Elevated geopolitical tensions and ambiguity related to the U.S. elections are likely to create volatility in the markets.

- Inflation volatility is likely to remain elevated as we anticipate inflation should moderate in the near-term but will reaccelerate to higher than pre-pandemic levels due to various structural influences.

- Monetary policy is expected to ease, but we believe market expectations may be too optimistic in terms of the timing and magnitude.

- We have shortened our duration modestly as we expect normalization of the yield curve.

- In domestic equities, we maintain our Value bias as well as quality factors.

- We maintained the exposure to gold and, where risk-appropriate, added silver as a hedge in volatile times.

ECONOMIC VIEWPOINTS

Markets are currently expecting that the FOMC will shift to easing and the economy will avoid a recession. We agree that the likelihood of a recession has declined and expect economic expansion for the majority of our three-year forecast time period. The Fed dots plot indicates 75 bps of easing in 2024 and futures-based market expectations call for even more aggressive easing. Although we concur that the next step is likely to be easing, market expectations may be too optimistic regarding the timing and magnitude, and this mismatch has the potential to create market volatility. We expect the Fed to hold policy steady later this year as we head into elections to avoid the impression of political favoritism.

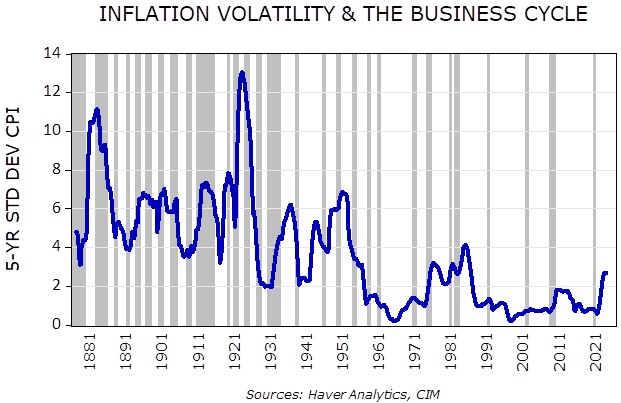

Economic growth should remain healthy over the forecast period; however, we believe that volatility, in general, will remain high for both economic indicators and markets. For example, we anticipate that inflation should continue to moderate in the short term due to tighter monetary policy but will reaccelerate to higher than pre-pandemic levels in the medium term. Factors contributing to tighter supply chains include supply chain rearrangement with reshoring and friend-shoring of industrial capacity, elevated geopolitical tensions, and developed world demographics. For investors, the volatility of inflation is equally as important as the level. As this first chart indicates, the volatility of inflation during the post-Cold War era has been much lower than it was pre-1990. We also expect many other economic and market metrics to return to the more volatile paradigm similar to what existed during the Cold War.

The effects of fiscal spending are a supporting factor for continued economic growth. According to the Congressional Budget Office, fiscal outlays are expected to further increase over the next three years from the current 23.7% of GDP. The Inflation Reduction Act, the CHIPS and Science Act, and the Infrastructure & Jobs Act form an accommodative fiscal backdrop, supporting corporations as well as consumers.

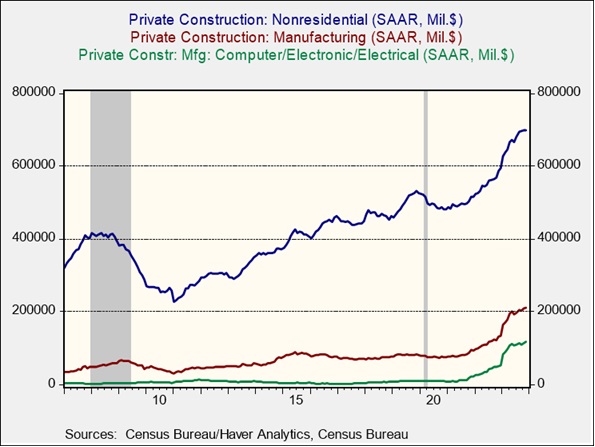

In the coming quarters, domestic industrial production should slowly increase as geopolitical tensions remain elevated and reshoring moves along its intended path. As this chart shows, industrial capacity construction has increased remarkably. Tight labor markets have hindered progress but growing technology/AI use should advance it. Given that capacity buildouts are extended over multiple years, there will be escalating demands on construction, labor, and materials in the short term, while increased revenue realization is likely to occur outside of our forecast period.

In addition to the U.S. elections, pivotal elections abound globally. This is especially significant amidst high geopolitical uncertainty. As the world continues to polarize into blocs, elections provide signposts along the way about the direction and speed of change. This introduces further volatility to the system, and for investors, it necessitates keeping a close eye on their portfolios. Markets tend to focus more on the uncertainty that elections introduce rather than a specific outcome. Moreover, markets discount election results rather quickly, so a quick resolution to the U.S. primaries would be beneficial.

STOCK MARKET OUTLOOK

We expect a good economic backdrop over the forecast period. While earnings growth has slowed somewhat, market consensus is calling for improving margins. The consumer is showing signs of a slowdown, with household debt service ratios rebounding to pre-pandemic highs. While saving levels have fallen, consumer confidence has remained solid and holiday shopping was strong (although we’ll quote Confluence CIO Mark Keller here: “Don’t extrapolate holiday shopping; no matter what, Santa always comes.”). On the other hand, domestic equity valuations might find support from the high levels of cash currently held on the sidelines.

We remain overweight Value across all market capitalizations. In our view, equities categorized as Value have more sustainable earnings growth, their fundamental valuation multiples are historically attractive, and they have a lower exposure to sectors that we view as overpriced. Although Growth has recently outperformed, we anticipate we are in the early stages of a value outperformance cycle. Within large caps, we maintain an overweight position in Energy and exited the Metals & Mining and Industrials sectors. In addition to military hardware exposure via the Aerospace & Defense factor, we also added a position in Cybersecurity as we believe global conflicts will be increasingly cyber-related. The military has a long history of working with private enterprises to innovate in the tech-heavy segments of national security. Our perspective holds that the valuations of small and mid-cap stocks continue to present an attractive proposition, coupled with robust fundamental earnings power. Historically, mid-cap stocks maintain considerable valuation discounts compared to their large cap counterparts. To mitigate potential risks amid economic volatility, we uphold our commitment to the quality factor within our mid-cap and small cap exposures, which involves screening for indicators such as profitability, leverage, and cash flows.

The Uranium Miners ETF that we introduced last quarter was constructive for our portfolios as our thesis of increased nuclear energy use started to materialize. Although the underlying uranium spot price increased significantly, we believe the uranium miners will benefit further. The evolving landscape of baseload energy production, influenced by dynamic policies, has opened a window of opportunity for nuclear energy. Ambitious green energy policies are driving substantial goals for reducing fossil fuel usage, yet the current green energy technologies face challenges in generating energy at the required scale and consistency. Given the constrained supply of uranium over the past decade, we perceive the supply/demand imbalance as a robust opportunity for exposure in this sector.

Low valuations in international developed equities are attractive for the more risk-accepting portfolios. The combination of deglobalization and increased geopolitical risks has widened the volatility range of the asset class. We maintain a country-specific exposure to Japan as shareholder-friendly reforms continue to take effect and as capital flows continue moving into Japan, which could potentially lead to a multiple expansion.

BOND MARKET OUTLOOK

Although the steeply inverted yield curve has attracted outsized interest on the short end, as indicated by the $8.8 trillion in money market funds and CDs as of year-end, it will likely prove fleeting as the Fed begins its pattern of easing. Similarly, our expectations of heightened inflation volatility for the foreseeable future combined with the rally in long-dated Treasuries over the past quarter dampen our return expectations for the long end of the curve. Contrasted with our positive view of long Treasuries last quarter, the rally occurred in a much tighter time frame than we anticipated which encouraged us to unwind this position. The belly of the curve, particularly around five years of maturity, holds the greatest allure in terms of rate stability and limitation of both market risk and opportunity cost. Within this segment, we find mortgage-backed securities (MBS) to hold merit within our thesis of an intermediate-term bond focus. With the bulk of conventional mortgages carrying rates well below refi rates, extension risk is currently dampened. Spreads on MBS remain attractive despite their narrowing since October. Conversely, corporate spreads have narrowed to historically tight levels of roughly +100 bps, encouraging a relative underweight to corporates versus the market benchmark.

Speculative grade bonds are also trading at low spreads to Treasuries; however, the concerns we have are confined to the lower-rated segments below BB. The acceptance by investors to rate adjustments on leveraged loans underscores our concern that the risk appetite has become tilted toward lower rated bonds. While this has positive implications for the refinancing wave that is poised to affect companies rated B and below over the next two years, the increased risk tolerance on the part of investors gives us pause. Consequently, the speculative grade bond exposures remain exclusively in the BB-rated segment.

OTHER MARKETS

Among commodities, elevated risks in the Middle East have implications for the price of oil, but the potential economic slowdown is dampening demand; thus, we have exited oil and its derivatives near-term. In contrast, we retain the position in gold as a hedge against elevated geopolitical risks and as international central banks are buying reserves of the metal. Gold is augmented by exposure to silver in the more risk-tolerant strategies given its low price relative to gold by historical measures. Real estate remains absent in all strategies as demand remains in flux and REITs still face a difficult financing environment.

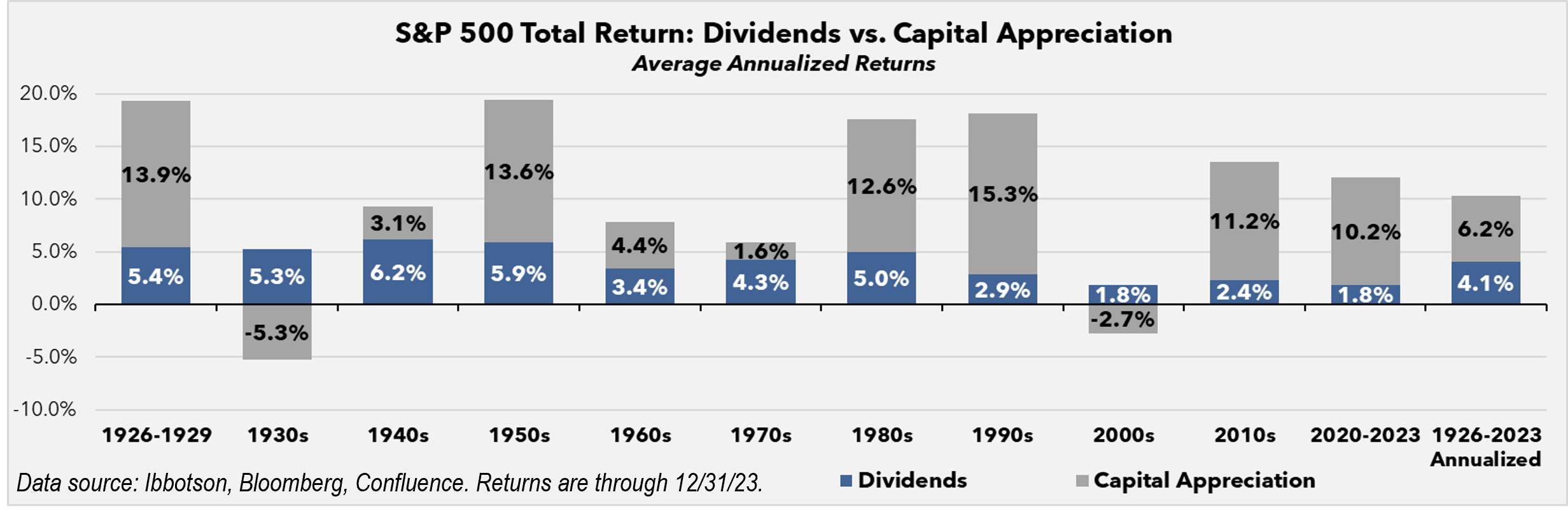

A Good IDEA for the Long Run: The Benefits of Increasing Dividends (December 2023)

A Report from the Value Equities Investment Committee | PDF

In this report, we examine the long-term outperformance of stocks with growing dividends; why certain dividend growers outperform and their attributes; how those attributes correspond to our approach when selecting businesses for the IDEA portfolio; and the impact of inflation on dividend stocks.

Why Dividends? A Bird in the Hand

It is a common maxim in investing that dividends make up a good portion of the long-term total return in the market. This chart demonstrates how significant that contribution has been over the past century. As the saying goes, “a bird in the hand is worth two in the bush”; the same can be said for the predictability of dividends relative to capital appreciation.

An Established History

At Confluence Investment Management, our value equity investment philosophy was initiated at our predecessor firm and continues to be implemented more than 25 years later. Accordingly, the members of the Value Equities Investment Committee have a long history of managing dividend-oriented investment strategies. With a dedicated team of research analysts conducting proprietary research, the fundamental approach is focused on understanding and valuing individual businesses with an emphasis on owning competitively advantaged businesses. This approach is the foundation of all domestic value equity strategies at Confluence, including the Increasing Dividend Equity Account (IDEA) strategy.

Confluence of Ideas – #34 “The 2024 Outlook: Slow-Bicycle Economy” (Posted 12/18/23)

The 2024 Outlook: Slow-Bicycle Economy (December 18, 2023)

by Patrick Fearon-Hernandez, CFA, Thomas Wash, Bill O’Grady, and Mark Keller, CFA

Summary of Expectations | PDF

The Economy

Economic Growth

We expect the U.S. economy to continue growing into 2024, but its momentum has been slowing, and slowing momentum will put the economy at increased risk of recession. As the growth rate continues to moderate or slow, the economy will become increasingly susceptible to shocks such as a domestic financial crisis or a major geopolitical event that saps confidence.

Just as riding a bike too slowly makes it difficult to stay in balance, slowing economic growth will increase the risk of a downturn in the economy.

Recession Risk

Reflecting the risks inherent in a slower-growing economy, we believe the economy is slightly more likely to slip into a recession in 2024 than it is to avoid one. Nevertheless, if a recession does transpire, we believe it will be relatively mild and short-lived.

Inflation & Monetary Policy

In any case, slowing demand growth and the Federal Reserve’s aggressive interest rate hikes since early 2022 will probably lead to further moderation in consumer price inflation. That should allow the Fed to avoid or at least minimize any further rate hikes, but we expect policymakers to try to keep rates high for an extended period to make sure inflation pressures are eliminated.

Elections

The U.S. presidential election in November 2024 could have a big impact on key asset classes. At this point, it appears to be a close race between President Biden and former President Trump, but there is an elevated chance that some third-party candidate or candidates could join the race.

The elevated political uncertainty could keep investors cautious. In contrast, if one candidate appears to break from the pack, or if the election is thrown into the House of Representatives, risk assets could be pushed sharply higher or lower than in our base case.

Market Outlook

Fixed Income

As investors come to accept the Fed’s “higher for longer” stance toward interest rates, we think intermediate- and longer-term U.S. Treasury obligations will be susceptible to selling pressure in 2024, pushing the yield on the benchmark 10-year Treasury note to 4.90% or more.

* The spreads between investment-grade corporate obligations and Treasuries have recently been unusually low, in part reflecting the way many firms refinanced and termed out their debt when interest rates were ultra-low during the coronavirus pandemic. Spreads could remain tight, but if a recession does materialize, we would still expect them to widen to take account of the increased credit risk.

* Similarly, the spread between below-investment-grade corporates and Treasuries is also low, but it would likely widen even more dramatically if economic growth falters.

U.S. Equities

For U.S. large capitalization equities, we forecast that the S&P 500 price index will be between 4,060 and 5,090 at the end of 2024, with a single point forecast of 4,580.

* The rise in the U.S. stock market in 2023 was heavily concentrated among just a few large cap growth stocks. Stocks with smaller capitalizations lagged, making them better values now. We therefore think small cap stocks will outperform in 2024.

* Similarly, value stocks lagged in 2023, likely setting them up to outperform in 2024.

Foreign Equities

We continue to believe that the performance of foreign equities will largely depend on the value of the dollar. Continued strength in the greenback in 2024 is likely to be a headwind for foreign equities, although prudent investors will still want some exposure to the asset class for diversification and as a hedge against any unexpected dollar weakening.

Commodities

Finally, we expect gold and precious metals to be supported in 2024 by a range of factors, including the end of the Fed’s interest rate hikes, safe-haven buying amid today’s increased geopolitical tensions, and strong buying by central banks.

Broader commodities would face headwinds if a recession materializes, but they could snap back by year’s end if any such downturn ends up being short and mild, as we expect.